November 19, 2025 in Thought leadership

From Copilots to Closers: How Agentic AI Accelerates Competitive Pressure

Agentic AI in banking is redefining deposit stickiness and loan retention by moving money at software speed, forcing banks and lenders to earn loyalty through execution.

We’re at the start of a major shift in how we interact with the world around us.

Whether it’s our bank, our doctor, or our insurance provider, AI is moving from simply giving us information to actually taking action on our behalf, based on what we want and what matters to us. Just as the internet and mobile changed how we live and work, this next wave of AI will change how we manage our lives.

Tom Brown, founder of Second Curve Capital and longtime banking analyst, believes this shift will redefine how financial institutions compete and create value. He points to a future shaped by personal AI agents that automatically optimize financial outcomes, like moving money to capture returns or refinancing mortgages within preset parameters.

This is about fundamentally rewriting the status quo that has sustained banking organizations for generations. When money moves at software speed, the industry’s most reliable advantages—deposit stickiness, loan retention, and switching costs—become competitive liabilities overnight.

To understand what this means for the industry, we have to examine where agentic AI will first apply pressure, and how that pressure becomes an opportunity for those prepared to act.

The end of banking’s comfortable inertia

For decades, most people have stayed with the same bank not because it was the best option, but because switching felt like too much effort. This stability has masked deeper operational inefficiencies and allowed competition to center more on convenience than on value.

There is a $6 trillion gap between deposits and loans—capital sitting idle instead of being actively optimized. At the same time, most bank branches process fewer than 4,000 transactions per month, yet they maintain relationships that represent millions in lifetime value. Consolidation has accelerated across the industry, but many large acquisitions have failed to deliver returns due to a focus on scale rather than operational excellence.

This equilibrium is about to be tested by agentic AI. When customers can deploy intelligent agents that monitor and optimize their financial position in real time, every point of friction becomes a risk, and every underperforming asset becomes an opportunity for movement. Loyalty will no longer be protected by inertia, it will be earned through execution.

The question now is whether banks are preparing for a future in which customers expect their money to be as productive and proactive as the technology managing it.

Deposits become fluid, not sticky

Today, many deposits stay put because moving them is inconvenient. Customers might notice they’re earning 0.5% while high-yield accounts offer 4%, but the process of researching options, opening accounts, and transferring funds often isn’t worth the hassle. Banks count on this inertia for stable, low-cost funding.

AI agents eliminate that friction entirely. A customer could configure their agent with simple instruction parameters: maximize yield on cash reserves above $10,000, maintain FDIC insurance, minimize account fees, keep no more than $250,000 at any single institution. The agent monitors rates continuously, calculates net benefits including switching costs, and moves money automatically when the math makes sense.

As Brown puts it, “You could literally build it so that my free cash moves from Bank A to Bank B for five to 10 basis points difference.” In this world, deposits don’t stay because customers are satisfied. They stay because the institution offers the best combination of yield, service, and agent compatibility.

This puts direct pressure on net interest margins and funding costs. Banks that relied on deposit premiums from customer inertia will face immediate competitive pressure. Those offering below-market rates will watch funding flow to more competitive alternatives without warning.

The stable deposit base that underpins loan growth becomes a daily contest for rate leadership.

Loan retention gets disrupted

Refinances often lag because borrowers don’t actively track rate changes or the process feels cumbersome. Most customers refinance months after it makes financial sense, limited by awareness, time, and complexity. Even financially savvy customers can miss opportunities simply because they’re busy. As a result, many homeowners continue paying higher rates longer than necessary, delaying savings that could meaningfully improve their financial health.

AI agents will fundamentally transform this dynamic for the benefit of both borrowers and lenders. The agent could be configured to continuously monitor mortgage rates, evaluate the borrower’s current terms, factors in closing costs and tax implications, and automatically initiate a refinance the moment it meets the borrower’s goals. Whatever parameters the customer sets, the agent executes without hesitation or procrastination.

This doesn’t just accelerate savings for consumers, it positions lenders as proactive partners, helping customers capture value in real time rather than reacting after the fact.

This new dynamic doesn’t erode lender relationships. It reshapes them. Instead of relying on manual processes or infrequent check-ins, banks will have the ability to serve customers proactively and continuously. Loan portfolios will become more dynamic as customers are automatically kept in the best possible financial position, strengthening trust and long-term loyalty.

Loyalty follows the best integration

If agents can execute across institutions, customers will stick with the providers that connect seamlessly, rather than the ones with the nearest branch or the best marketing. Traditional loyalty drivers like geographic convenience, brand recognition, or relationship history matter less than API compatibility and integration capability.

Banks that offer agent-friendly interfaces will capture flow from institutions that require manual processes. Those with robust data feeds will attract customers whose agents need real-time account information. Institutions that can process agent-initiated transactions will quickly win business from those requiring extensive human approval loops.

This reshapes customer lifetime value and where growth flows, leveling the playing field for smaller institutions. A community bank with excellent agent integration could capture deposits from national banks with superior rates but inferior connectivity. A credit union with seamless refinance APIs could steal market share from mortgage giants with cumbersome application processes.

The competitive moat shifts from physical presence to digital integration. Success requires thinking like a software company: APIs matter more than branches, integration capability matters more than product breadth, and automation capability matters more than human service speed.

Banking at software speed

AI agents will fundamentally change customer expectations. Financial decisions won’t wait for a human to initiate them, agents will continuously scan for opportunities, evaluate trade-offs, and act the moment value can be created. In this environment, the institutions that win will be those whose systems are built to originate, approve, and retain in real time, not those that rely on manual triggers or static customer relationships.

This shift requires more than surface-level automation. It calls for a new architecture, one where lending workflows are intelligent, adaptive, and directly compatible with autonomous financial decision-making. Institutions that make this transition will become the preferred destination for agent-driven activity because their platforms are built to execute, not just inform.

Ready to explore how your institution can thrive in the agent economy?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

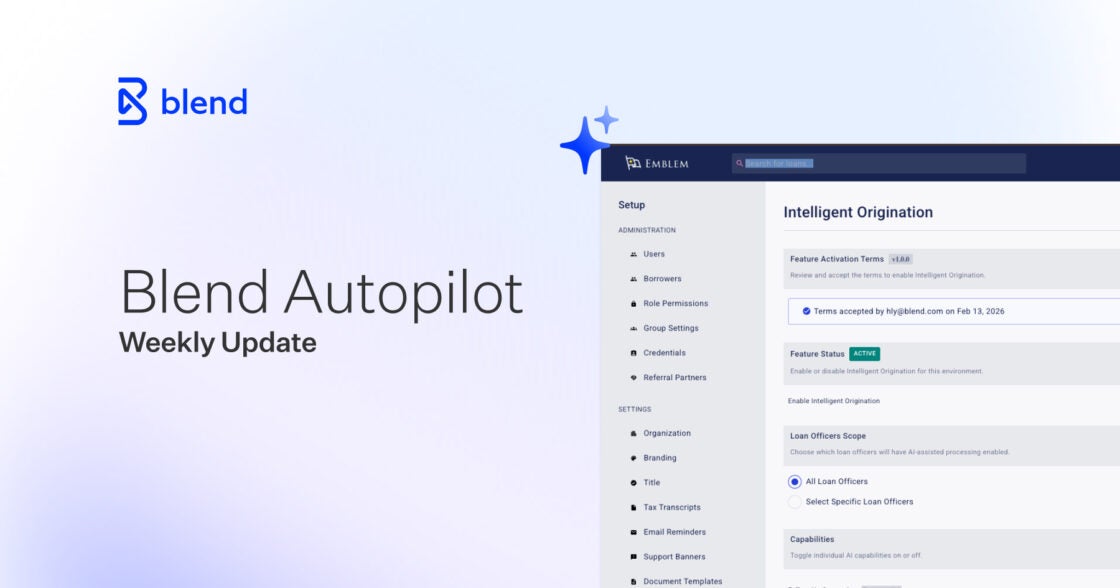

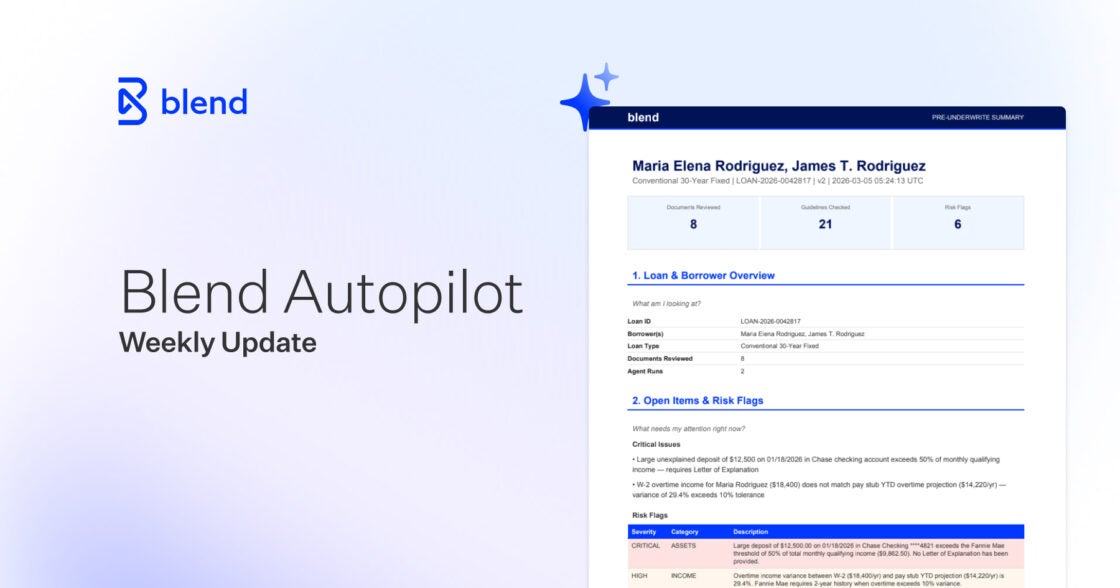

Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation

AI that handles edge cases automatically. See what shipped in Autopilot's third week of production.

Read the article about Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation

Blend Autopilot Week 2 Update: A Smarter Agent, Gift Fund Detection, and Transparent Income Calculations

This week’s Autopilot update brings a faster agent, gift fund detection, step-by-step income breakdowns, and native routing.

Read the article about Blend Autopilot Week 2 Update: A Smarter Agent, Gift Fund Detection, and Transparent Income Calculations

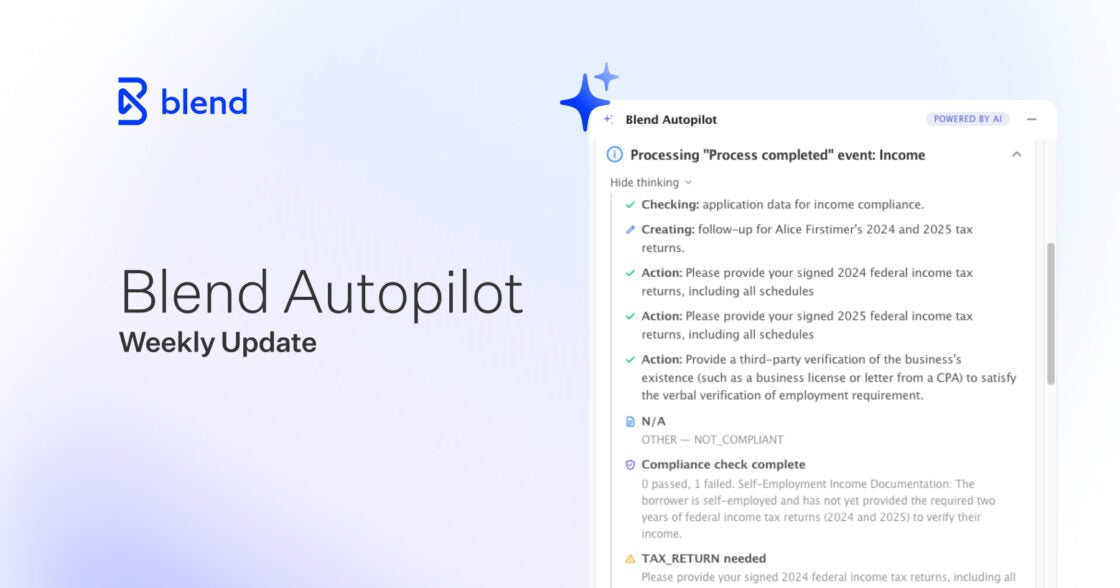

Blend Autopilot Week 1 Update: Pre-Underwriting Summaries, Income Calculation, and Smarter Follow-Ups

Reduce manual touchpoints. See how this week's Autopilot feature updates accelerate your time-to-close.

Read the article about Blend Autopilot Week 1 Update: Pre-Underwriting Summaries, Income Calculation, and Smarter Follow-Ups