April 27, 2026 in Thought leadership

Where AI Belongs in the Mortgage Origination Lifecycle

Apply AI differently across borrower experience and fulfillment so you can cut cost per loan, shorten cycle times, and improve loan quality.

For most lenders, the question is no longer whether to use AI but where to put it so that it actually moves the numbers that matter, including cost per loan, cycle time, and loan quality.

That question is harder than it sounds. Most AI investments in mortgage have followed the same pattern of identifying a painful task, layering a model on top of it, and measuring activity instead of outcomes. The result is a collection of point solutions that don’t compound and a cost structure that hasn’t meaningfully changed.

The lenders seeing different results have taken a different path, in that they stopped asking what AI can do and started asking where in the origination lifecycle a specific kind of intelligence actually belongs. That distinction, more than the technology itself, is what separates the organizations scaling AI from the ones still running pilots.

Two workflows, two different jobs

Before the point-of-sale handoff, the job is speed: meet the borrower where they are, capture a complete file, keep them moving. The cost of a mistake here is a callback or a re-upload.

After the handoff, the job is precision: verify everything, reconcile discrepancies, satisfy investor guidelines, produce an audit trail that holds up under examination. The cost of a mistake here is a buyback or a post-close defect.

Same loan file, completely different mandates. A system optimized for one will make tradeoffs that are unacceptable for the other.

The model that works: two agents, one flow

The architecture that’s working in production isn’t a single AI model bolted onto existing workflows. It’s two purpose-built agents operating on shared data, with a clean handoff between them.

An edge agent at the point of sale

A well-designed point-of-sale agent activates the moment a borrower takes an action, with no manual trigger and no batch processing overnight. When a document lands, the agent is already working.

That means parsing W-2s, tax returns, bank statements, and paystubs against the applicable guideline set, whether Fannie Mae, Freddie Mac, lender overlays, or fully custom rules, with findings cited to the specific guideline reference, not just a pass/fail flag. Income calculation runs in the same pass. For self-employed borrowers, that means depreciation add-backs, business expense deductions, and multi-year averaging, with a step-by-step breakdown showing the formula, inputs, and result for every calculation step.

When something is missing, the follow-up should be specific. Not “please provide additional documentation,” but the exact dollar amount, the specific document, the entity involved, and a plain-language explanation of what’s needed and why.

And the agent should be applying contextual reasoning, not threshold rules: a payroll direct deposit that exceeds the large-deposit threshold doesn’t need a Letter of Explanation if the agent can identify the source. Credit inquiries consistent with rate-shopping during an active refinance don’t need to be flagged.

That kind of contextual reasoning can reduce unnecessary follow-ups by up to 50% compared to rules-based automation, which matters because every unnecessary follow-up is friction for the borrower and noise for the loan officer.

The standard to aim for is simple. By the time the file leaves the point of sale, it should be pre-reviewed, pre-validated, and effectively pre-underwritten. A clean, decision-ready file, not a partially complete package for fulfillment to triage.

A core agent inside the LOS

In fulfillment, the agent isn’t working with the borrower anymore, and the job shifts entirely.

A well-designed fulfillment agent classifies incoming documents, routes them correctly within the loan file, and maps extracted data directly into the loan application and underwriting engine, eliminating manual data entry at the point of ingestion. When data in one document contradicts another, the agent flags the discrepancy, resolves it where deterministic resolution is possible, and escalates complex items with full context attached.

Condition clearing runs automatically against DU and LPA results. Third-party verifications for income, employment, assets, and appraisal trigger without manual orchestration. Tasks that can run in parallel do, because ordering an appraisal while verifying income shouldn’t require a human to sequence that.

Compliance monitoring runs continuously, not at post-close audit, so when fees or data points change, TRID and HMDA checks run automatically. If DTI shifts during processing, the system flags it immediately rather than surfacing it three weeks later.

Every agent action should be recorded inline with the loan’s existing audit history, with full reasoning attached. The question “why did the system do that” should take seconds to answer, not hours. That’s not just a compliance requirement, it’s the baseline for any AI that’s going to operate inside a regulated lending workflow.

The key design principle is that this agent needs to be built into the system of record from the ground up, not retrofitted onto a legacy LOS. The data models and core workflows have to be designed for AI operation, and when they are, the agent compounds, and each new capability builds on the same foundation rather than requiring its own integration.

The handoff: where most AI value gets lost

The handoff between POS and fulfillment is where data quality degrades and rework accumulates. Processors re-verify documents already reviewed, and loan officers re-key data that already exists somewhere else. Time and cost disappear into a gap that most lenders have accepted as inevitable.

It doesn’t have to work that way. When the edge agent produces structured, validated output, including the pre-underwriting summary, compliance findings, income calculations, and application data, and that output flows into the fulfillment agent via a native API, the handoff tax goes away.

The fulfillment agent picks up exactly where the edge agent left off, running cross-document reconciliation, condition clearing, third-party triggers, and task orchestration across the fulfillment team, all starting from a pre-underwritten file rather than a raw application.That’s where the cost-per-loan improvement compounds.

The question of where AI belongs in the origination lifecycle is only half the challenge. The other half is knowing how to evaluate whether a given AI solution actually performs across your full pipeline, not just a vendor-curated sample. To find out more about the questions IMBs should ask in every AI vendor conversation, read The Question IMBs Should Be Asking Before Their Next AI Investment.

