June 10, 2026 in Blend momentum

Blend Autopilot Week 14 Update: Borrower Chat Comes to Rapid Loans, Smarter Large-Deposit Requests, and a Loan File That Fills In More of Itself

Autopilot Weekly Update: Week 14

Autopilot already works on Rapid loans. This week it starts talking to those borrowers too.

Two weeks ago, the Rapid Autopilot switch moved into your hands, letting the agent run on Rapid loans alongside flagship. The borrower-facing chat (the assistant a borrower opens to ask what’s left to do) still couldn’t see those loans. This week it can. Alongside that, the agent got more precise about which large deposits it actually asks borrowers to explain, and it now fills in more of the loan file on its own. A quieter week, pointed squarely at the borrower’s experience.

Borrower chat comes to Rapid loans

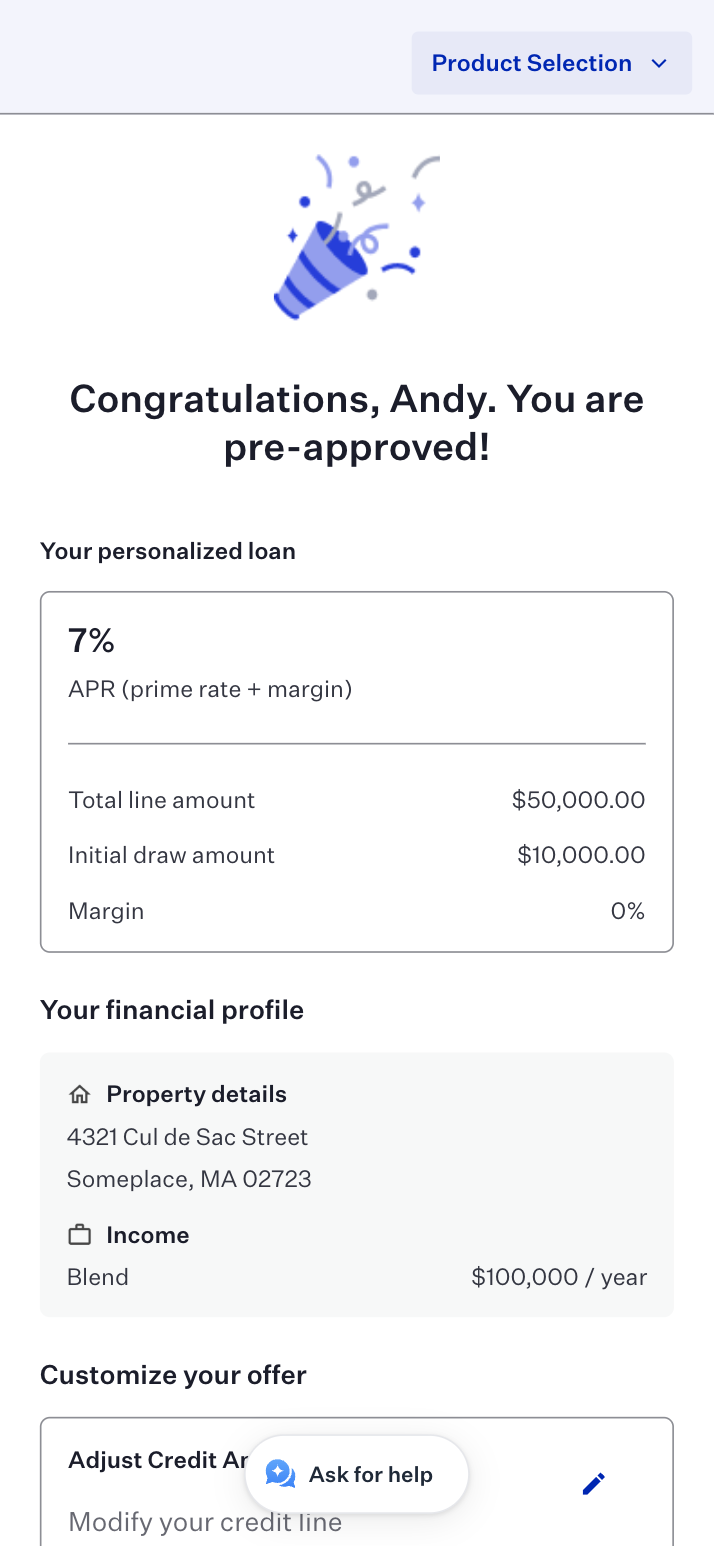

Borrower chat has always been good company on a flagship loan. A borrower opens the assistant, asks “what do you still need from me?” or “where is my application?”, and gets an answer grounded in their actual file. On Rapid loans, that conversation came up empty. The chat read only the standard lending data, so a Rapid loan’s application details, its current step, and its status were invisible to it. The borrower got a chat window with nothing useful behind it.

