October 14, 2025 in Thought leadership

Personalization With Boundaries: Insights From Navy Federal’s Chipotle Analogy

Leading financial institutions are rethinking what personalization means, focusing on clarity and efficiency, not complexity.

Financial leaders love a good metaphor, and one from Navy Federal Credit Union recently hit the mark. During a panel discussion on digital experiences, one executive described their approach to personalization as their “Chipotle analogy.”

“If you go to Chipotle, you can create anything as you walk down the line—you can customize your bowl just how you want it. But you’re still working within defined parameters. You can’t order pasta or sushi. The choices are broad enough to feel personal, but narrow enough to stay fast and consistent.”

This landed because it’s both playful and true. One of the biggest challenges in banking right now is how to deliver personalization that actually scales.

Why personalization became a problem in banking

Over the last few years, banks and credit unions have been told personalization is the future. Customers expect tailored offers, context-aware recommendations, and proactive insights—just like they get from Spotify or Amazon.

A Financial Brand study found 74% of consumers want more personalized experiences from their financial institutions, and two-thirds are comfortable with banks using their data to make that happen. But here’s the catch: Another study found that only 14% of customers say their bank is “very effective” at delivering relevant, personalized experiences.

Why the gap? Because most personalization strategies in banking tried to mimic retail models without accounting for operational complexity, compliance requirements, or the limits of legacy systems.

In many financial institutions, you’ll see the symptoms of overcomplexity:

- Multiple checking account variants that differ in marginal ways

- Mortgage products with dozens of rate-term permutations

- Front-line service scripts that slightly shift depending on which product line you’re discussing.

Behind the scenes, those small differences multiply into significant training, systems, and exception-handling overhead. And members end up overwhelmed by choices that don’t feel any more “personal.”

What Navy Federal got right: Defining personalization’s boundaries

That’s where the Chipotle analogy becomes more than just a metaphor. It’s a reminder that personalization has to exist within a framework.

Chipotle doesn’t offer every possible ingredient—it offers a smartly curated set of options that give customers real agency while keeping operations efficient. Navy Federal applied the same principle to their member experience design.

“We always think of personalization as being endless opportunities,” said one Navy executive. “But practically, we can’t give endless opportunities. That’s expensive. That’s impossible to scale.”

Instead of trying to build infinite product variations, Navy Federal focused on what truly matters: understanding member goals.

If a member says, “I want to buy a house in 10 months,” that becomes the organizing signal for the relationship. Marketing adjusts automatically to support that goal. Product recommendations prioritize savings and credit-readiness tools. Staff conversations shift to planning and progress tracking.

The personalization isn’t about inventing new products—it’s about contextual matching within existing offerings. That’s scalable.

The trade-offs behind scalable personalization

There’s a discipline to making personalization work in financial services. Every gain in customer relevance has a cost in operational complexity, and banks have to choose their line carefully.

Research from Mastercard found that 94% of banks say they can’t deliver the kind of hyper-personalization customers expect, citing data fragmentation, resource limitations, and regulatory risk as top barriers. Another 80% collect more data than they can actually use to improve engagement.

That’s why the smartest institutions are rethinking what “personal” really means. It’s not infinite customization. It’s goal-based orchestration within defined parameters, powered by data and automation.

This kind of personalization forces institutions to make conscious trade-offs:

- Control vs. Flexibility: Limit product variations so staff can deliver quality advice.

- Automation vs. Oversight: Use intelligent systems to handle the routine, but always keep human judgment in the loop.

- Speed vs. Precision: Personalize around intent, not identity—what the member wants to accomplish, not every data point about them.

When done right, the payoff is real. Financial institutions that use goal-based personalization see higher conversion rates, shorter training times, and lower servicing costs. Customers report greater satisfaction because choices are simplified and aligned with their goals, not their demographic profile.

Why it matters now

The personalization conversation in banking is maturing. The early hype promised “a segment of one.” The reality is more nuanced: customers want relevance and recognition—but not chaos. They want clarity and confidence, not a maze of micro-options.

And as economic pressure mounts, banks can’t afford to over-engineer experiences that strain operations. Personalization done wrong drives cost; done right, it drives loyalty.

As one Navy Federal leader put it, the key is “focus over frenzy.” Boundaries don’t limit personalization—they make it real.

