August 10, 2022 in Challenges and solutions

Embracing digital lending for credit unions

Maintain the service you’re known for as you close loans faster by harnessing the power of digital lending.

Wondering how to make your credit union more competitive against powerful banking conglomerates? The key might be offering what many traditional financial institutions don’t.

After all, in early 2022 there were 5,002 credit unions in the United States, slightly outnumbering the 4,796 FDIC-insured commercial banks and savings institutions. And while those large banks tend to have deeper pockets to spend on technology, credit unions that transform their digital lending processes can remain competitive — and even outcompete — in the current banking landscape.

Leveraging digital lending for credit unions

Credit unions have historically built their competitive advantage over traditional financial institutions by focusing on three key factors:

- Lower, more competitive interest rates

- More flexible eligibility requirements for loans

- A dedication to personalized, member-focused banking

Investing in even modest shifts to digital lending enables line-of-business leaders to offer improved lending experiences and products while retaining the personalized approach that preserves customer loyalty.

Take, for instance, Mountain America Credit Union (MACU). The credit union made the strategic decision to invest in delivering a superior mortgage experience and improved customer service, an extension of their member-first approach. This digital pioneer among credit unions honed in on the right customer demographics and expanded access to lending products through a commitment to digital — made possible through cloud banking software delivered by Blend.

Hone in on inefficiencies

Credit unions face competition from an increasingly crowded market of fintech startups, banking conglomerates, and digital-only market disruptors. When it comes to expanding digital lending for credit unions, however, both big and small changes can lead to a substantial return on investment:

- Establish priorities. Where in the lending process do you see the biggest inefficiencies? If you’re working with a tight technology budget, select one or two attributes of your credit union lending to streamline.

- Remove manual paper processes. Long before it adopted Blend’s infrastructure, MACU began phasing out its paper processes. Offering customers the ease of online document signing and digital loan applications can greatly reduce loan cycle times.

- Maintain a digital trail. Implementing digital lending for credit union strategies can help keep stakeholder information and each step of the loan process consolidated in one centralized platform, providing a documented process for improved audit tracking.

- Focus on an omnichannel lending experience. Can your credit union’s customers begin the loan process from anywhere — their home computer, tablet, or smartphone? The key to customer conversion when it comes to loans is ease of process.

- Capture analytics. All the data points contained within an encrypted digital platform can give your financial institution the insight to make better, more strategic decisions when it comes to loan product offerings

How Blend drives end-to-end digital transformation

University of Wisconsin Credit Union partnered with Blend to overhaul its mortgage lending process. Not only did Blend reduce the burden on loan officers in terms of time savings through origination, processing, and underwriting, it enhanced efficiency organization-wide. UWCU reported $2,866 in ROI from Blend per loan, a 12-day decrease in loan cycles, and a 33% increase in loan volume above market growth rate.

Blend’s cloud-based banking infrastructure can give credit unions the tools they need to stay ahead of the digital lending credit union curve.

Want to learn more about how credit unions can capitalize on the opportunity of digital?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

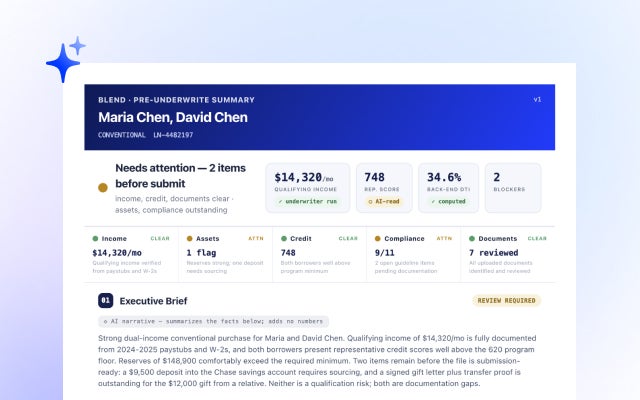

Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Every figure, every source. See how Autopilot's latest update makes pre-underwriting faster to act on.

Read the article about Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

The mortgage market is projected to reach $2.2 trillion in 2026, but flat isn't the same as easy. With per-loan costs exceeding $12,500, discover why cost per loan is the…

Read the article about Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

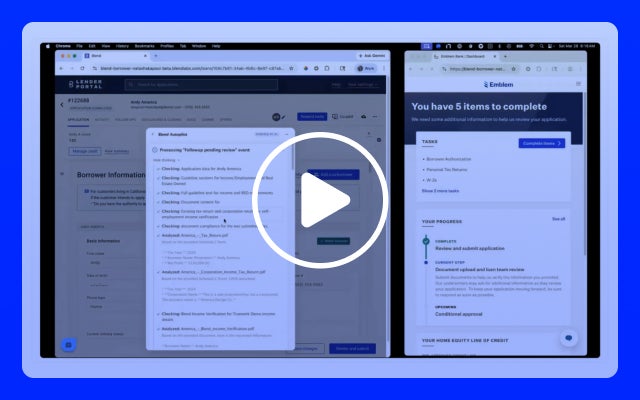

Five-Minute Home Equity: How to Outpace Fintechs and Win Member Loans

How credit unions are using AI to close HELOCs in minutes and outcompete fintech lenders.

Watch video about Five-Minute Home Equity: How to Outpace Fintechs and Win Member Loans