This week closes that gap. On a Rapid loan, borrower chat now reads the loan’s application data directly and answers with the same context it has on flagship: where the application stands, what step comes next, and what the agent still needs. It reuses the same data the agent already relies on for Rapid loans, so the answers a borrower sees line up with the work Autopilot is actually doing on the file.

This update is designed with joint applications in mind. A borrower can ask freely about their own loan and get straight answers, while the assistant only ever shares that borrower’s own information. A co-borrower’s details stay private. Borrowers get openness about their own file, without exposing the person they are applying with.

Flagship loans are untouched by the change. For lenders who have turned Rapid Autopilot on, the borrower conversation now reaches as far as the agent does.

Fewer large-deposit letters a borrower doesn’t need

When a sizable deposit lands in a borrower’s bank statement, lenders often have to ask where it came from, and the borrower writes a letter of explanation or tracks down a paper trail. It’s one of the more tedious asks in a file, so it matters that Autopilot only raises it when it genuinely should. The agent infers based on the size of the deposit relative to the borrower’s monthly income. This week, two changes make that process more accurate.

First, the agent now derives the monthly income figure behind that threshold using Lending’s own formula, rather than producing its own figure independently and risking a number that drifts from the rest of the system. The bar a deposit has to clear before it needs explaining now matches what the rest of the loan uses.

Second, the agent no longer raises a large-deposit explanation against an account that isn’t on the loan in the first place. Previously, a deposit on a stray or unlinked account could trigger a request the borrower had no reason to answer.

The combined effect is fewer borrowers asked to chase down paperwork for a deposit that never needed it, and a cleaner follow-up queue for the loan officer. The agent is still flagging deposits that genuinely need sourcing. It’s just stopped asking about the ones that don’t.

Subscribe to Autopilot updates

Rental income and employers now fill in on their own

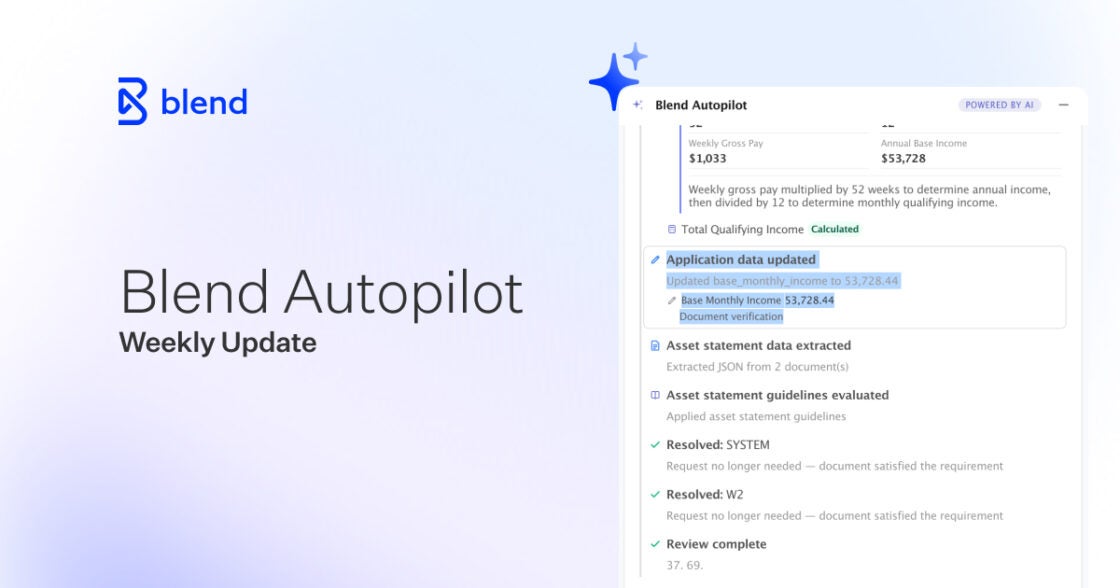

Last week, Autopilot started updating the loan file automatically with verified data: checking, savings, and trust balances, plus employment, non-employment, and other income, captured as the agent reads documents instead of waiting for a loan officer to transcribe them. This week, those automatic updates reach further into the file.

