January 12, 2026 in Thought leadership

Lessons from 2008: Why Better Data Won’t Prevent the Next Banking Crisis

Bridge the gap between data and action by using AI to modernize your banking infrastructure, ensuring your institution can respond to emerging risks at the speed of the modern market.

The 2008 financial crisis revealed a critical gap in banking infrastructure: major institutions had access to warning signs but lacked the systems to act on them fast enough. As economist Nomi Prins observed from her Wall Street experience, banks could see subprime lending problems emerging in their data, but the tools to respond decisively didn’t exist at the scale or speed required.

Today’s banking leaders face a critical fork in the road. AI systems can detect fraud patterns in milliseconds, flag credit anomalies before they spread, and predict portfolio risks with unprecedented accuracy. But more importantly, modern infrastructure can now transform those insights into immediate action–a feat that was technologically unlikely just two decades ago.

The infrastructure gap that defined 2008

During a recent industry discussion, Prins described watching traders in 2008 desperately try to offload deteriorating securities. This wasn’t primarily about institutional avoidance—it revealed the limitations of the technology and infrastructure available at the time. Banks engineered elaborate securitization structures because the systems for real-time risk assessment and rapid portfolio adjustment weren’t available.

The challenge wasn’t just about having data, but about what could be done with it. Nowadays, AI systems flag suspicious loan applications, but approval processes remain slow and bureaucratic. Risk models identify portfolio concentrations, but diversification strategies get delayed by competing priorities. Fraud detection algorithms catch anomalies, but the question is whether investigation protocols keep pace with the speed of insight.

The complex securitization structures present before 2008 reflected the operational reality that banks couldn’t quickly rebalance, diversify, or adjust exposures through their existing systems. When problems surfaced, the web of interconnections made rapid response impossible because the infrastructure for coordinated action was inefficient, at best.

The trust velocity problem

AI amplifies both the promise and the peril of modern risk management. Institutions that use AI to accelerate decision-making—not just improve reporting—will build competitive advantages that compound over time. Those who treat AI as a better documentation system will find themselves repeating familiar patterns with more precise measurements.

The distinction matters because trust operates on accelerated timelines in digital banking. Social media can turn isolated customer complaints into viral reputation crises within hours. Regulatory scrutiny that once took months to build now materializes in days. Market confidence that took ages to build can vanish overnight, as regional banks discovered during the 2023 deposit runs.

This velocity demands operational agility that matches analytical sophistication. AI systems must integrate with decision workflows, not just feed into reporting dashboards. Risk flags need automatic escalation protocols. Credit anomalies require immediate investigation capabilities. Portfolio alerts should trigger rebalancing actions, not quarterly review agenda items.

Building intelligence that actually acts

So what’s the solution? Actionable AI that helps you take an automated, proactive approach.

Consider credit origination, for example: when income-to-debt ratios spike beyond normal ranges, integrated systems automatically request additional documentation rather than waiting for underwriter review. The approval process continues moving while verification strengthens.

In portfolio management, advanced institutions build systems that automatically rebalance lending concentrations when exposure limits are breached. One potential example: when commercial real estate loans in a market reach 15% of the total portfolio, new applications in that area receive enhanced scrutiny or alternative pricing—without manual intervention.

The operational advantage compounds quickly. While competitors investigate problems that already occurred, institutions with integrated AI prevent problems before they materialize—stopping risky loans before they fund and addressing compliance gaps before audits discover them.

The choice that defines the next decade

The next financial crisis won’t be caused by insufficient data or inadequate AI systems. It will be caused by institutions that accumulate perfect information about emerging risks but lack the operational infrastructure to act decisively when that information demands rapid response.

Banking’s evolution depends on closing the gap that defined 2008: the distance between knowing and acting. Customers, regulators, and investors expect institutions to actually manage risk in real time, not just measure it more precisely after the fact.

The question facing today’s financial leaders isn’t whether their AI systems can detect the next crisis. It’s whether their organizations will build the operational infrastructure to act on what they see, at the speed the modern market demands. Learn how modern lending infrastructure turns AI insights into immediate action.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

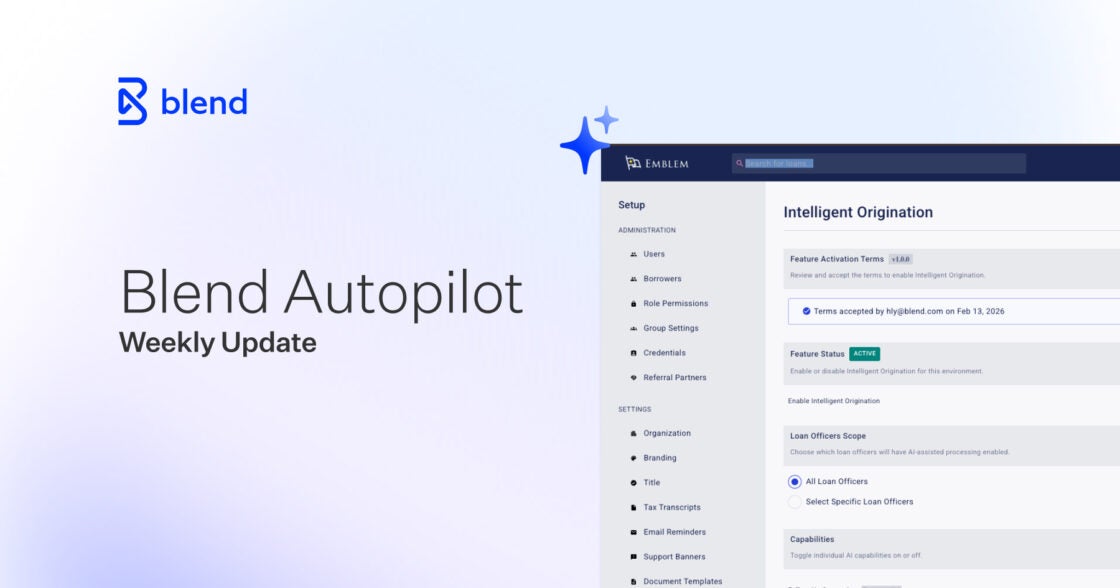

Blend Autopilot Week 1 Update: Pre-Underwriting Summaries, Income Calculation, and Smarter Follow-Ups

Reduce manual touchpoints. See how this week's Autopilot feature updates accelerate your time-to-close.

Read the article about Blend Autopilot Week 1 Update: Pre-Underwriting Summaries, Income Calculation, and Smarter Follow-Ups

Turning Home Equity Into a 2026 Growth Engine for Share, Loyalty, and Revenue

See how banks and credit unions can turn home equity into a 2026 growth engine with rapid, digital journeys that compete with fintechs and strengthen loyalty.

Read the article about Turning Home Equity Into a 2026 Growth Engine for Share, Loyalty, and Revenue

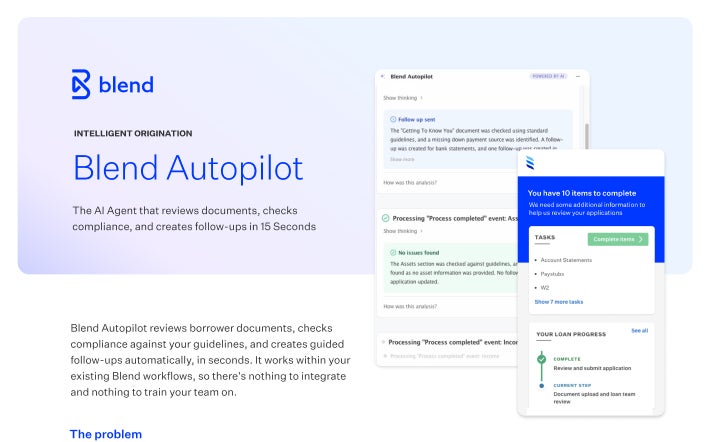

Blend Autopilot: AI That Keeps Loans Moving Forward

The AI Agent that reviews documents, checks compliance, and created follow-ups in 15 seconds.

Start learning about Blend Autopilot: AI That Keeps Loans Moving Forward