July 13, 2026 in Thought leadership

Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

In a stabilizing mortgage market, the lenders who win won't out-rate the competition. They'll out-operate it.

The mortgage market is recovering, but don’t mistake recovery for growth.

The Mortgage Bankers Association projects total single-family origination volume will reach $2.2 trillion in 2026, a modest improvement from an expected $2.0 trillion in 2025.

It’s a market stabilizing, not surging. And in a stabilizing market, lenders who compete for the same loans at the same rates with the same operational models aren’t building a competitive advantage. They’re burning capital just to stay in place.

The real battleground in 2026 isn’t rate. It’s cost per loan.

The mortgage margin problem nobody has solved

After two consecutive years of net production losses, independent mortgage banks returned to modest profitability in 2024, posting an average net income of $443 per loan compared to a loss of $1,056 per loan in 2023, according to the MBA’s Annual Mortgage Bankers Performance Report. On the surface, that’s encouraging. Dig deeper, and the picture gets uncomfortable.

Per-loan production costs hit $12,579 in Q1 2025, according to MBA’s Q1 2025 Quarterly Mortgage Bankers Performance Report, more than 60% higher than the historical average of $7,702 since 2008. Meanwhile, smaller lenders with less than $100 million in production volume posted average losses of over $1,000 per loan. Nearly 42% of mortgage companies in MBA’s sample were still unprofitable when combining production and servicing operations through Q1 2025.

The industry has been here before, stretched thin, searching for efficiency, watching consolidation accelerate. The difference today is that the tools to address the problem have fundamentally changed. The question is whether lenders are willing to use them.

Why the traditional mortgage playbook isn’t cutting costs

For years, the industry has responded to cost pressure with incremental automation: digitize the front-end application, automate some document verification, add a borrower-facing portal. These investments helped, but they didn’t move the structural needle. Industry data suggests the average time to close a mortgage loan still hovers around 38 to 42 days, nearly identical to several years ago.

The reason is architectural. Most lenders have automated individual steps inside a fundamentally disconnected workflow. The transitions between loan origination systems, processing teams, underwriters, compliance reviewers, and closing teams introduce friction at every stage. Every gap is a place where documents stall, exceptions pile up, and costs accumulate.

Freddie Mac’s 2024 Cost to Originate Study quantified the gap starkly: the top 25% of lenders operate at an average cost of $6,900 per loan. The bottom 25% average $16,500. That’s not a rate environment problem. That’s an operational architecture problem, and it’s one that technology was always supposed to solve but never fully has, until now.

The AI advantage lenders can’t afford to ignore

The distinction that matters most in today’s lending landscape isn’t between “digital” and “manual.” It’s between AI that surfaces information (generative AI) and AI that takes action (agentic AI).

Generative AI gave the industry better information retrieval: smarter search, faster summarization, document extraction. But agentic AI does something categorically different. It builds on generative AI capabilities to orchestrate multi-step workflows autonomously, adapts when conditions change, and coordinates across systems and teams without requiring a human to manage every transition.

This isn’t a minor upgrade. It’s the difference between a GPS that shows you the map and one that actually drives the car.

Lenders who have begun deploying agentic AI across their operations, not just in isolated pilots, are starting to see what genuine cost compression looks like. According to Freddie Mac’s updated Cost to Originate analysis, maximizing AI-driven digital capabilities in origination can save lenders up to $1,700 per loan. At scale, across thousands of transactions, that math changes the business model.

Why maximizing volume is no longer enough

There was a time when lenders could absorb high per-loan costs by maximizing volume. The refi boom of 2020 and 2021 masked operational inefficiency across the industry. When volume collapsed, the costs became impossible to ignore.

The MBA is projecting 5.8 million total loan originations in 2026. That’s a market where scale is available, but scale alone won’t protect margins if the cost structure doesn’t change. According to MBA’s Q1 2025 performance data, lenders with low production volume and average loan balances below $250,000 posted average production losses of over $1,300 per loan.

The lenders who will win in this environment are the ones who understand that the market is flat by design, not by circumstance. Rate cuts will unlock pockets of refinance activity. Demographics will support purchase demand. But neither of those tailwinds will rescue an operation spending well above industry averages to close each loan, when top-performing lenders have demonstrated it can be done for significantly less, per the Freddie Mac Cost to Originate Study.

How top-performing lenders are pulling ahead

Top-performing lenders in today’s market share a common orientation. They’re not waiting for volume to return before they invest in operational transformation. They’re investing now, while the market is tight, to build the infrastructure that will let them outperform when volume does pick up.

That investment is increasingly concentrated in AI, not as a departmental tool, but as an enterprise layer that touches every phase of loan fulfillment. From intelligent document processing at application intake, to automated compliance review, to AI-assisted underwriting, to real-time borrower communication, the leaders are rebuilding the loan production workflow from the inside out.

The market opportunity is real. But the companies that capture it won’t do so by waiting for rates to fall. They’ll do it by making each loan they close fundamentally cheaper to originate.

Why 2026 is the moment to close the cost-per-loan gap

A $2.2 trillion market sounds like plenty of runway. And it is, for lenders who’ve built the operational model to compete efficiently at that scale. For those who haven’t, it’s a treadmill where more loans bring more costs and the same razor-thin margins.

Fixing cost per loan isn’t a technology project. It’s a strategic imperative. And the window for acting before the next rate cycle opens is narrowing.

Ready to see how Blend’s AI capabilities can help you reduce cost per loan?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

How Lenders Can Reach More Bilingual Borrowers Without Adding Friction

Bilingual borrowers are a growing market. See how clarity, not just translation, builds confidence and keeps loans moving.

Read the article about How Lenders Can Reach More Bilingual Borrowers Without Adding Friction

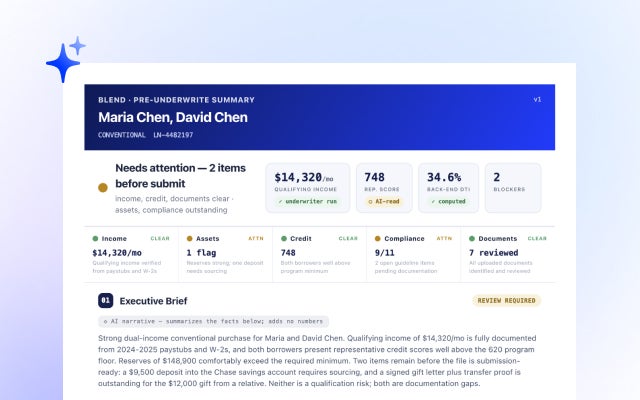

Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Every figure, every source. See how Autopilot's latest update makes pre-underwriting faster to act on.

Read the article about Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Five-Minute Home Equity: How to Outpace Fintechs and Win Member Loans

How credit unions are using AI to close HELOCs in minutes and outcompete fintech lenders.

Watch video about Five-Minute Home Equity: How to Outpace Fintechs and Win Member Loans