Rental income now flows through. When the agent works a loan with investment property income, it derives net rental income from the Schedule E figures and adds it to the application, so rental-reliant files fill in the same way salaried ones already do. Employer details follow the same path: when the agent reads employment information, it records the employer on the application rather than leaving a loan officer to key it in. And the set of asset types it fills in expands beyond the core deposit accounts to cover the other assets a borrower discloses.

The throughline from last week holds. The agent treats every one of these as data capture, not an eligibility verdict: the number lands in the file even when the agent has also flagged a follow-up against it. The practical effect is a loan file that grows more complete on its own, across more of the income and asset picture, the longer Autopilot works it.

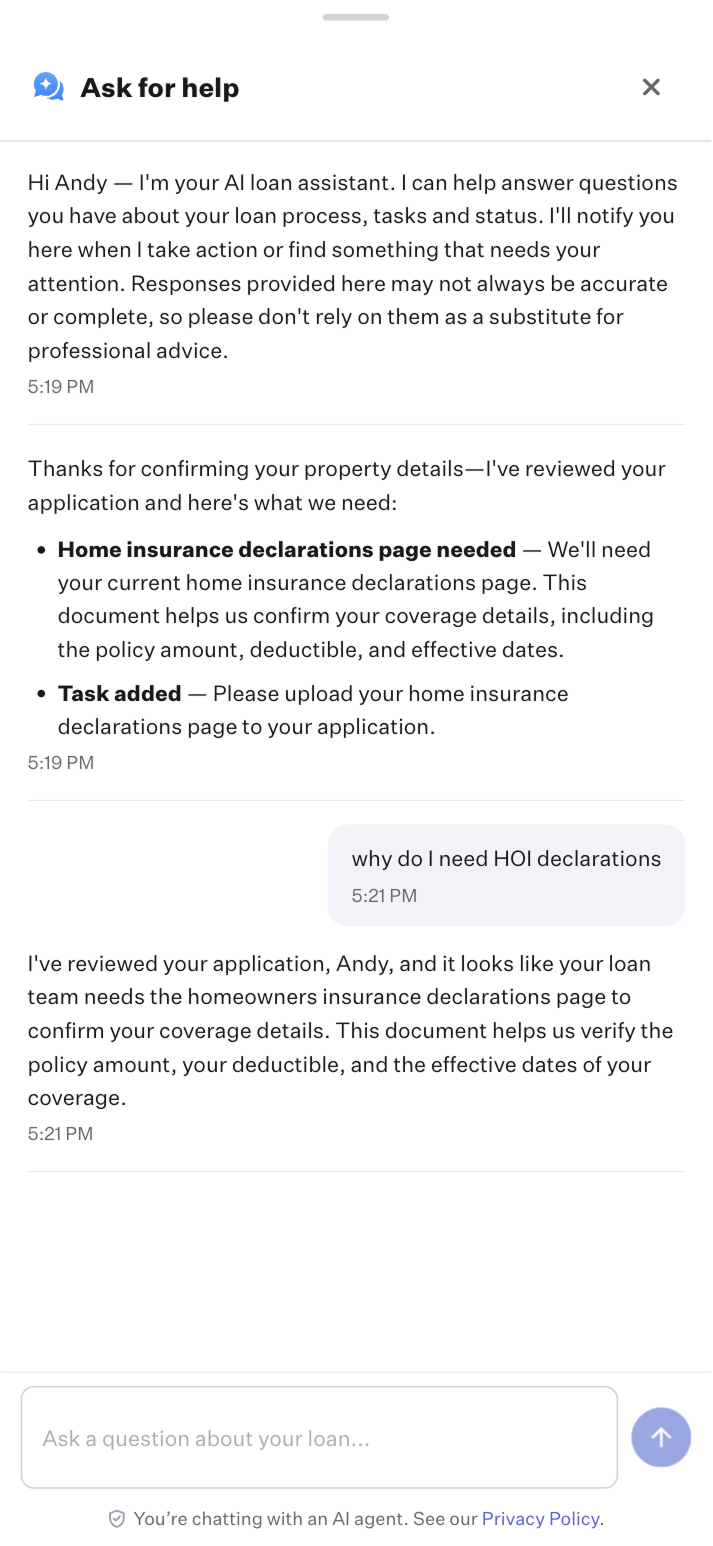

Lenders can now brand and format the borrower chat window

The chat surface itself got more polished and more configurable this week. Lenders can now set the borrower chat widget’s color from the branding configuration, so the assistant’s launcher matches the rest of a lender’s borrower experience instead of standing out as a generic add-on. The launcher itself was refined to sit cleanly in the corner of the page across the loan flow.

Inside the conversation, answers now render as formatted text rather than a single run-on block. When the agent lays out a list of outstanding items or walks through a few steps, the borrower sees a clean, readable list. It’s a small change, but it’s the difference between a wall of text and an answer a borrower can actually scan.

Under the hood: reliability and accuracy improvements

Beyond the headline work, the team shipped a series of reliability and accuracy improvements:

- Runs that finish on time: Autopilot works each loan as a background run, and a run could previously get stuck waiting on a model call that never came back, in one observed case for more than three hours, before anyone knew. Every call the agent makes is now wrapped in a hard time limit, and the connections it uses to reach Blend’s lending services are bounded the same way. A single slow call can no longer stall an entire run, so the agent finishes its pass and reports back predictably.

- Follow-ups never silently dropped: A change to how follow-up creation is handled removes an internal de-duplication step that could, in rare edge cases, swallow a request the agent meant to create.

