November 4, 2022 in Challenges and solutions

Modern banking versus traditional banking: The benefits of a blended approach

Financial institutions don’t need to choose when strong, scalable success can be achieved with a combination of the two.

Banking has evolved significantly over the last few decades, with many of today’s fintechs choosing a digital-only, modern-banking approach over the traditional brick-and-mortar-led strategy.

Get the best-of-both worlds

Subscribe for industry trends, product updates, and much more.

The embrace of digital has been largely welcomed by consumers, who increasingly favor online touchpoints for everyday activities such as checking their account balances or transferring money.

While the collective thought process may be that customers no longer value what traditional, in-person banking has to offer, experts from Deloitte and other financial institutions believe branches will remain relevant long into the future. While it’s true that branch use is declining, customers who are applying for banking and lending products are more likely to do so face-to-face. Call-center demand has also increased in over 76% of financial institutions since the pandemic began.

Leaders at financial institutions may be feeling the pressure to dedicate their organization to one approach or the other in order to deliver the best results for their customers and banking teams.

But luckily, financial institutions don’t have to choose between the two — they can adopt modern-banking development that is digital-first and incorporates the most powerful benefits of a traditional strategy.

Traditional banking elements to include in a modern approach

Financial institutions operating with a mostly traditional model have maintained their system for a reason — in large part, it works. Buoyed by decades of experience, these institutions continue to offer stability for long-standing customers, especially those wanting to make regular cash deposits or from an older generation. Here are three key traditional banking elements that can drive value for financial institutions looking to adopt a digital-first strategy:

- Interpersonal connection

Traditional financial institutions pride themselves on the human touch. They offer the in-person channels that have historically helped build strong customer relationships and loyalty. When it comes to interpersonal connections, traditional institutions also benefit from legacy and scale. They have access to a significant amount of customer-provided information, which enables them to provide more personalized customer service, as long as they use it effectively and responsibly. - Trust

Another key edge incumbent banks have over digital-only modern banking organizations is trust. EY’s global consumer banking study found that customers of traditional banks are more confident that their data is protected, feel more empowered, and like the ability to reach their financial institution via a branch, if needed. - Reassurance

Customers value in-person interactions for services that are more complex. Thirty-five percent of boomers and one-third of millennials said they prefer to visit a branch to receive financial advice.

The top benefits of digital banking

Without the restraints of legacy technology and processes, digital-first firms are nimble and agile with the ability to take products to market faster and more cost effectively. Here are three key aspects of digital banking that can help both traditional and more-modern institutions succeed:

- Speed

Digital solutions that leverage automation can improve efficiency and eliminate many of the bottlenecks and paper-based processes rife in traditional banking. The faster, seamless experience of modern banking can help improve the customer experience. - Convenience

Around-the-clock access to digital channels gives customers the ability to bank at a time and a place that suits them. Table-stake digital banking features include quick and seamless onboarding and advanced access and security. - ROI

Faster processes, with less need for heavy lifting by bank employees, free up time to deal with more customers more efficiently.

How digital lending fits into both traditional and modern banking

Digital lending is one of the many offerings both modern and more traditional institutions can use to achieve scalable success. An end-to-end lending software platform offers advantages for the financial institution and its employees that translate to real value for customers, no matter if it’s a credit union with physical locations, an online-only bank, or anything in between. Benefits include:

Shorter loan-life cycles

Digital lending includes a shorter loan-life cycle from origination to close — thanks to automatic aggregation and verification of customer data and documents. In addition to seeing a reduction in the back-and-forth of traditional manual processes, banks and credit unions can build upon customer trust by securely storing sensitive customer data.

Personalized approaches to lending

Using a digital platform gives any institution the ability to tailor each lending product to an individual customer’s journey while offering them additional financial resources and step-by-step guidance throughout the life of their loans.

More meaningful customer connections

Automatic processes help improve overall operational efficiency for employees, freeing them up for more face-to-face interactions. This gives employees the opportunity to become valued advisors invested in customers’ continued financial health while building upon the trust of the institution.

Using a digital solution for a simpler, more intuitive lending process helps boost customer satisfaction and loyalty in the long run.

Modern banking vs traditional banking: How Blend combines the two

Physical branches aren’t going away anytime soon, and in-person interactions will remain valuable for customers long into the future. That’s why Blend supports the best of modern and traditional banking in a single cloud-based platform.

We give financial institutions the tools to level up their digital offering by facilitating end-to-end customer journeys for any banking product. Our unified digital experience with responsive design and guided application workflow helps any process feel simple and straightforward.

Eager to learn more about what Blend can do for your financial institution?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

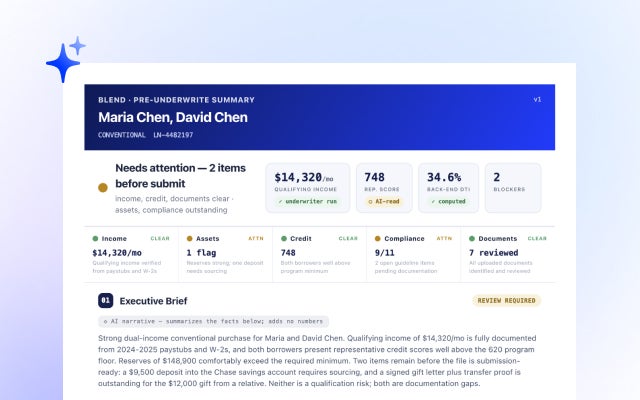

Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Every figure, every source. See how Autopilot's latest update makes pre-underwriting faster to act on.

Read the article about Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

The mortgage market is projected to reach $2.2 trillion in 2026, but flat isn't the same as easy. With per-loan costs exceeding $12,500, discover why cost per loan is the…

Read the article about Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

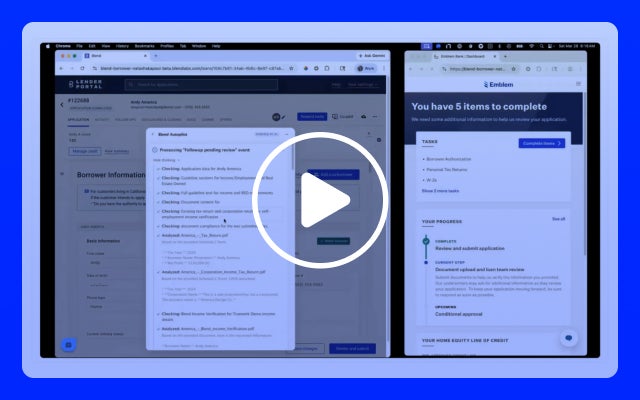

Five-Minute Home Equity: How to Outpace Fintechs and Win Member Loans

How credit unions are using AI to close HELOCs in minutes and outcompete fintech lenders.

Watch video about Five-Minute Home Equity: How to Outpace Fintechs and Win Member Loans