October 29, 2020 in Challenges and solutions

Blend has you covered for the new URLA

Over the last five years, Uniform Residential Loan Application (URLA) changes have brought both challenges and opportunities for financial institutions.

Back in 2016, the Federal National Mortgage Association (FNMA) and the Federal Home Loan Mortgage Corporation (FHLMC), jointly referred to as government-sponsored enterprises (GSEs), announced that they would be making substantial changes to the format, content, and structure of the Uniform Residential Loan Application (URLA), also known as the 1003 mortgage application.

Although the URLA is designed to significantly streamline the mortgage lending process, the roll out has been anything but straightforward. The new URLA changes were postponed three times over the better part of five years, due in part to the impact of COVID-19. Its use became mandatory as of March 1, 2021 for loans purchased by the GSEs. We understand how confusing the transition has been for financial services organizations, so let’s unpack the change

What is URLA, and what is the reason for the changes?

The URLA is a standard form that many mortgage lenders in the U.S. use to assess a borrower’s creditworthiness when applying for a home loan. The URLA requests information about a customer’s employment, income, assets, debts, and the property the customer is looking to purchase.

The changes to the URLA were a long time coming. According to the FNMA, this was the first significant modification of the form in over 20 years.

In addition to supporting the industry’s wider move toward digitization, the URLA changes aimed to help lenders more effectively obtain the most relevant loan application information to deliver an easier, consumer-orientated loan application experience.

What changes were made to the URLA?

The changes to the URLA were designed to make the experience more consumer-friendly, enable better efficiency, and support accurate data collection. According to the FNMA press release and a GSE fact sheet, the updates help borrowers and lenders in several key ways:

- Clearer upfront instructions support borrower self-service and reduce reliance on the lender.

- The format redesign helps borrowers navigate the form more easily and facilitate better data collection.

- Obsolete fields are removed from the form, and new and updated fields are designed to obtain the loan application information that both the GSEs and government require.

Back in 2016, the Federal National Mortgage Association (FNMA) and the Federal Home Loan Mortgage Corporation (FHLMC), jointly referred to as government-sponsored enterprises (GSEs), announced that they would be making substantial changes to the format, content, and structure of the Uniform Residential Loan Application (URLA), also known as the 1003 mortgage application.

Keep in mind that the loan application process has not changed for the lender or borrower. The changes support the collection of loan application details that are relevant and useful in making an underwriting decision.

The benefits of a standardized application

By maintaining a standardized mortgage application, the GSEs are helping everyone benefit in a number of ways. Standardized applications are:

- More consumer friendly, since borrowers have a consistent experience every time they take out a mortgage loan.

- Easier for LOs to navigate, since they need to input the same data every time — this improves efficiency.

- Helping to improve access to capital, since it is easier for lenders to exchange information with the GSEs.

At Blend, we recognize how important these benefits are for our financial services customers. We are committed to better banking for all, and we can help achieve that by committing to driving positive change through our technology.

Blend’s commitment to our customers

Blend’s approach to the URLA changes reflects our wider philosophy to adapt quickly and effectively to new market requirements. We can’t predict the future, but we can help you be better prepared for it.

With continuous improvement as a priority, we will enable our customers to have access to the latest banking software that helps them navigate the industry’s twists and turns.

Looking to learn more about Blend?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

How IMBs Are Redefining Profitability Without Growing Headcount

The average cost to originate a loan sits above $11,000 while profitability per loan has compressed to $853. The IMBs holding margin right now are not solving that with more…

Read the article about How IMBs Are Redefining Profitability Without Growing Headcount

