April 13, 2026 in Thought leadership

Embedded Insurance Infrastructure: A Blueprint for Reducing Loan Fallout

Homeowners insurance friction is one of the most overlooked drivers of loan fallout, and embedded infrastructure is how modern lenders are solving it.

There is a quiet deal-killer hiding inside the modern mortgage process. It does not show up in your pipeline reports as a line item. It does not get flagged in QC reviews. But it is costing lenders deals every single day, and the borrowers who walk away never fully understand why.

Homeowners insurance has become one of the most disruptive friction points in the origination journey. And for most lenders, the workflow built around it has not fundamentally changed in decades.

Why rising insurance premiums are now a mortgage origination problem

Over the past six years, homeowners insurance premiums have risen more than 40%. In 2024 alone, premiums climbed approximately 11.5%, pushing the national average annual premium to roughly $2,800. In high-risk states like Florida, California, and Texas, the situation is considerably more acute, with some carriers exiting markets entirely and leaving borrowers scrambling to find coverage at any price.

The downstream consequences for mortgage lenders are direct and measurable. A premium higher than expected can shift a borrower’s debt-to-income ratio past qualification thresholds. Sticker shock at the insurance stage can introduce doubt and hesitation into a process where momentum is everything. And in the most difficult markets, the simple inability to find coverage at all can kill a transaction that was otherwise ready to close.

Yet even setting aside market volatility, the operational reality of how insurance gets handled inside most origination shops is ripe for modernization. The process is largely manual, largely offline, and almost entirely dependent on the borrower figuring things out on their own.

How the insurance shopping experience is quietly killing your pipeline

Consider what a borrower typically experiences today. They spend weeks providing their lender with detailed personal and financial information: income, assets, employment history, property details. Then, somewhere in the middle of the process, they are told to go find homeowners insurance.

What follows is an entirely separate journey. They search online, re-enter the same information they already gave their lender, and receive quotes, or they don’t, depending on their location. If they land on an aggregator site, they consent to contact and within hours are fielding calls from a dozen different carriers, all while their loan officer, real estate agent, and home inspector are already competing for their attention.

Eventually they find a policy, bind it, and try to get the declaration page to their processor. Except the processor needs a specific format, or the deductible does not meet GSE guidelines, or the coverage limits are insufficient. And the chase begins again.

Research from Stratmor Group puts a clear number on what this friction costs lenders from a relationship perspective: the single biggest driver of declining NPS scores among mortgage borrowers is being asked for the same information twice. Insurance, in its current form, asks borrowers to do exactly that, repeatedly.

This is not a technology problem waiting to be invented. It is an integration problem waiting to be solved.

Embedded insurance: What it actually means for mortgage lenders

The term “embedded” gets used liberally in fintech, often as shorthand for any digital experience that incorporates a service. But embedded infrastructure, particularly in the context of insurance, means something more specific and more consequential.

True embedding means the insurance workflow is not a detour. It is not a referral link or a contact card with a few agent names. It is a native task inside the origination flow, powered by data the borrower already provided, surfacing options already calibrated to GSE requirements, and delivering verified evidence of insurance directly back into the loan file.

Done correctly, embedded insurance infrastructure changes the calculus for everyone in the transaction. For the borrower, it eliminates redundancy. For the loan team, it eliminates the chase. For the lender organization, it eliminates a category of fallout that has historically been treated as unavoidable.

The cost-to-originate case for automating insurance

Mortgage lenders are under significant pressure to reduce the cost to originate, which currently ranges between $11,000 and $13,000 per loan industry-wide. Approximately 75% of that cost is tied to personnel. Every manual task a processor or underwriter performs, every call to chase a document, every re-review of a non-compliant policy, is a direct draw on that personnel budget.

Insurance, handled the old way, is one of the most labor-intensive and least-automated steps in the origination process. Handling it with native, automated infrastructure is one of the highest-leverage operational improvements a lender can make without restructuring the entire business.

The math is straightforward. If insurance-related friction contributes to even a fraction of current loan fallout, and if the average funded loan represents meaningful revenue to your organization, then reducing that fallout by several percentage points has real bottom-line consequences. The operational improvement is not just about saving deals. It is about redirecting skilled people toward work that requires their expertise and away from work that should have been automated years ago.

Why GSE compliance must be built into the quoting layer

Any conversation about embedding insurance into the mortgage workflow has to address compliance head-on, because it is the first objection most lending leaders raise.

If borrowers are selecting insurance through the portal, how do lenders know the coverage actually meets investor requirements? How do they know deductibles are within acceptable limits and that policies are GSE-aligned?

The answer lies in how the underlying quoting logic is constructed. An insurance infrastructure solution built specifically for the mortgage channel should have compliance baked into its core logic. GSE alignment should not be a manual review step performed after the fact. It should be the framework within which quotes are surfaced in the first place.

This shifts the conversation significantly. Instead of asking “how do we review what the borrower chose?” the question becomes “how do we ensure what we show the borrower is already within guidelines?” These are fundamentally different ways of operating, with very different downstream consequences for re-review rates and processing time.

How Blend and Covered deliver a native insurance workflow inside the borrower portal

This is precisely the problem that Blend and Covered Insurance have partnered together to solve.

Inside the Blend borrower portal, homeowners insurance is a native task, not a detour. At the right moment in the borrower’s journey, typically after initial disclosures and intent to proceed, the insurance task surfaces automatically. The borrower does not re-enter any data. Blend pre-populates relevant information from the application and, in partnership with Covered’s network of over 65 carriers, returns the top five most affordable quotes for that specific property.

The borrower compares options, selects a policy, and answers a focused set of coverage and discount questions, all without leaving the portal. No parallel Google search. No aggregator opt-in. No flood of unsolicited calls.

Once the borrower selects a quote, a single W-2 licensed advisor from Covered’s dedicated mortgage team reaches out to finalize the policy. Rather than a carousel of competing insurance agents, one dedicated person handles the relationship from quote to close. That advisor understands exactly where the borrower is in the mortgage process and what is required to close. Evidence of insurance then flows directly back through Blend and syncs into the LOS.

For the loan team, the experience is equally clean. Coverage options are filtered through GSE-aligned logic from the start, and lenders can incorporate their specific investor requirements to reduce re-reviews on the back end. Lenders already on the Blend platform can be configured in a test environment within a day, with a go-live timeline driven entirely by lender readiness. The solution is also highly configurable and can be toggled on or off at the loan officer or branch level, allowing lenders to preserve existing agent relationships in the markets where they have them while expanding coverage options everywhere else.

Why 2026 is the year to fix your insurance workflow

The mortgage market is showing signs of meaningful recovery heading into 2026. Lenders who have spent the last two years tightening operations now have an opportunity to translate that efficiency into competitive advantage as volume returns.

Insurance is not a side issue in that environment. It is a conversion factor. Lenders with a modern, embedded, borrower-friendly insurance workflow in place will close more of the deals they start, with less manual effort, fewer fallouts, and stronger borrower relationships on the other side.

The infrastructure is ready. The integration is proven. The only question is whether this is the cycle your organization chooses to treat insurance as a strategic part of the origination workflow rather than a step left for borrowers to navigate on their own.

Want to reduce loan fallout caused by insurance friction?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

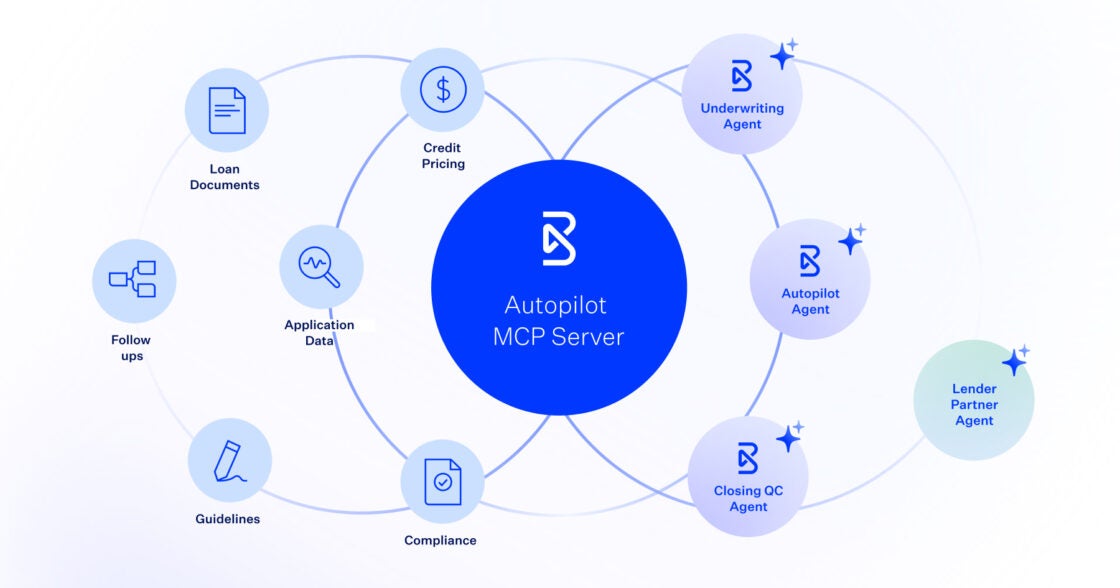

Blend Autopilot Week 5 Update: Autopilot MCP Server Ships, Opening the Full Lending Platform to AI Agents

One connection. Full platform access. Here's what Autopilot MCP means for your institution.

Read the article about Blend Autopilot Week 5 Update: Autopilot MCP Server Ships, Opening the Full Lending Platform to AI Agents

Next-Level Growth: Closing the Execution Gap in 2026

Join Blend, Cornerstone Advisors and, People First FCU, as they operationalize the findings of the Next-Level Growth: Credit Union Opportunities in a Changing Market report.

Watch video about Next-Level Growth: Closing the Execution Gap in 2026

Blend Autopilot Week 4 Update: Borrower Chat Is Coming, API-Uploaded Documents Now Visible to Autopilot, and Smarter Cross-Document Analysis

Real adoption, real feedback. See how lenders are shaping what Autopilot has become this week.

Read the article about Blend Autopilot Week 4 Update: Borrower Chat Is Coming, API-Uploaded Documents Now Visible to Autopilot, and Smarter Cross-Document Analysis