- Findings stay visible when auto-creation is off: For lenders who run the agent’s application-data review without letting it create follow-ups automatically, the discrepancies it finds are now surfaced for the loan officer instead of being held back.

- Bigger uploads get through: Oversized PDFs are now compressed on upload rather than rejected, so a borrower sending a large scanned statement doesn’t hit a wall. It’s the same instinct behind the TIFF support from Week 12: accept what borrowers actually send.

Under-the-hood improvements ship automatically to every lender with Autopilot activated.

This week was about reach and precision. Autopilot reached the borrower: the chat assistant now speaks to borrowers on Rapid loans with the same grounding it has always had on flagship loans, in a window lenders can brand as their own. And it got more precise about what it asks borrowers, holding back large-deposit requests that never needed asking, and filling in more of the loan file on its own, including rental income and employer details. The week added up to an agent that is more present on more loan types and more careful about the borrower’s time on every one of them.

Blend Autopilot is currently in preview and available at no additional charge during the preview period for all Blend customers. To get started, visit your Lending Config Center or contact your Blend account team.

We publish a new update every Wednesday. Subscribe to the Autopilot weekly update to make sure you stay up to date with everything we are shipping.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

Blend Autopilot Week 13 Update: Autopilot Fills In Verified Assets and Income, Picks Up Unassigned Loans, and Respects Loan Officer Judgment

Autopilot now fills in what it finds. See how the agent does more of the file's actual work.

Read the article about Blend Autopilot Week 13 Update: Autopilot Fills In Verified Assets and Income, Picks Up Unassigned Loans, and Respects Loan Officer Judgment

Blend Autopilot Week 12 Update: The Intelligent Analytics Agent, Self-Serve Capability Toggles, and VA/FHA Production Hardening

More visibility, more control, and more reliability in every loan.

Read the article about Blend Autopilot Week 12 Update: The Intelligent Analytics Agent, Self-Serve Capability Toggles, and VA/FHA Production Hardening

Blend Autopilot Week 11 Update: Rapid, VA, and FHA Continue to Harden, Ongoing Investment in Accuracy, and Verified Income Goes End to End

When upstream income is verified, Autopilot already knows. See what else shipped in week 11.

Read the article about Blend Autopilot Week 11 Update: Rapid, VA, and FHA Continue to Harden, Ongoing Investment in Accuracy, and Verified Income Goes End to End