May 20, 2026 in Blend momentum

Blend Autopilot Week 11 Update: Rapid, VA, and FHA Continue to Harden, Ongoing Investment in Accuracy, and Verified Income Goes End to End

Autopilot Weekly Update: Week 11

The last two weeks were launch weeks. Week 9 brought Autopilot to Rapid Refi and Rapid Home Equity. Week 10 brought VA and FHA guideline support to production. This week was the work that makes those launches matter: a substantially expanded eval framework, deeper hardening across the new loan types, broader borrower data protection, an extension of how Autopilot handles upstream-verified income, and a meaningful expansion of which loans Autopilot can cover.

Rapid, VA, and FHA: continued hardening

The work doesn’t stop at launch. After every new loan type, the agent’s depth grows, the test coverage expands, and the edges get tighter. This week, that continued investment spanned all three of the loan types Autopilot took on in the last two weeks.

For Rapid, additional refinements landed to the agent’s handling of Rapid-specific workflows, deepening the consistency the system already delivers across the Rapid product line.

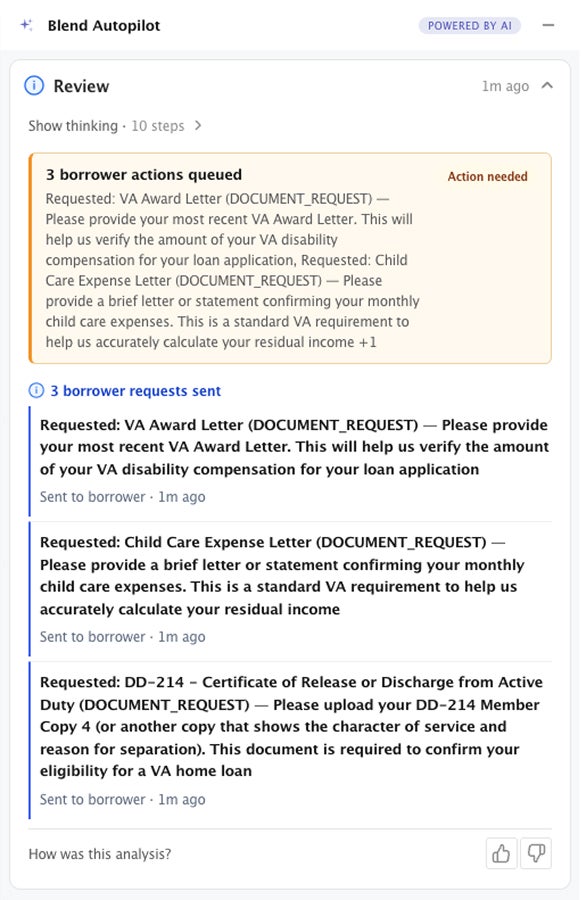

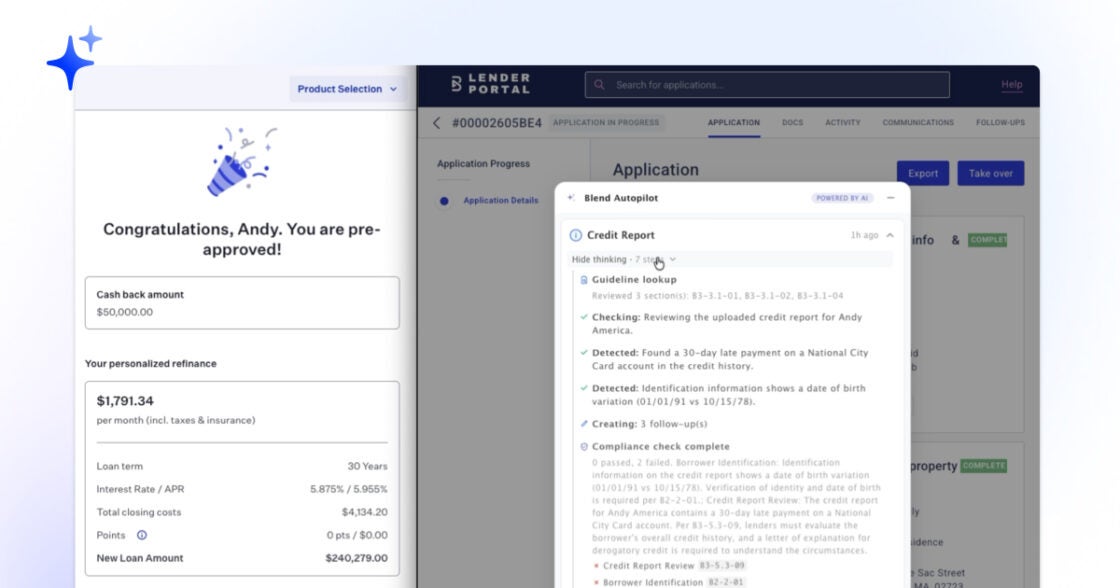

For VA and FHA, the agent reasons against an authoritative version of the FHA Handbook 4000.1 and the VA Lender’s Handbook that is identical across every environment we run. We added a dedicated VA test suite alongside the FHA coverage we already had, so every change to the agent gets measured against VA scenarios before it goes live. And the way our team runs the full accuracy eval on every change was tuned this week as well, with cleaner separation between scenarios and tighter feedback before release.

For lenders running government loans on Autopilot, the system continues to mature week over week, with the rigor of continuous measurement underneath it.

Accuracy as a first-class citizen

Subscribe to Autopilot updates

Accuracy is the product. Every other thing Autopilot delivers, including faster reviews, fewer unnecessary borrower follow-ups, lower-cost operations, and speed to close, depends on it being right.

That is why we have been investing heavily, week after week, in an evaluation framework engineered for the rigor and precision that lending demands. Before any improvement ships, it runs against a growing set of real-world scenarios drawn from the messiest loans we have seen: self-employed borrowers with Schedule C income, VA and FHA files, bundled documents stitched into a single PDF, blank uploads, mistaken uploads, edge-case income structures, and dozens more. After it goes live, it runs again against the live system. Every week, that coverage grows. Every week, the bar moves up.

This week, that framework saw substantial expansion across multiple fronts. We added new regression scenarios for the edge cases real loans throw at us. We normalized document-type naming across every suite, so eval results compare cleanly across runs and across loan types. And we expanded the roster of standardized borrower scenarios that run through every change to the agent.

This is the kind of investment that AI in regulated industries demands. And it is why you will see us sharing more and more of our eval metrics and accuracy performance moving forward, so your risk and compliance teams can see directly how Autopilot is performing on the loans that matter most.

Verified income, end to end

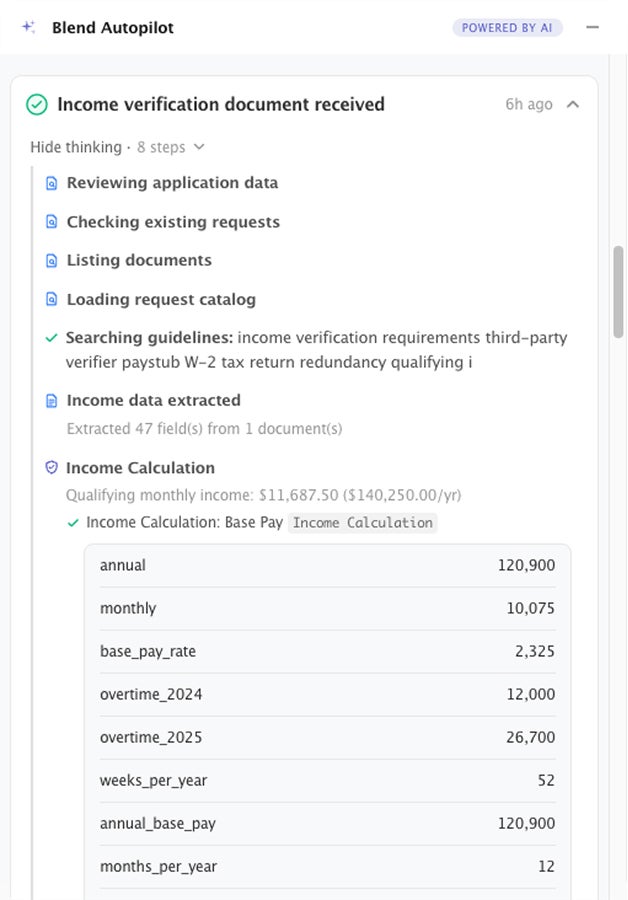

Autopilot has long treated trusted upstream sources as the source of truth for the data they cover. Linked assets are the canonical example: when a lender has verified assets through a trusted aggregator, the agent uses that data directly in its review and skips duplicate document collection. This week, Autopilot extended that same pattern to income.