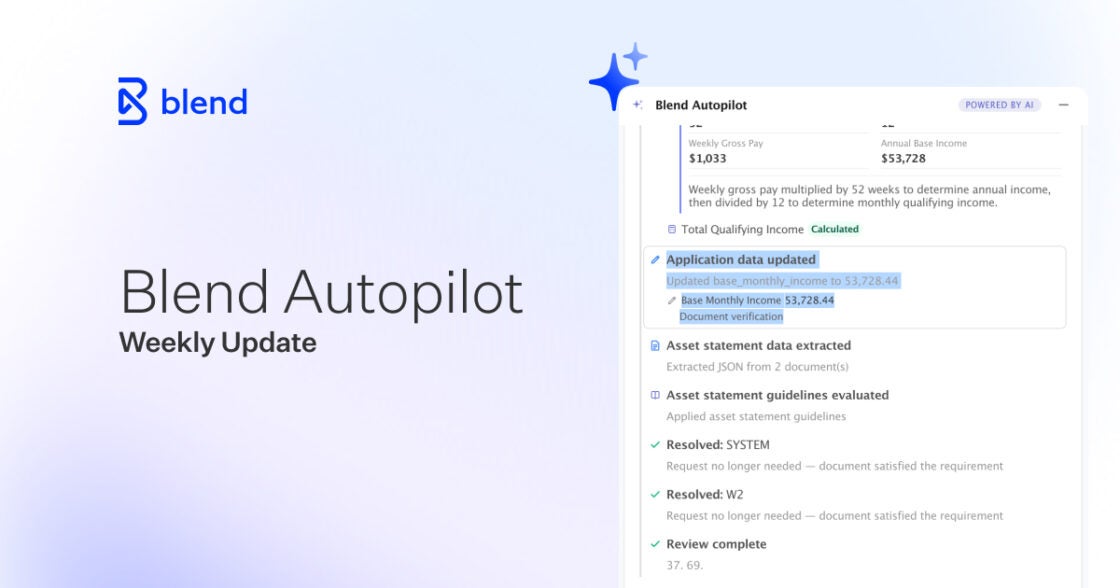

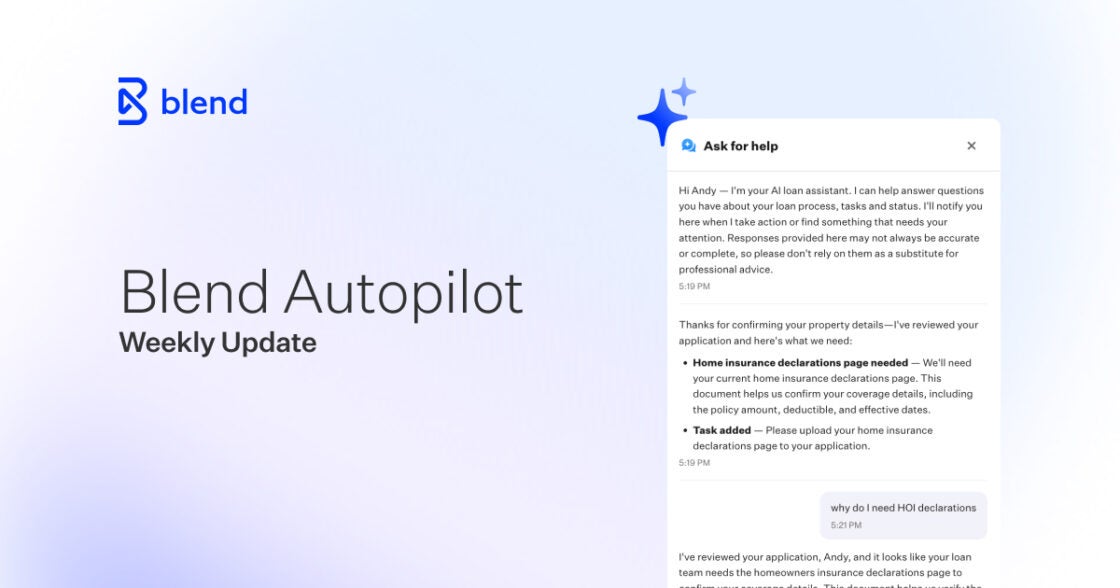

Blend Autopilot Week 14 Update: Borrower Chat Comes to Rapid Loans, Smarter Large-Deposit Requests, and a Loan File That Fills In More of Itself

Rapid loans now get the full borrower chat experience. See what else shipped in week 14.

Read the article about Blend Autopilot Week 14 Update: Borrower Chat Comes to Rapid Loans, Smarter Large-Deposit Requests, and a Loan File That Fills In More of Itself

Blend Autopilot Week 13 Update: Autopilot Fills In Verified Assets and Income, Picks Up Unassigned Loans, and Respects Loan Officer Judgment

Autopilot now fills in what it finds. See how the agent does more of the file's actual work.

Read the article about Blend Autopilot Week 13 Update: Autopilot Fills In Verified Assets and Income, Picks Up Unassigned Loans, and Respects Loan Officer Judgment