August 11, 2020 in Mortgage Suite

How a fintech mortgage solution provides an end-to-end digital experience

For mortgage lending, fintech solutions do more than digitize the process. See how Blend’s platform provides an unparalleled end-to-end experience.

With lenders looking to differentiate in an increasingly competitive space, the need to modernize the mortgage experience is critical. Rather than relying on internal resources, some lenders are tapping into the partnership that fintech in mortgage lending can provide. Fintech mortgages provide the digital infrastructure to help banks simplify the data collection process, enabling them to offer a differentiated customer experience while lowering their mortgage servicing costs.

Using fintech in mortgage lending can lead to higher application completion rates, faster closings, and more satisfied customers. Here’s a closer look at what a fintech mortgage is and the benefits fintech mortgage servicing can offer to both consumers and lenders.

What is a fintech mortgage solution?

While many lenders today are using digital front ends, fintech lending is more than just digitizing processes. Rather, a fintech mortgage helps lenders build better partnerships with borrowers thanks to faster, more streamlined experiences. It speeds up data collection, supports borrowers with better communication, and eliminates unnecessary steps along the way.

Here are some key benefits of Blend’s fintech mortgage solution:

- Increases efficiency. Blend’s data-driven workflows eliminate unnecessary steps while automating tasks associated with conditioning, fulfillment, and closing. It supports your team in providing a best-in-class customer experience throughout the lending process.

- Reduces fragmentation. Fintech mortgages replace the fragmented, siloed solutions of traditional lending with an integrated, end-to-end digital solution. This results in greater productivity and efficiency, along with shorter loan cycle times and faster closes.

- Better experiences, higher revenues. A faster, more streamlined application process means customers may be more likely to complete a given task, which benefits the lender in terms of the number of applications completed and funded.

What does an end-to-end digital mortgage look like?

Unlike traditional multichannel solutions, fintech lending solves the puzzle of fragmented lending practices. From W2s to contracts to appraisals and titles, a digital end-to-end mortgage helps to cut manual data gathering steps out of the process, allowing customers to complete applications more quickly and efficiently with an automated mortgage experience.

Here’s what the digital mortgage process with Blend might look like:

- A borrower begins a mortgage application over their smartphone, online, or in person at the branch.

- As the borrower works through the application, they have the option to connect directly to their asset, payroll, and tax accounts. There’s no need to access paperwork buried in a file.

- If the borrower stops the application, they can pick up exactly where they left off on any channel that’s convenient to them, whether online or off.

- As the borrower works through the application, fields are pre-filled for them from previously provided answers and connected accounts, eliminating unnecessary manual steps.

- If the borrower has questions, the application interface provides real-time help at any point during the process, and LOs are just a tap away thanks to the Co-pilot feature.

- And lastly, the borrower is able to complete and approve steps digitally with e-signatures. No need to run to the bank to sign papers.

Digital mortgage lending is more than just digitizing processes. Rather, it’s about creating efficiency at every step of the application process, leading to a more pleasant application process and a better experience for the customer.

How is reporting improved by a fintech mortgage solution?

Better reporting is also a benefit of fintech lending. Traditional reporting and business metrics look at things like percentage of applications submitted, pull-through tracking for applications taken, and the number of loans closed and funded.

While these metrics are important, fintech solutions also provide a bigger picture. They allow lenders to learn about consumer behavior, what they’re saying about the application, NPS, and what percentage of people are connecting their assets. Armed with this valuable information, lenders can use this data to further refine and optimize the borrower experience.

Blend’s new suite of loan data analytics tools includes a Reporting Dashboard, Interactive and Generated Reports, and the Reporting API. These powerful tools can give you the insights you need to plan intelligently and act quickly.

What makes Blend different?

At Blend, we’re committed to providing end-to-end digital mortgages, all the way from application to close. Our unified platform offers automated approval after application and many system integrations, including product and pricing, fees, and automated underwriting systems.

Currently, we have over 230 lenders partnering with us. Our customers report that up to 89% of their borrowers submit applications they started in Blend. Customers are also experiencing a reduction of up to seven days from the average loan cycle and up to 67% year-over-year loan volume increases.

“The idea that we could have a mortgage loan where we didn’t have to ask for pay stubs or asset statements was such an idyllic, blue-sky type of mind-blowing concept. But a month after implementation, that’s exactly what was happening. When you get to that point, you approve a mortgage in 48 hours.”

Jay Romanovsky

Director of IT Systems, Affinity Federal Credit Union

Hear Affinity Federal Credit Union’s story

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

How Lenders Can Reach More Bilingual Borrowers Without Adding Friction

Bilingual borrowers are a growing market. See how clarity, not just translation, builds confidence and keeps loans moving.

Read the article about How Lenders Can Reach More Bilingual Borrowers Without Adding Friction

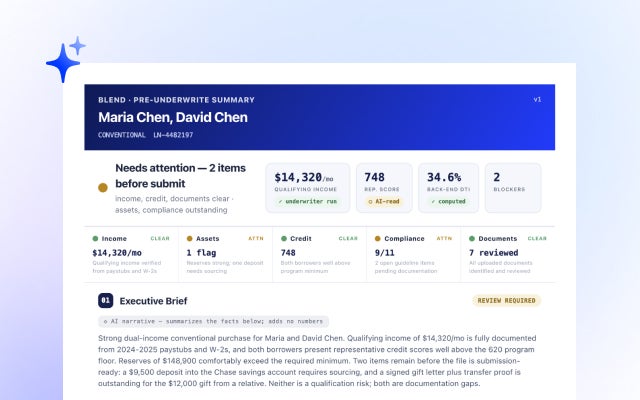

Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Every figure, every source. See how Autopilot's latest update makes pre-underwriting faster to act on.

Read the article about Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

The mortgage market is projected to reach $2.2 trillion in 2026, but flat isn't the same as easy. With per-loan costs exceeding $12,500, discover why cost per loan is the…

Read the article about Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan