June 24, 2026 in Blend momentum

Blend Autopilot Week 16 Update: A First Look at Selective, a New Follow-Up Mode for More Control Over Borrower Requests, and Continued Hardening

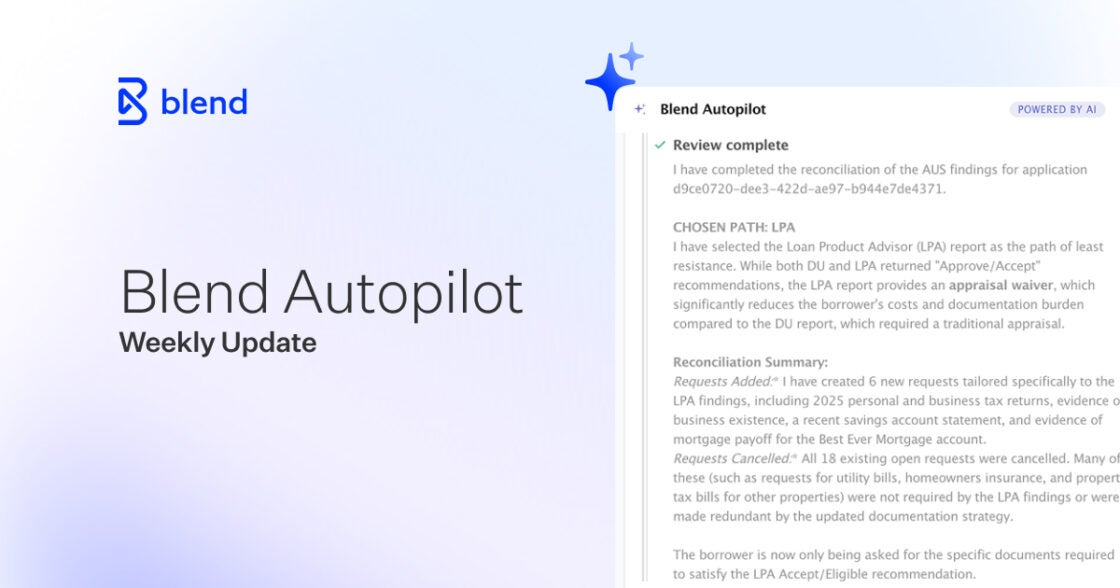

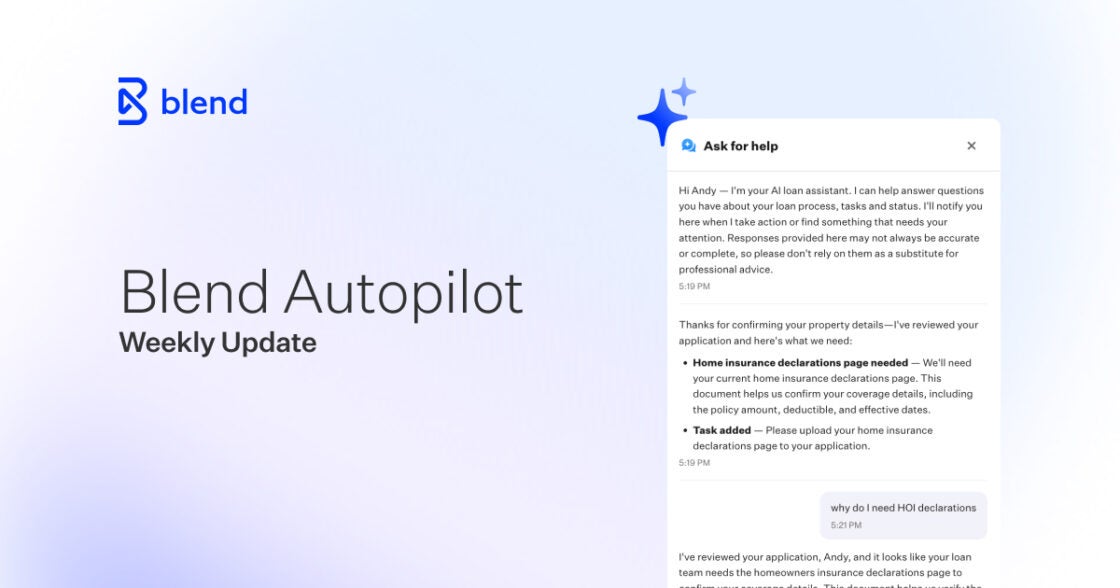

Autopilot Weekly Update: Week 16

Automated follow-ups are one of the most valuable things Autopilot does. When the agent reads a document, assesses income, or checks a file against guidelines and finds something missing, it asks the borrower for it right then.

That matters more than it sounds. More than half of borrower applications come in outside business hours, on nights and weekends, when no loan officer is at a desk to notice the gap and send the request. An agent that can engage the borrower in that moment, build out the needs list, and start working through follow-ups is what moves the file forward faster instead of letting it sit until someone is back at their desk.

It also pulls work to the earliest and least expensive point in the loan rather than letting it surface as late-stage rework, and it compresses the time to clear-to-close. Speed is a direct input to pull-through, and follow-ups are a big part of how Autopilot creates it.

That power comes with another ask from lenders: give us more control over how those follow-ups reach borrowers. An agent eager to be thorough would sometimes ask for an explanation a borrower did not owe, or ask before the file was ready for the question.

This week, we are sharing an early look at what we are building in response: a new follow-up mode, now in active development, that we are excited to make available to you soon.

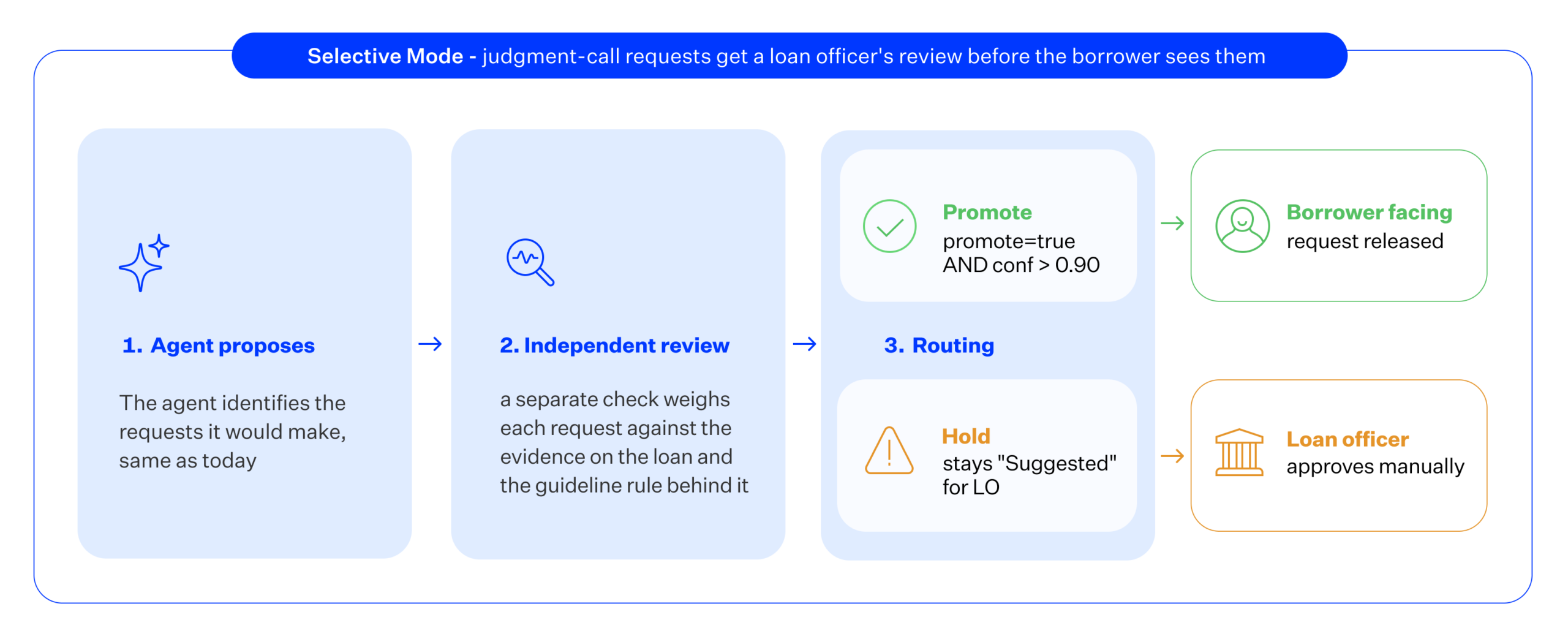

Introducing Selective: a new follow-up mode that sends clearly warranted requests to borrowers and routes judgment calls to the loan officer

Today, when a lender turns on Autopilot’s follow-up generation, it works one way: the agent reasons over the file, infers what it needs from the borrower, and sends those requests directly, so the file keeps moving without waiting on anyone.

That is how it works for every lender using it today, and it is built for coverage, surfacing every need the agent identifies. Selective is a second mode for lenders who want a different posture, one where the borrower receives the requests that are clearly warranted and anything that calls for a loan officer’s judgment is surfaced as a suggestion instead.

Under Selective, every request the agent wants to make passes through a second, independent review before it reaches the borrower. That review looks again at the agent’s reasoning, the evidence on the loan that triggered the ask, and the guideline rule behind it. It separates requests the file clearly supports from the ones that turn on a judgment call.

The clearly warranted requests go straight to the borrower. The judgment calls are routed to the loan officer as suggestions rather than sent to the borrower.

