June 22, 2022 in Thought leadership

How loan automation can increase operational efficiency and improve experiences

By automating processes across the end-to-end loan lifecycle, lenders can reduce manual tasks, streamline workflows, and achieve several efficiency benefits.

A typical mortgage loan cycle can take more than 45 days, with the origination cost per loan amounting to as much as $9,000.

With so many lending processes now digitized, why is the mortgage loan cycle still time- and cost-intensive? At many traditional lenders, lending teams are still working with paper-based documentation and switching between multiple disparate software solutions — not just during the application stage, but across processing, underwriting, and closing too.

Automatically tap into new insights.

Subscribe for industry trends, product updates, and much more.

To complete a loan, loan officers are also regularly delayed because they have to wait for customers to seek out key documentation to verify their income, employment, and more. Meanwhile, as many as five underwriters need to get involved with risk assessment and verification, leading to even more bottlenecks.

This situation is far from ideal and is hampering loan officer team productivity. It’s also costing mortgage providers valuable business, in part because customers are being lured by the convenience of alternative fintech offerings. In fact, there’s a 20–30% difference in customer satisfaction scores between customers at traditional lenders and those at fintechs — who often have more modern, digitized processes.

In order to keep their businesses afloat and level up against the competition, lenders need to make the most of every lead they get. How can they achieve this? One approach is by using automation.

How loan automation is streamlining every step of the lending process

With automation, it’s possible to transform the end-to-end loan lifecycle, from the initial application through to processing, underwriting, and finally closing. Let’s explore the potential for loan automation in four key areas.

The application

Loan automation takes much of the hassle out of the application process. Instead of having to manually fill out paper application forms — which can be hundreds of pages long — the whole process can be streamlined through digitization. Data entry can be minimized since fields are pre-filled with linked data and information the consumer has provided in the past. In addition, the application flow can be dynamically updated using information the consumer has inputted previously. Extra features such as borrower single sign-on from any device and the automatic flagging of inaccurate information can make the process even more efficient — reducing the need for lender support.

Florida-based Lennar Mortgage is using loan automation to deliver a best-in-class application process for its customers. “We get some really good feedback on our digital mortgage process as being simple, intuitive, and informative,” said Tom Moreno, Lennar’s chief information officer.

Lennar’s Net Promoter Score illustrates the impact loan automation has had on the customer experience. Lennar customers using a digital application scored the lender 42% higher on the NPS scale.

Processing

Historically, lenders have had to spend countless hours chasing down supporting documents from borrowers. Loan automation, however, can make the process much easier. Borrowers can receive automated checklists of document collection requirements, and these can be automatically adapted for the particular needs of the applicant. This is supported by the real-time checking of entries to flag incorrect or inaccurate documents and data, addressing issues before underwriting even occurs. Overall, loan automation reduces bottlenecks and takes care of any oversights so that loan offers can focus on what matters most: customer service.

By using loan automation for processing applications, mortgage loan officers at Indiana-based Elements Financial now spend less time collecting documents and more time interfacing with their community and growing their business.

In fact, Elements Financial has reduced the average member’s mortgage application-to-fund time by five calendar days. “Not only are we providing a consistent member experience … but our members are also completing their applications more quickly and converting at higher rates,” said Ron Senci, EVP, sales and lending at Elements.

Underwriting

Verifying and validating information can cause significant delays in the underwriting stage, but automation during earlier stages can help speed up these fundamental activities. Data connectivity included within the digital application flow allows a substantial portion of the verification work to occur at the time of application. Connections to assets, payroll, tax accounts, and other third-party data sources can help improve accuracy and, in some cases, support expedited or even instant verification and approvals. It’s a win:win scenario — minimizing friction for the borrower and improving efficiency for the lender.

Lending teams can also use loan automation software to configure risk rules, tolerances, outcomes, and stipulation requests. By modernizing workflows in this way, lenders can streamline manual underwriting processes or even automate less complex approvals entirely. Not only can this lead to shortened cycle times and reduced costs, it can also free underwriters to focus on higher-scrutiny applications.

Texas-based SWBC Mortgage is using loan automation software, and it has been able to cut loan cycle time by 28% during a two-month pilot.

“I’ve been rolling out in-house and external products for 30 years, and I’ve never experienced anything that went as quickly and smoothly as this implementation,” said Debbie Dunn, chief operating officer at SWBC Mortgage

Closing

The full benefits of automation can only be unlocked when lenders make the shift to digital closing workflows — efficiencies up front can be minimized or even lost completely when the final steps of the process revert to manual, antiquated interactions. In modern closing systems, data syncing and document preparation can be automated, thanks to integrations with LOS, eNote providers, and eVaults. This can minimize signing errors and missing documents, signatures, or dates, making for a streamlined and faster closing process.

Amarillo National Bank in Texas is using loan automation software to streamline the closing process. It’s doing this by automating closing document preparation and enabling closing teams to send documents to the settlement agent to finalize details before sharing them with the borrower.

The benefits have been significant. “We’ve been able to see faster funding times,” said Lauren Lyons, senior system administrator. “With documents coming back digitally, it speeds up the back and forth communication.”

Unleashing new efficiencies, from application to close

By leveraging loan automation software, lenders can achieve a new level of efficiency across the lending process.

The result? Lending teams have far more time to focus on delivering the meaningful service that leads to better customer experiences and long-term loyalty.

Want to see more benefits of loan automation?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

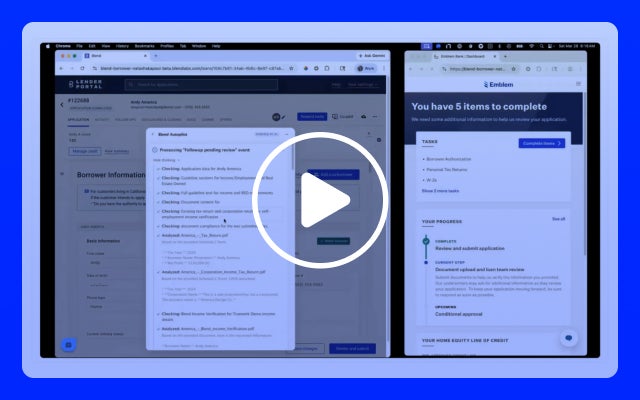

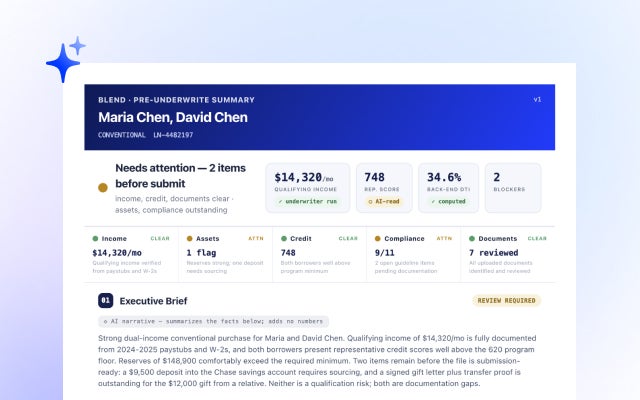

Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Every figure, every source. See how Autopilot's latest update makes pre-underwriting faster to act on.

Read the article about Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

The mortgage market is projected to reach $2.2 trillion in 2026, but flat isn't the same as easy. With per-loan costs exceeding $12,500, discover why cost per loan is the…

Read the article about Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

Five-Minute Home Equity: How to Outpace Fintechs and Win Member Loans

How credit unions are using AI to close HELOCs in minutes and outcompete fintech lenders.

Watch video about Five-Minute Home Equity: How to Outpace Fintechs and Win Member Loans