February 8, 2023 in Thought leadership

How partnering with a fintech for home equity can accelerate modernization

Banks that partner with a fintech for home equity loans can reduce bottlenecks and streamline the closing process.

When the leadership team at BMO Harris Bank decided to grow the company’s home equity assets, they realized that they had to take a modernized approach. Providing an individually digitized product experience for a subset of their consumers wasn’t enough. Instead, they needed portfolio-wide digital transformation.

“We needed to grow our mortgage business beyond what our bankers could do,” said Sean D’Esposito, director of product transformation at BMO Harris Bank. “We knew we weren’t getting our fair share digitally, and we knew that we needed some capabilities in that realm to grow our overall market share.”

The team at BMO Harris Bank chose a fintech solution to help it achieve its goals — and with impressive results. “[W]e’ve reduced mortgage and home equity cycle times by over five days,” said Tom Parrish, director of consumer lending product management.

4 ways fintech partnerships are modernizing the home equity process

BMO Harris Bank isn’t alone in its decision to use a fintech solution. Eighty-nine percent of financial services providers say that fintech partnerships are important to their business today, up from 49% in 2019.

Why is this? As BMO Harris Bank has witnessed, in part because fintechs are using the cloud to help financial services organizations handle higher volumes of home equity loans while reducing operational costs. Let’s explore four ways fintech home equity partnerships are helping financial firms achieve this.

1. Fast adoption of digital capabilities

The challenge: Digitalization can be time- and cost-intensive for a financial institution to achieve on its own, often requiring a team of IT experts — and a degree of experimentation to get right.

The solution: Adopting cloud-based digital technologies via a fintech partnership enables financial institutions to outsource their IT problems, which can help them deploy a solution and enjoy the benefits of digital more quickly. Faster adoption of digital is an imperative as financial providers seek to meet rising consumer demands. In fact, research suggests that 81% of applicants prefer online loan solutions.

2. Fewer bottlenecks

The challenge: Applying for a home equity loan can be a lengthy process that is sometimes fraught with bottlenecks. Filling out paper-based forms, verifying identities, and sourcing documentation from different places is time-consuming and frustrating — and can lead to high application abandonment.

The solution: Financial providers can streamline processes with a cloud-based solution delivered by a fintech provider, saving staff and their clients precious time. Many of the steps involved in applying for a home equity loan can be completed digitally, which can speed up the process. For example, applicants may be able to connect directly to their asset, payroll, and tax accounts. They may also not have to re-enter information they’ve provided in the past, thanks to data pre-fill functionality.

3. Anywhere access

The challenge: Historically, applicants have had to enter a branch to apply for a home equity loan.

The solution: With fintech solutions delivered via the cloud, applicants can apply for a loan online at their own convenience. They can also start an application on one device, save their progress, and finish it on another device later, seamlessly picking up exactly where they left off.

4. Streamlined closing

The challenge: Many financial institutions still require their clients to enter a branch to finalize the application process. This is frustrating for customers, who increasingly expect a seamless experience from application to close.

The solution: The right fintech home equity solutions delivered via the cloud can enable lenders to meet these changing expectations — and expedite the closing process at the same time. For example, lenders can automate document preparation and offer a remote signing room integrated right within the platform.

Looking towards a modern future in home equity

Through its fintech partnership, BMO Harris Bank achieved the improved delivery of home equity they were after while modernizing across product lines.

“We’re able to do things much more efficiently like collecting documentation with ease,” said Parrish. “Less back and forth with our processors, underwriters, and customers is critical to our ongoing success as we grow consumer lending profitably.”

As a result, it has realized a 253% increase in digital home equity applications — and this is just the start.

“[W]e believe it’s going to continue to evolve so that customers will be doing the majority of the processing and the majority of the closing with very little human touch,” said Mark Shulman, head of consumer lending at BMO Harris Bank.

Want to find out more about BMO Harris Bank’s fintech approach to home equity lending?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

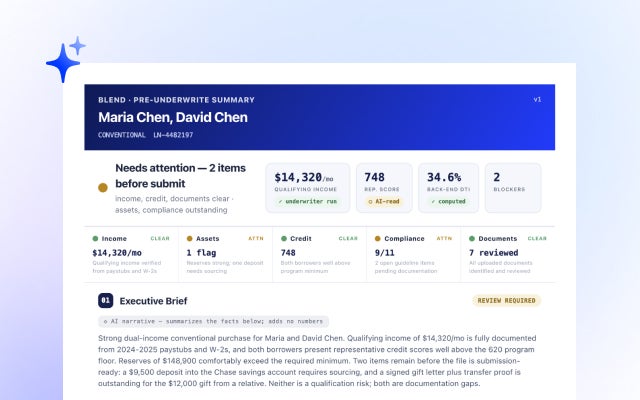

Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Every figure, every source. See how Autopilot's latest update makes pre-underwriting faster to act on.

Read the article about Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

The mortgage market is projected to reach $2.2 trillion in 2026, but flat isn't the same as easy. With per-loan costs exceeding $12,500, discover why cost per loan is the…

Read the article about Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

Five-Minute Home Equity: How to Outpace Fintechs and Win Member Loans

How credit unions are using AI to close HELOCs in minutes and outcompete fintech lenders.

Watch video about Five-Minute Home Equity: How to Outpace Fintechs and Win Member Loans