The two modes serve different goals, and neither is more correct than the other. The standard mode is built for coverage: every need the agent identifies goes to the borrower with the least friction for the lender. Selective is built for lenders who want only the well-supported requests reaching borrowers directly, with the more discretionary ones routed to the loan officer as suggestions instead.

It is a choice the lender makes based on how they want Autopilot to engage their borrowers.

Either way, nothing the agent finds is lost. The loan officer still sees every proposed follow-up, including the ones Selective holds back as suggestions, and can send any of them to the borrower in one step.

Under Selective, the borrower simply hears the requests that are clearly warranted. For the borrower, that is fewer letters of explanation to write and fewer documents to chase. For the loan officer, it is a follow-up queue they can trust.

Selective is lender-controlled. It is a mode the lender’s admin selects in the same place every other Autopilot capability lives, with no deployment and no integration work. A lender who wants the agent to send every follow-up it identifies keeps the standard mode. A lender who wants the judgment calls brought to the loan officer first switches to Selective.

The control sits with the lender, loan by loan.

Selective came straight from what customers told us they needed, and we are excited to put it in their hands soon. It is the clearest expression yet of where Autopilot is headed: an agent that is not just capable of engaging borrowers directly, but trusted to.

Autopilot hardening continues across follow-ups and borrower requests

Alongside the bigger work, the team keeps hardening the agent’s everyday precision, one rule at a time, on a single principle: do not put an ask in front of a borrower the file does not actually support.

It is steady, continuous work, and it means fewer needless requests reaching borrowers every week. Several more of these fixes shipped this week, live now for every lender with Autopilot activated.

- A borrower who has come off the loan is no longer chased: When a borrower is removed from an application, Autopilot stops generating follow-ups addressed to them rather than asking someone who is no longer party to the loan to produce documents.

- Documents the lender already obtained do not trigger borrower asks: When a lender’s own team has supplied a document directly, the agent recognizes it is already handled and does not turn around and ask the borrower for the same thing.

- A follow-up the loan officer cancelled stays cancelled: If a loan officer deliberately cancels a request and nothing about the underlying data has changed, the agent no longer re-issues it on the next pass.

- A signed disclosure is not requested again: When a borrower adopts a signature once and it is applied across several documents, Autopilot reads those as validly signed instead of flagging the reused signature and asking for it again.

- Co-signed debts are questioned only when they actually matter: The agent now asks for proof that someone else pays a co-signed debt only when that debt is genuinely being excluded from the borrower’s ratios, not as a reflex.

- U.S. citizens are not asked for residency paperwork: A fix at the data layer means the agent reads citizenship status correctly and stops asking citizens for documents meant for non-citizens.

Subscribe to Autopilot updates

Each of these is the agent declining to send an ask that is not warranted, so fewer of them ever reach the borrower.

This week came down to a single principle: the requests that are clearly warranted belong with the borrower, and the ones that call for judgment belong with the loan officer.

That is the control customers asked us for, and it is what Selective will put in their hands as a new follow-up mode built directly from their feedback. It is also what the team shipped by hand this week, one rule at a time, so the agent stops chasing borrowers who have left the loan, re-asking for documents already in hand, and questioning what the file does not support.

As Autopilot moves toward general availability, the work is about making the agent not just capable, but trusted to engage borrowers with precision, and that trust is built one well-judged ask at a time.

Blend Autopilot is currently in preview and available at no additional charge during the preview period for all Blend customers. To get started, visit your Lending Config Center or contact your Blend account team.

We publish a new update every Wednesday. Subscribe to the Autopilot weekly update to make sure you stay up to date with everything we are shipping.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

Blend Autopilot Week 15 Update: Sharper Underwriting Precision, Stricter Document Checks, and a Fuller Rapid Loan Picture

Fewer false flags, stricter document checks. See all that Autopilot refined in week 15.

Read the article about Blend Autopilot Week 15 Update: Sharper Underwriting Precision, Stricter Document Checks, and a Fuller Rapid Loan Picture

Blend Autopilot Week 14 Update: Borrower Chat Comes to Rapid Loans, Smarter Large-Deposit Requests, and a Loan File That Fills In More of Itself

Rapid loans now get the full borrower chat experience. See what else shipped in week 14.

Read the article about Blend Autopilot Week 14 Update: Borrower Chat Comes to Rapid Loans, Smarter Large-Deposit Requests, and a Loan File That Fills In More of Itself

Blend Autopilot Week 13 Update: Autopilot Fills In Verified Assets and Income, Picks Up Unassigned Loans, and Respects Loan Officer Judgment

Autopilot now fills in what it finds. See how the agent does more of the file's actual work.

Read the article about Blend Autopilot Week 13 Update: Autopilot Fills In Verified Assets and Income, Picks Up Unassigned Loans, and Respects Loan Officer Judgment