September 27, 2022 in Mortgage Suite

Economic forces favor growth for home equity lending

Macroeconomic forces in the US suggest home equity lending is a long-term opportunity for lenders.

Rising interest rates are creating economic headwinds for both lenders and borrowers alike. But, as in any storm, there can be some favorable tailwinds as well. An unprecedented level of home equity has been building in recent years, and it now presents lenders with an exceptional long-term opportunity to tap into the potential of the home equity lending market. According to the Federal Reserve, U.S. home equity values reached a stratospheric $27.8 trillion in Q1 2022 compared to $17.5 trillion in Q1 2018. That’s a compound annual growth rate (CAGR) of 12.3%¹. With homeowners sitting on record home equity, lenders find themselves with an exceptional long-term opportunity to increase their exposure in the home equity lending market.

Entering the home equity lending market creates strategic advantages for financial institutions (FIs). They can expand existing borrower relationships as well as gain new customers that they might not have otherwise acquired. Further, an FI with existing mortgage borrowers obtains an instant customer market for homeowners needing to expand or renovate. For an FI’s overall lending business, this creates a flywheel effect for cross-selling opportunities that drive customer lifetime value.

¹Source: Federal Reserve Bank

Homeowners are remaining in place long term

Rising interest rates and high home prices are convincing existing homeowners to adopt a strategy of stay, borrow, and renovate. Even the work-at-home trend bodes well for home equity lending as stay-at-home employees need funds for additional rooms or home office space with accompanying furnishings and equipment. Another favorable condition to spurring a need for home renovation funding is rising food and fuel prices, meaning that households will travel less and spend more time at home. These scenarios will generate the borrower demand that should incentivize financial institutions (FIs) to be active home equity lenders.

Another home equity lending tailwind is the aging U.S. housing stock, a key leading indicator of the remodeling and renovation needs of homeowners. The National Association of Home Builders states that the median age of U.S. homes is 39 years, with the Northeast region skewing higher in the range of 55 – 60 years old.

The dual tailwinds of record home equity values and aging home infrastructure will underpin medium and long-term opportunities for the home equity lending market. Even the current rising interest rate environment will not reduce home equity demand since home-changing and mobility options for households has diminished. Existing homeowners are deterred from buying a primary or seasonal home due to the surge in home prices. Funding house renovation through home equity loans is on a fast-tack growth path.

Traditional financial institutions aren’t the only ones noticing these trends. They already face intense competition from digitally native fintechs in the home equity lending market. Many lenders are now offering favorable rates and terms to borrowers along with periodic promotional offers. This will stimulate more demand for home equity lending and create higher application volume. Many lenders need to step up their game to offer the right delivery channels and provide the personalized customer experience that digitally savvy borrowers require. FIs that have fallen behind in market share must modernize, enabling delivery that meets the needs of consumers while positioning effectively against digitally native competition. How to get there remains the most pressing question.

Lenders can leverage existing technology for home equity lending

Financial institutions with mortgage lending operations can leverage technology to quickly develop or expand their home equity lending. Financial institutions should seek out vendors offering solutions with cloud-based architecture. Cloud benefits include cost savings and scalability to manage cyclical variations of loan application volume. Additionally, AI technology with accompanying machine learning algorithms brings loan processing productivity, faster decisioning, and risk management for loss prevention.

Home equity lending platforms deliver long-term strategic success for FIs

FIs that use leading home equity loan origination platforms can gain economies of scale and systems alignment when they:

- Meet emerging demand for home equity loans. Homeowners are staying in place and renovating homes as mobility options decrease. Remote and hybrid work schedules have become accepted work routines causing households to need more space.

- Enhance customer experience. Borrowers will recognize and become loyal to FIs that deliver consistency and personalization throughout the lending process. Digital engagement with customers maintains and extends relationship banking.

- Diversify their loan portfolio. As mortgage application volume decreases, offering another home lending product helps to insulate the FI’s business from economic cycles and changing consumer borrowing preferences. The right loan origination software can manage several types of home loans from a single platform.

- Optimize revenue opportunities with technology. Leading solutions from vendors with cloud and AI platforms bring financial improvements and favorable return-on-investment (ROI) results for core lending operations.

Lenders that invest in home equity lending solutions make an investment in their long-term strategic success. The solutions they choose must be agile, resilient, and versatile to meet the continually changing forces on the financial services landscape. Economic conditions dictate the ebb and flow of different loan products. Having advanced lending technology prepares a lender to offer the right loan products aligned with borrower demand.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

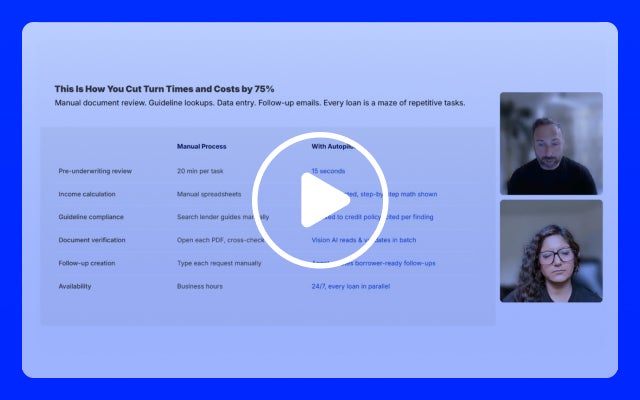

MBA Power Hour: Optimizing the Loan Originator Workflow – Blend Autopilot

Watch a live demo of Blend's Autopilot and see how AI automates the loan originator workflow around the clock.

Watch video about MBA Power Hour: Optimizing the Loan Originator Workflow – Blend Autopilot

The Intelligent Lending Playbook

How AI agents are redefining mortgage origination. From borrower experience to loan officer productivity.

Start learning about The Intelligent Lending Playbook

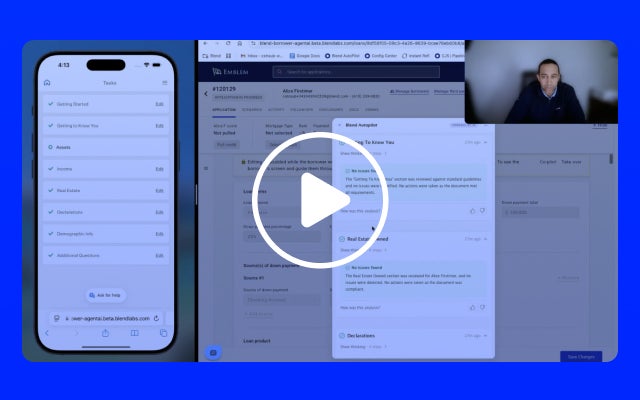

Home Equity Is the Proving Ground: How Digital-First Origination Will Define the Next Era of Lending

Speed is winning home equity. See how digital origination helps your institution compete.

Watch video about Home Equity Is the Proving Ground: How Digital-First Origination Will Define the Next Era of Lending