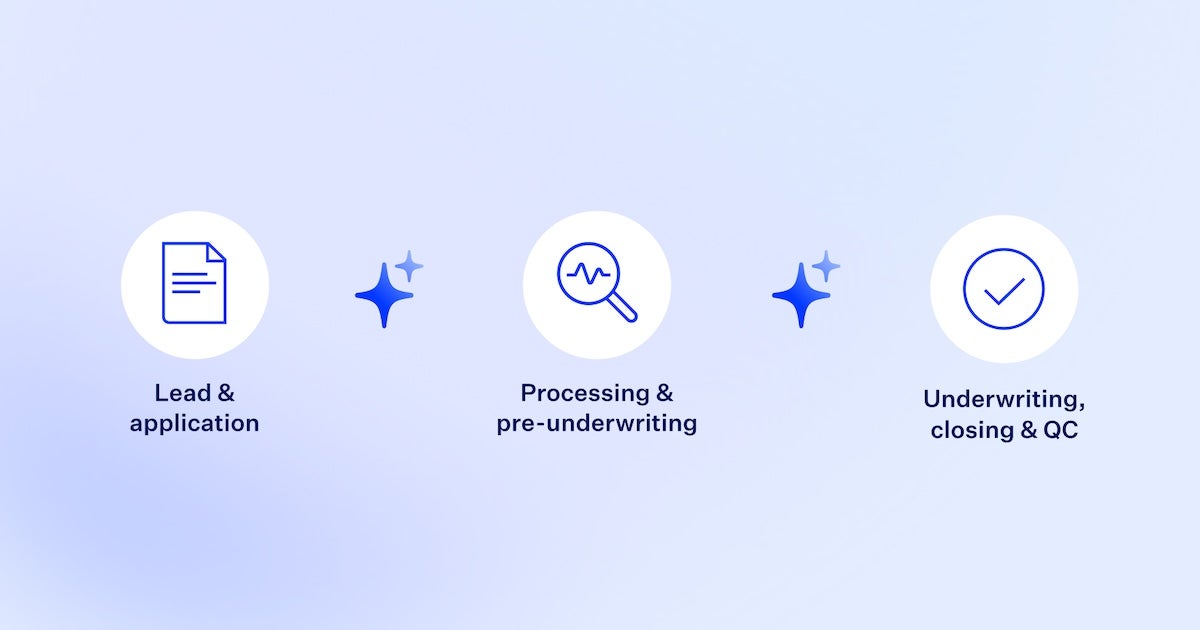

How to apply this across the origination lifecycle

Lead and application. The edge agent activates on every borrower action. Documents are reviewed against applicable guidelines in real time, and follow-ups are generated with specific context, not generic requests. By submission, the common issues are already resolved.

Processing and pre-underwriting. Agents interpret documents, normalize data, reconcile discrepancies across sources, and generate conditions with guideline citations. The work that historically sat with processors and junior underwriters runs continuously, against every document, as it arrives.

Underwriting, closing, and QC. The fulfillment agent validates data and documents against product and agency guidelines, clears conditions against AUS results, and flags discrepancies with a full audit trail. Compliance monitoring runs automatically when fees or data points change, and every action is traceable.

How mortgage lenders should structure their AI deployment

Map the two layers first. Identify where you have speed problems at the edge (drop-off, condition chasing, incomplete files) and precision problems in the core (rework, post-close defects, conditions caught too late). That’s your deployment map.

Embed, don’t bolt on. Agents that live inside your POS and LOS, integrate with the tools your teams already use, and write back to your audit trail are the ones that compound over time. Agents that advise instead of execute don’t.

Measure end-to-end from day one. Cost per loan, days to close, post-close defect rates. Define what a pre-underwritten file looks like at the handoff and measure against that baseline.

Extend once the pattern is stable. Once the edge-and-core model is working in mortgage, it extends naturally to home equity and other products, with the same agents, the same data model, and adjacent workflows.

What separates lenders who are scaling AI from those still running pilots

The lenders seeing real results aren’t running better pilots. They’ve stopped treating origination as one workflow and started designing for two distinct agents with different mandates, connected across a clean handoff.

Files arrive at fulfillment pre-underwritten, and conditions get cleared against live AUS results. The cost savings aren’t coming from any single capability, they’re coming from the compounding effect of two agents that each do their job well and hand off cleanly to the next.

Speed at the point of sale, precision in fulfillment, and no rework between them. That’s what it looks like when the two agents are working together.

Cut cost per loan starting at the point of sale

If you’re trying to improve margins without sacrificing loan quality, the edge agent is where the leverage is. It’s the part of the stack closest to the borrower, where incomplete files, unnecessary follow-ups, and manual review cycles quietly accumulate cost before the loan ever reaches fulfillment.

Blend Autopilot is built for exactly this role. It activates on every borrower action, reviews documents against applicable guidelines, calculates qualifying income, and generates targeted follow-ups in seconds. By the time the file reaches fulfillment, the common issues are already resolved, and the file arrives pre-underwritten, not as a package for processors to sort out from scratch.

The lenders who will look back on this period as a turning point are the ones who stopped waiting for the perfect moment and started building.

See how Blend Autopilot can help you reduce cost per loan and compress cycle times across your origination lifecycle.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

How Agentic AI Can Transform Mortgage Fulfillment and Cut Cost per Loan

The average mortgage still takes 38 to 42 days to close and costs over $12,500 to produce. Agentic AI changes that by transforming every phase of fulfillment.

Read the article about How Agentic AI Can Transform Mortgage Fulfillment and Cut Cost per Loan

Blend’s Autopilot Analytics Agent

Understand performance across your entire lending operation — without leaving Blend.

Start learning about Blend’s Autopilot Analytics Agent

Make Every Data Question an Actionable Answer: Introducing Autopilot Analytics Agent

Autopilot analytics agent helps lenders act faster with plain-language answers, dashboards, and connected insight.

Read the article about Make Every Data Question an Actionable Answer: Introducing Autopilot Analytics Agent