July 8, 2025 in Thought leadership

What Traditional Banks Can Learn from Fintechs: Rethinking Digital Origination

Fintechs aren’t winning because they offer more products—they’re winning because they design around the customer.

In today’s banking landscape, a frictionless experience is no longer a differentiator—it’s an expectation. The rise of fintechs and digital-first financial services has pushed traditional banks and lenders to reconsider how they approach customer experience, operational efficiency, and digital origination. So, what sets leaders apart?

Put simply: the future belongs to those with a tech-first mindset, who recognize their competition is not necessarily from other financial institutions. In this exclusive Leaders interview with American Banker, Blend’s Head of Product, Technology and Client Operations Srini Venkataramani shares his POV on how banks need to evolve and adapt to stay competitive.

“Financial institutions are dealing with a dual imperative paradox. They have tremendous pressure to increase operational efficiency, but they still need to be providing personalization at scale. That’s one thing that digital banks and banks need to be ready with. The second is the advent of new players. These are non-traditional players, new age fintechs, tech-native companies coming and changing what a B2C experience should look like in the financial world itself.”

— Srini Venkataramani, Blend

The Tech-First Shift in Mindset

Fintechs are winning because they design around customer behavior and needs. They spend time reducing steps, and anticipating what’s needed before you ask, just like Netflix recommends a next show to watch or Amazon prompts reorders just at the right time.

Banks, on the other hand, are often burdened by legacy systems and siloed data. Srini argues that the transformation isn’t just about replacing technology—it’s about embracing a new operating philosophy.

Moving from Bank Product to Customer Journey

The traditional model treats each product—checking accounts, credit cards, loans—as a separate funnel. But customers don’t think about bank products. They think in outcomes: “buy a home, reduce my debt, build savings.” A tech-first mindset encourages institutions to unify those journeys and use data to personalize them.

Why It Matters Now: Staying Competitive with Fintechs

As Srini shares, more than half of loan applicants drop off before completing an application, and this is costing real money. Fintechs are gaining market share by making these experiences intuitive, mobile-first, and invisible. Banks must catch up—not by replicating the tools, but by adopting the mindset.

“A typical home equity loan used to take 45 days. Now for example at Blend, what we have done is we have moved a lot of these things upfront. I talked about pre-fill. We also get the valuation of the particular property. You are also able to consolidate debt because you want to use the money now. We are able to do that in as low as 10 days.”

— Srini Venkataramani, Blend

Want more?

Watch the full interview to hear Srini expand on how AI and unified platforms are transforming origination, conversion, and ultimately driving measurable ROI for banks and credit unions.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

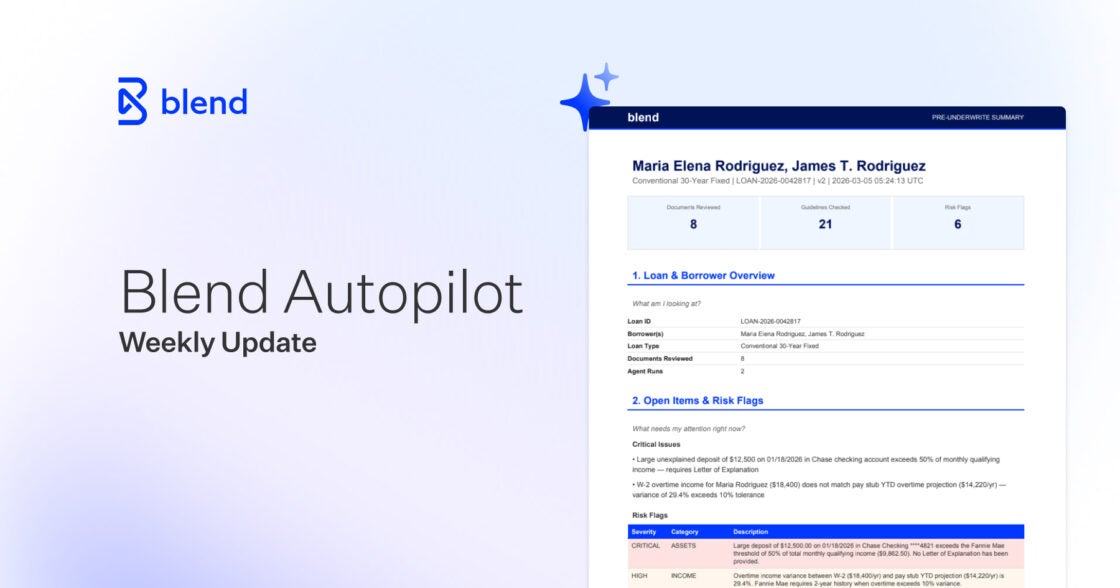

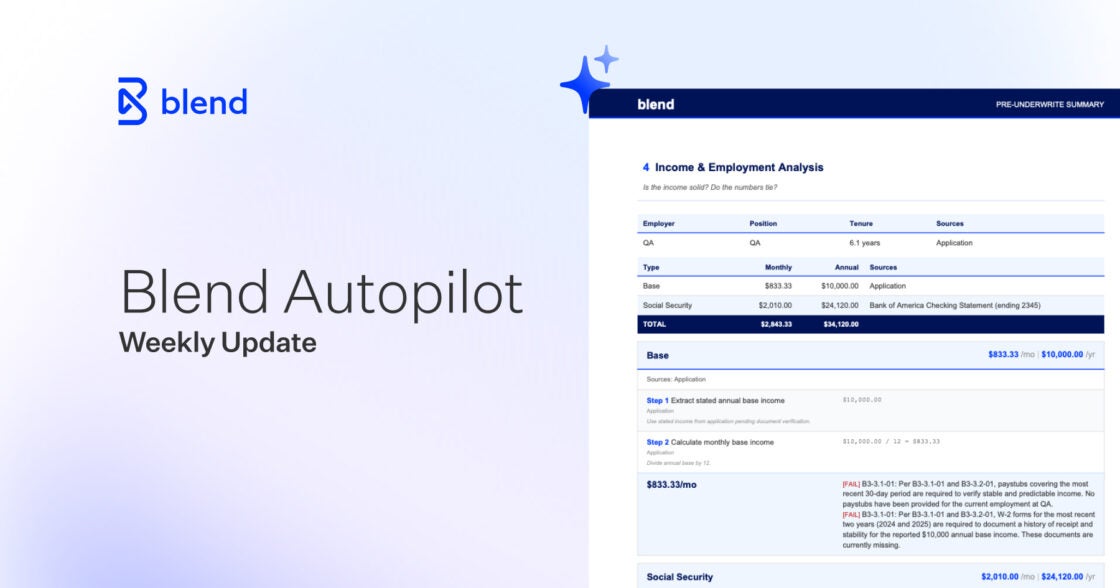

Blend Autopilot Week 4 Update: Borrower Chat Is Coming, API-Uploaded Documents Now Visible to Autopilot, and Smarter Cross-Document Analysis

Real adoption, real feedback. See how lenders are shaping what Autopilot has become this week.

Read the article about Blend Autopilot Week 4 Update: Borrower Chat Is Coming, API-Uploaded Documents Now Visible to Autopilot, and Smarter Cross-Document Analysis

Reduce Pre‑Closing Delays with Refreshable Asset‑Based Employment Checks

Learn how refreshable, asset‑based employment checks can reduce pre‑closing delays, cut last‑minute outreach, and align with DU®, LPA®, and agency expectations.

Read the article about Reduce Pre‑Closing Delays with Refreshable Asset‑Based Employment Checks

Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation

AI that handles edge cases automatically. See what shipped in Autopilot's third week of production.

Read the article about Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation