November 2, 2021 in Thought leadership

MBA Annual 2021: Key strategies for a borrower-first roadmap

Blend President Tim Mayopoulos shared his insights on why putting the customer first matters now more than ever, post-pandemic.

In-person events are back, and the team at Blend joined the Mortgage Bankers Association Annual 2021 in San Diego this October.

In addition to hosting a booth where we connected with customers and hosted demos, Blend President Tim Mayopoulos took to the stage for the Innovation & Tech Track: Pandemic Innovation panel with key industry leaders.

The panel members discussed the pandemic’s impact on the financial services sector and how innovation and technology played crucial roles in increasing convenience, building confidence, and deepening relationships between businesses and their customers.

The discussion initially focused on innovations each panelist’s organization adopted to provide products and services to customers digitally. They then shared insights about the permanent shakeup caused by the pandemic and what financial services leaders should think about as they shape their digital strategy to better serve their borrowers moving forward.

As leaders at financial firms build their digital roadmap for 2022, here are four key insights to consider from this thoughtful conversation.

1. Provide the why to borrowers through education

One key topic the panelists covered is that mortgages are complicated, and consumers need more education about and visibility into the journey from start to finish. When borrowers understand the why — for example, the reason why certain documents are required over others or complexities behind rules — it can provide clarity and calm nervousness or frustration.

Shelley Leonard, EVP, chief product and digital officer at Black Knight, highlighted the importance of providing this education to consumers. Leonard suggested easy-to-access explainer videos or other materials that make it easier and more intuitive for consumers to understand what they’re signing or why they have to turn in a certain document.

Teri Pansing, vice president, corporate closing at Fairway Independent Mortgage Corporation, noted that it’s important for loan officers and others in the network to have the “what to expect” conversations with customers early on in the process. This gives lenders the opportunity to set the stage so that customers can understand the application and closing processes.

2. A hybrid approach to meeting customer expectations

Some aspects of the homeownership process are completely digital while others may require an in-person interaction — and more likely, it’s a combination of both.

As the panelists discussed, the industry has improved its digital presence, and while consumers may understand that this hybrid process is necessary, they also expect the experience to be seamless.

Lenders can start this transformation by identifying gaps between their digital and traditional mechanisms. The panel noted key areas that were historically challenging for lenders and where technology could improve efficiencies for their consumers. For example, borrowers who shared their personal information digitally shouldn’t have to fill out the same documents or have to re-authenticate their identities in person. They expect to be able to pick up where they left off to complete the transaction at hand.

Lenders may be able to close some of these gaps by implementing new technologies that can help eliminate manual processes. This saves time, which means lenders can focus on maximizing in-person interactions to deliver the highest value for customers.

3. Keep costs low for the borrower

As Tim mentioned in the panel, he believes that digitization is all about convenience for the consumer. But lenders should also think through how to lower costs for the consumer, including those related to transactions, such as the cost of originating the loan itself.

Similar to how consumers can now self-serve throughout much of the mortgage process, thanks to the technology improvements of the past decade, loan officers and other internal key team members can also benefit from quality of life improvements. Access to modern, digital-friendly back-office tools can drive increased efficiency and faster processing — and ultimately, save lenders money on a per-loan basis. These benefits can be passed back to the consumer, buoying loyalty by demonstrating a commitment to customer-first lending.

4. Leverage data and artificial intelligence to focus on high-value interactions

Finally, the panelists discussed how an industry movement in a digital direction is an opportunity for lenders to leverage data and AI. The ultimate aim is to be more predictive in how they are servicing customers.

A more predictive approach can help lenders with customer retention. When lenders understand more about what a customer needs and when, they can move quickly to engage them when they want to refinance, for example.

Using predictive analytics to gauge whether a customer is considering a refinance or even looking for a new home opens up new opportunities for lenders to engage and retain customers.

The pandemic has already proven that financial organizations can raise the bar for higher efficiency, shorter wait times for application processing and closing, and embracing a more proactive customer life cycle. But this is just the start.

What strategies does your team have in place to put the borrower first?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

How Lenders Can Reach More Bilingual Borrowers Without Adding Friction

Bilingual borrowers are a growing market. See how clarity, not just translation, builds confidence and keeps loans moving.

Read the article about How Lenders Can Reach More Bilingual Borrowers Without Adding Friction

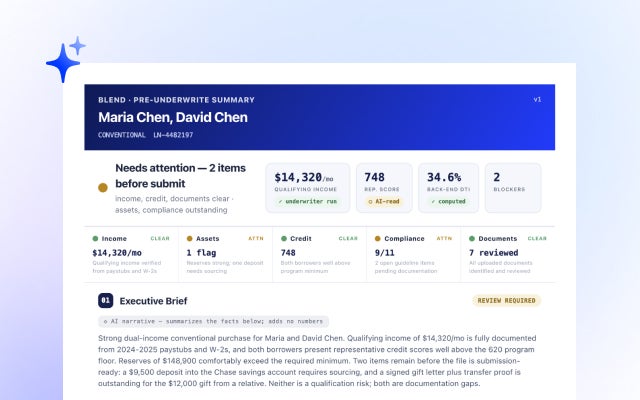

Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Every figure, every source. See how Autopilot's latest update makes pre-underwriting faster to act on.

Read the article about Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

The mortgage market is projected to reach $2.2 trillion in 2026, but flat isn't the same as easy. With per-loan costs exceeding $12,500, discover why cost per loan is the…

Read the article about Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan