April 29, 2026 in Blend momentum

Blend Autopilot Week 8 Update: Autopilot Thinks Like an Underwriter, Borrower Chat Ships to Production, and New MCP Capabilities

Autopilot Weekly Update: Week 8

AUS findings just met their match.

DU findings land on a loan. Seconds later, Autopilot has extracted every condition, checked which ones are already satisfied by documents on file, and updated the borrower’s needs list. Then LPA findings arrive. Autopilot reads those too, compares both reports, and picks the path that asks the least of the borrower.

That’s the headline this week: Autopilot now reads and acts on automated underwriting findings the way an experienced underwriter does. Not just parsing a single report, but reasoning across both DU and LPA, checking what’s already been validated, and making sure borrowers only get asked for what’s actually needed. Alongside that, borrower chat moves to production environments this week, and the MCP platform continues to expand.

Autopilot now reads AUS findings like an underwriter

When a loan is submitted to Desktop Underwriter (DU) or Loan Product Advisor (LPA), the results come back dense: numbered findings, conditions, validation results, appraisal waiver offers, and cross-references to specific guideline sections. Interpreting those findings requires deep knowledge of Fannie Mae and Freddie Mac guidelines, plus context from every document already on the loan.

Under the hood, Autopilot coordinates specialized sub-agents for different types of analysis. When AUS findings are uploaded, Autopilot delegates the work to a sub-agent built specifically for findings reconciliation. That sub-agent works in two steps.

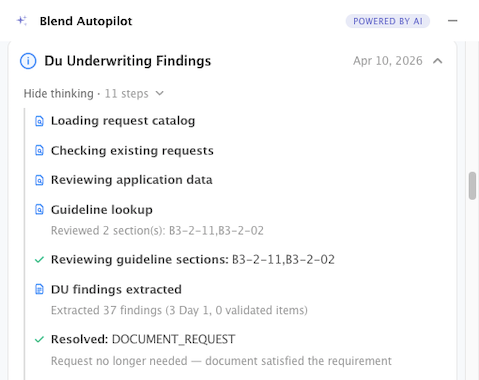

Step 1: Structured extraction

Autopilot reads the full AUS report and extracts every numbered finding, every validation result, and the recommendation. This isn’t summarization. Every finding is captured verbatim with its section, MSG ID, Day 1 Certainty tags, and full conditional text. A typical report has 10-20+ findings. Autopilot gets all of them.but going back and making the core experience better. The summary that underwriters open on every loan is now faster to scan, clearer about what needs action, and structured around how lenders actually work. Every agent intelligent improvement ships automatically to every lender with Autopilot activated. No upgrade cycles. No implementation projects.

Step 2: Reconciliation

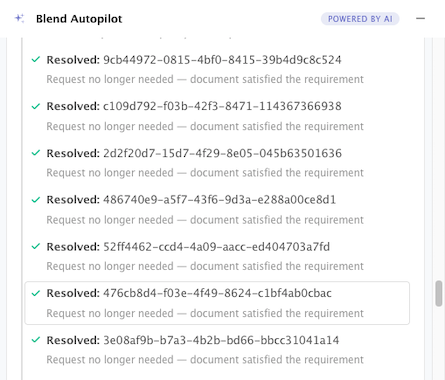

With the structured findings in hand, Autopilot reconciles them against the loan. For each finding, it classifies the action required: is this something the borrower needs to provide? Something the lender handles? Or purely informational? Then it checks what’s already on file.

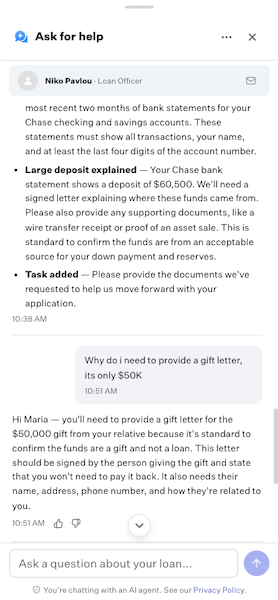

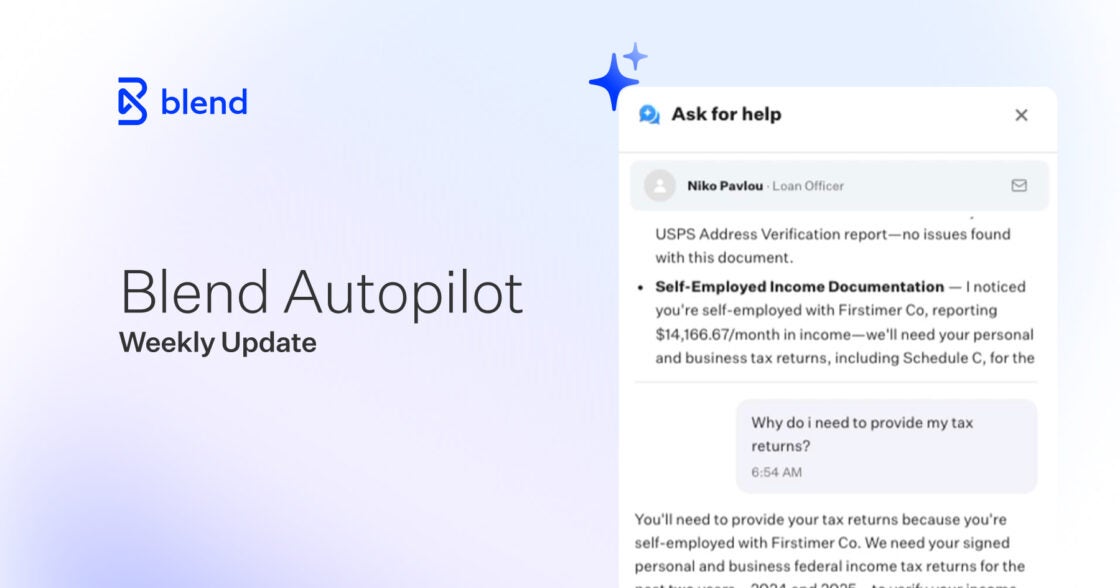

A condition about employment verification might already be satisfied by a W-2 the borrower uploaded last week. A bank statement showing sufficient reserves might cover an asset condition. Autopilot makes those connections automatically, so borrowers aren’t asked for something that’s already been provided.

For findings that do require borrower action, Autopilot creates follow-up requests in plain language. Not “LPA findings require evidence of revolving account payment inclusion in DTI,” but “We need a recent statement for your Emblem Mortgage account showing your monthly payment. This helps us make sure all your bills are accounted for.”

Validation awareness

Both DU and LPA include validation services: Day 1 Certainty (Fannie Mae) and AIM (Freddie Mac). When an item is marked “Validated,” it means the system has already confirmed it. No additional documentation needed.

Autopilot checks these validation results before requesting anything. If Day 1 Certainty validated a borrower’s employment at a specific employer, Autopilot won’t request W-2s or paystubs for that employer. If AIM validated an asset account, it won’t request bank statements for that account. Validation is matched to specific employers and accounts, not applied as a blanket rule.

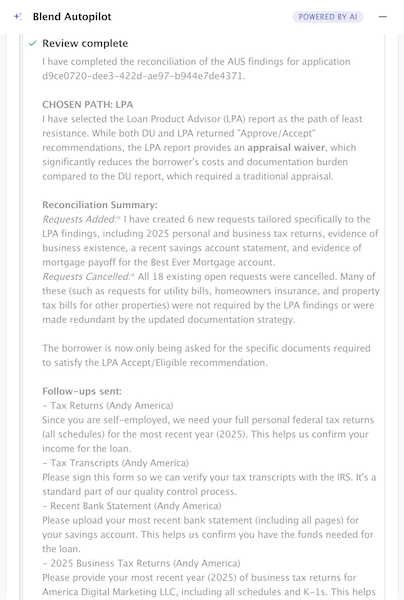

Dual-report comparison

When both DU and LPA results are available on the same loan, Autopilot compares them side by side and picks the path of least resistance for the borrower.

It compares across five dimensions: recommendation strength (Approve vs. Refer), appraisal waiver availability (a PIW or ACE offer can save the borrower $400-600+ and weeks of waiting), number of borrower-actionable conditions, validation coverage (more validated items means fewer documents needed), and documentation requirements.

Autopilot picks the stronger path, explains why, and tailors the borrower’s needs list to that report. Requests that were only needed under the non-chosen path get cancelled.

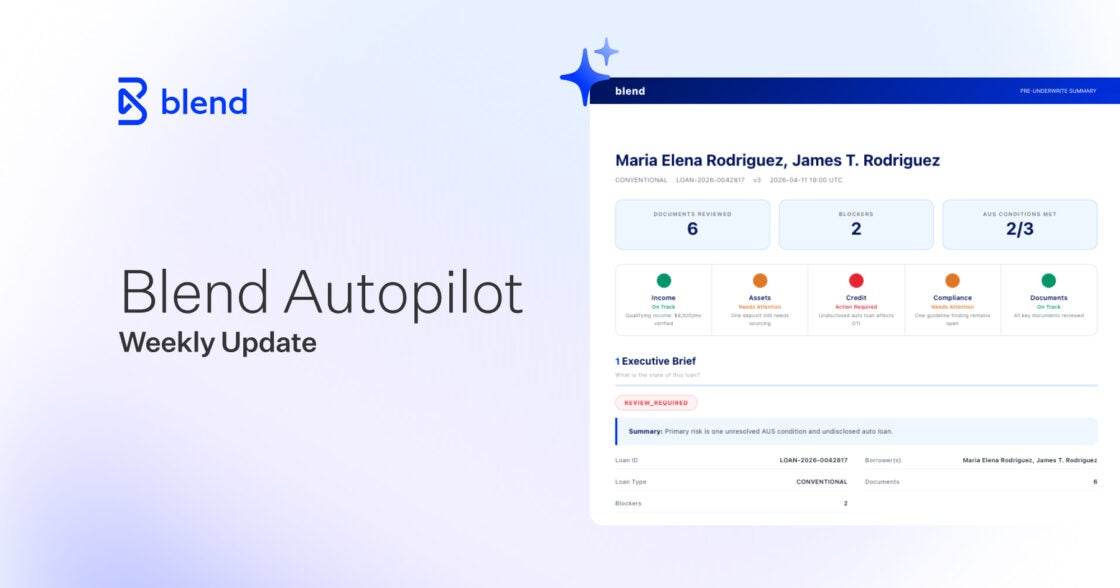

For underwriters, this means the gap between “AUS results received” and “conditions reviewed and actioned” drops to seconds. Autopilot handles the prep work: extracting findings, cross-referencing documents, and tailoring the needs list. The underwriter still reviews every recommendation and makes every credit decision. They just start from a clean, organized picture instead of a raw findings report.

Borrower chat moves to production environments

Borrower chat launched in beta last week. This week, it moves to production. The team has already released a series of improvements based on real-world usage during the beta period.

Smarter compliance filtering

The compliance filter was being too aggressive in its first week, deflecting legitimate borrower questions that happened to touch on sensitive-adjacent topics. The team narrowed the filter scope so it catches what it should (rate guarantees, legal advice, discriminatory language) without blocking normal loan questions. Off-topic redirects are also preserved correctly now. If a borrower asks about something unrelated to their loan, they get a gentle redirect instead of a compliance wall.

Richer proactive notifications

Proactive messages are now anchored to the specific document and event that triggered them. Instead of a generic “We’ve reviewed your documents,” borrowers see messages tied to exactly what happened: which document was reviewed, what was found, and what (if anything) they need to do next. When a loan officer triggers a proactive notification, the framing correctly reflects that it came from their team.

AI-generated, personalized welcome back

The welcome-back experience for returning borrowers is now fully AI-generated and personalized instead of template-driven. When a borrower comes back after time away, Autopilot catches them up on exactly what happened while they were gone, based on the actual state of their loan, not a canned message.

Accurate task counts

Borrowers now see correct task counts across all tools, and data is properly scoped to the right borrower on joint applications. Co-borrowers only see their own tasks and documents.

Secure Input

The team added additional safeguards against system prompt extraction attempts and prompt injection via uploaded documents. Graceful fallback responses ensure borrowers always see a clean experience, even when adversarial input is detected.

Subscribe to Autopilot updates

New MCP tools

Preapproval letter generation. Agents can now generate and send preapproval letters directly through MCP. No manual export, no switching between systems.

Document deletion. Agents can permanently remove documents from a loan file when needed.

LOS number lookup. Agents can retrieve the LOS number for any loan, bridging the gap between Blend and external loan origination systems.

Guardrails

Workflow creation caps. Rate limits now prevent runaway or abusive workflow creation through the MCP server.

Document download rate limiting. A separate rate limit for document downloads prevents bulk extraction attempts.

Audit logging on schema discovery. Calls to the schema discovery tools are now logged, giving lenders visibility into how agents explore the platform.

Under the hood: performance and reliability improvements

- Concurrent event processing: The core workflow engine now processes events concurrently instead of sequentially. When multiple documents arrive on a loan at once, they’re reviewed in parallel.

- Higher worker capacity: Temporal worker capacity increased from three to 10 activities per worker, keeping throughput ahead of adoption growth.

- Gemini context caching: Borrower chat now uses Gemini’s context caching, reducing latency and cost on repeated conversations within the same session.

- Automatic Gemini retries: Transient Gemini errors (503s, 429 rate limits) are now retried automatically, so borrowers don’t see failures from temporary provider issues.

- Smarter question routing: When a borrower asks “why do I need to provide this?”, the chat now routes the question to the right tool to explain the specific task, rather than giving a generic answer.

- Streaming reliability: Cleaner handling when the LLM refuses during review generation, and a fix for thought rendering on Python 3.11+.

Autopilot is getting deeper. Not just reviewing more document types, but reasoning the way underwriters do: reading AUS findings, checking what’s already validated, comparing reports side by side, and making sure borrowers only get asked for what’s actually needed. Autopilot keeps getting better every week. No upgrade cycles. No implementation projects.

Blend Autopilot is currently in preview and free to activate and use during the preview period for all Blend customers. To get started, visit your Lending Config Center or contact your Blend account team.

We publish a new update every Wednesday. Subscribe to the Autopilot weekly update to make sure you stay up to date with everything we are shipping.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

Blend Autopilot Week 7 Update: Borrowers Can Now Talk to Autopilot and MCP Platform Hardening

Borrowers get answers. Underwriters get clarity. See all that Autopilot shipped in week 7.

Read the article about Blend Autopilot Week 7 Update: Borrowers Can Now Talk to Autopilot and MCP Platform Hardening

Blend Autopilot Week 6 Update: A Redesigned Pre-Underwriting Summary, MCP Platform Expansion, and Smarter Follow-Up Creation

Your Pre-Underwriting Summary just got a serious upgrade. Here's what changed.

Read the article about Blend Autopilot Week 6 Update: A Redesigned Pre-Underwriting Summary, MCP Platform Expansion, and Smarter Follow-Up Creation

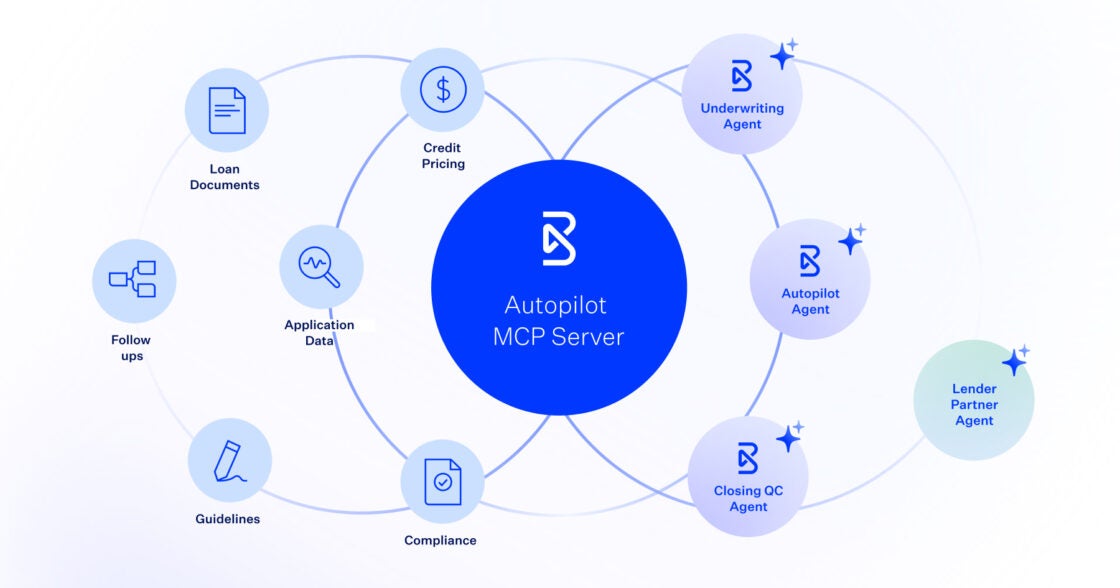

Blend Autopilot Week 5 Update: Autopilot MCP Server Ships, Opening the Full Lending Platform to AI Agents

One connection. Full platform access. Here's what Autopilot MCP means for your institution.

Read the article about Blend Autopilot Week 5 Update: Autopilot MCP Server Ships, Opening the Full Lending Platform to AI Agents