Three questions every bank should ask

If you’re re-evaluating your own personalization strategy, start with these questions:

- What dimensions of choice actually matter to your customers?

- How can goal data inform product recommendations without creating new SKUs?

- Where can automation reduce friction while preserving human oversight?

That’s the Chipotle lesson worth remembering. It’s not about burritos—it’s about building a menu your teams can deliver, your systems can sustain, and your customers can actually enjoy.

Want to see how employing technology strategically can transform both your core business indicators and customers experience?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

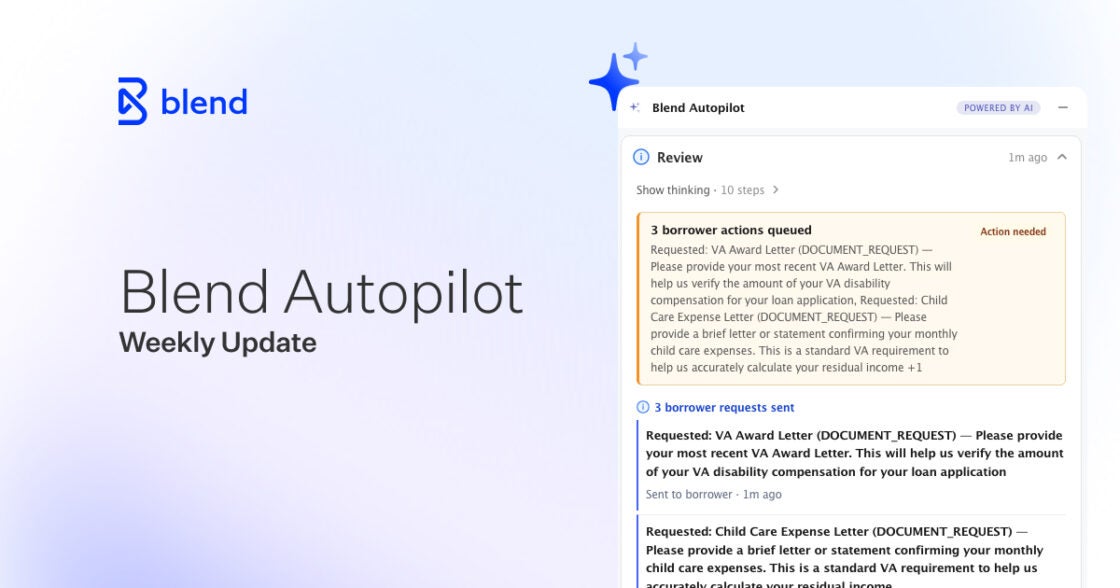

Blend Autopilot Week 11 Update: Rapid, VA, and FHA Continue to Harden, Ongoing Investment in Accuracy, and Verified Income Goes End to End

When upstream income is verified, Autopilot already knows. See what else shipped in week 11.

Read the article about Blend Autopilot Week 11 Update: Rapid, VA, and FHA Continue to Harden, Ongoing Investment in Accuracy, and Verified Income Goes End to End

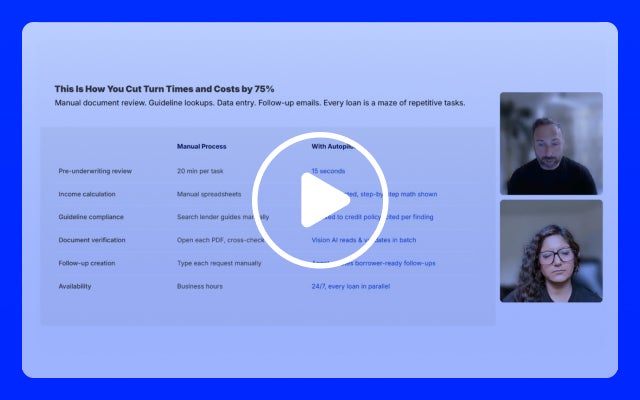

Home Equity Is the Proving Ground: How Digital-First Origination Will Define the Next Era of Lending

Speed is winning home equity. See how digital origination helps your institution compete.

Watch video about Home Equity Is the Proving Ground: How Digital-First Origination Will Define the Next Era of Lending

CrossCountry Mortgage

streamlined operations, eliminated errors, and empowered borrowers through Blend Close.

streamlined operations, eliminated errors, and empowered borrowers through Blend Close.

Read the full story about CrossCountry Mortgage