For lenders using a third-party service to verify borrower income, that verified income is now treated as the source of truth for qualifying income calculations. The agent uses it directly. A new guardrail prevents the agent from re-asking the borrower for paystubs or W-2s on income that has already been verified upstream. Follow-ups that would have been generated absent that verification signal are suppressed before they ever reach the borrower’s screen.

The principle is simple. When a lender has already verified something through a trusted upstream source, the agent should know that and act on it. Less duplicate document collection. Faster path through pre-underwriting. A cleaner experience for the borrower, and one fewer thing for the loan officer to manage.

Borrower data protection deepens

Another week of investment in the layer that filters borrower information out of our internal observability and tracing systems before it ever leaves Blend’s environment.

This week’s work broadened the coverage of that layer across additional data shapes the agent encounters, added production-grade monitoring so we can watch its performance at scale, and extended the test coverage that proves the redaction holds under every condition we can think to throw at it.

This is unglamorous work. It is also the work that has to be right. Each week’s progress is another step toward the discipline that lending demands.

Autopilot’s scope expands to unassigned loans

Until this week, Autopilot’s scope was limited to loans that had a loan officer assigned. Newly submitted applications, loans in transit between LOs, and loans sitting in the queue waiting for assignment all sat outside the agent’s review.

This week, lenders gained the option to extend Autopilot’s coverage to those unassigned loans. With a single configuration change, the agent now picks up unassigned loans the same way it picks up assigned ones. When a document is uploaded, a borrower sends a chat message, or any other loan event fires on the loan, the agent runs its pre-underwriting review, creates the right follow-ups, and updates the borrower’s task list. Borrower chat extends the same way: borrowers asking questions on an unassigned loan get the same conversational experience as borrowers with an assigned LO.

For lenders, the practical benefit is simple. Pre-underwriting can start as soon as the loan starts moving, without waiting on LO assignment.

Under the hood: reliability and workflow improvements

Beyond the headline work, the team shipped a series of quality and reliability improvements:

- Manual asset accounts: Continued tuning of the agent’s handling of manually-entered account information, including borrowers with more than one account on file.

- Wrong-document handling simplified: Last week, Autopilot learned to detect when a borrower uploads the wrong document type. This week, that handling was folded into the agent’s general workflow, so the borrower experience is identical and the system is easier to maintain.

What this week delivered is substantive engineering across every front. The trusted-upstream-source pattern extended cleanly into income. Borrower data protection deepened. Autopilot’s coverage expanded to unassigned loans. And government loan support kept maturing week over week. This is what compounding investment in a regulated AI system looks like, and it is the work that earns trust.

Blend Autopilot is currently in preview and free to activate and use during the preview period for all Blend customers. To get started, visit your Lending Config Center or contact your Blend account team.

We publish a new update every Wednesday. Subscribe to the Autopilot weekly update to make sure you stay up to date with everything we are shipping.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

Blend Autopilot Week 10 Update: VA and FHA Guideline Support, Wrong-Document Detection, and Parallel Validation

Switch loan products mid-stream. Autopilot already knows the rules on the other side.

Read the article about Blend Autopilot Week 10 Update: VA and FHA Guideline Support, Wrong-Document Detection, and Parallel Validation

Blend Autopilot Week 9 Update: Autopilot Now Runs on Rapid Loans, Evaluates LO-Created Follow-Ups, and Refines Borrower Chat

More loan types, less noise. See how Autopilot keeps pace with your volume in week 9.

Read the article about Blend Autopilot Week 9 Update: Autopilot Now Runs on Rapid Loans, Evaluates LO-Created Follow-Ups, and Refines Borrower Chat

Blend Autopilot Week 8 Update: Autopilot Thinks Like an Underwriter, Borrower Chat Ships to Production, and New MCP Capabilities

Less prep work for underwriters. See how Autopilot thinks through AUS findings in week 8 updates.

Read the article about Blend Autopilot Week 8 Update: Autopilot Thinks Like an Underwriter, Borrower Chat Ships to Production, and New MCP Capabilities