March 10, 2026 in Thought leadership

Turning Home Equity Into a 2026 Growth Engine for Share, Loyalty, and Revenue

Learn how banks and credit unions can build rapid, digital home equity journeys that match fintech speed while deepening customer relationships.

Home equity has quietly shifted from a branch‑led retention product to one of the most powerful growth engines for market share, customer loyalty, and revenue.

In a home equity market where refinance volume is flat and rate cuts are uncertain, lenders that modernize home equity with digital, self‑service experiences are turning dormant equity into new originations, deeper relationships, and profitable fee and interest income.

This post looks at how leading banks and credit unions are turning home equity into a 2026 growth engine, capturing more share in a stagnant mortgage market, improving digital banking customer experience, and building durable revenue streams.

The real shift: borrower urgency and fintech expectations

U.S. homeowners hold about 35 trillion dollars in home equity, but the more important story is how they want to tap into it.

- Nearly 73% of Gen Z homeowners and 66% of millennial homeowners say they are likely to apply for a HELOC in the next 18 months.

- These borrowers already expect one‑click commerce, instant decisions, and mobile‑first servicing.

They are not looking for a mortgage‑style process stretched over 45 to 60 days. They:

- Want to consolidate high‑interest debt and see savings quickly.

- Want to fund big life moments such as starting a business, paying tuition, or renovating a home without restarting their financial lives.

- Prefer digital self‑service with human help on demand, not paperwork and phone tag.

Home equity is uniquely sticky. Once you help someone tap their equity, you often become their primary institution. That makes it a powerful relationship product and a frontline tool for customer acquisition. If your process is slow and manual, fast‑moving borrowers will simply get an approval elsewhere.

Why traditional home equity processes are losing to fintechs

Most banks still run home equity on processes designed for another era:

- Long, form‑heavy applications that make you re‑collect information you already have for existing customers.

- Manual decisioning queues that turn what could be minutes into days.

- Fragmented fulfillment and closing workflows that stretch cycle times into weeks.

Fintechs offer something very different:

- Application experiences that take minutes, not hours.

- Automated decisioning that gives a clear answer, or near‑final approval, in real time.

- Digital fulfillment and closing that can wrap in about a week for straightforward scenarios.

Even when a borrower would prefer to work with their primary bank, the path of least resistance often leads to a fintech. To win back that ground, banks need to adopt the fintech playbook in a way that uses their own strengths so they can deliver a faster, simpler home equity journey.

Four pillars of a digital home equity journey

Think of Digital Home Equity as an operating model that lets banks and credit unions match fintechs on speed and experience while using richer data and stronger risk controls.

1. Digital application experience

Your existing customers already gave you their income, employment, balances, and behavior. Asking them to start from scratch is frustrating for them and wasteful for you.

A Digital Home Equity approach:

- Prefills as much of the HELOC or home equity loan application as possible from core and DDA data, prior mortgage files, and existing KYC.

- Uses account, card, and transaction data to pre‑calculate indicative loan amounts and show real debt consolidation options up front.

- For new‑to‑bank borrowers, relies on soft‑pull credit and third‑party data sources to build a usable profile from a small set of initial fields instead of a long, manual form.

The key KPI is conversion. The goal is to move more borrowers from interest to approval by removing friction and repetition.

2. Expedited decisioning

When a borrower is ready to act, hours matter and days are dangerous. If your decision takes two or three days and a fintech can deliver a clear answer in minutes, many customers will not wait.

A Digital Home Equity model:

- Uses rules‑based and automated decisioning for low‑risk, straightforward scenarios.

- Clearly explains when more documentation is required and what happens next instead of dropping borrowers into a black box.

- Treats time to decision as a frontline performance metric, not a back‑office statistic.

The aim is to shorten the time from intent to answer so that you keep the borrower engaged and win the relationship before they shop elsewhere.

3. One‑week processing and fulfillment

Once a borrower has a decision, every extra day between approval and closing is an opportunity for them to:

- Second‑guess the decision.

- Compare offers from other lenders.

- Delay or downsize the project or payoff that triggered the application.

Rapid Home Equity targets a model where most straightforward home equity loans can be processed and fulfilled in about a week by:

- Centralizing fulfillment so branches focus on advice and relationship work while specialist teams handle documentation and verification.

- Automating document collection, conditions, and common follow‑ups.

- Using real‑time integrations for property data, income and employment checks, and liabilities instead of batch‑based workflows.

Banks that move in this direction report cutting cycle times from months to weeks, and in many cases to under 10 days for simple HELOCs.

4. Digital closing as the default

Closing is the most emotionally charged part of the journey. Redraws, missing forms, and in‑person scheduling all undermine trust at the exact moment when borrowers expect simplicity.

A Rapid Home Equity stack:

- Standardizes eClose and remote online notarization (RON) for eligible transactions.

- Uses clear digital checklists and validation to avoid redraws.

- Lets borrowers close from home or work, on their own schedule.

If your goal is to close in under 10 days, digital closing is not optional. It is part of the core experience promise that keeps you competitive with fintechs.

Fixing the utilization problem with ethical debt consolidation

A persistent challenge with HELOCs is utilization. Many borrowers open a line of credit and then barely use it. Industry data suggests it can take nine months or more before many lines are meaningfully drawn.

Fintechs often try to solve this with aggressive marketing or confusing product structures. Banks can take a better path by building debt consolidation directly into the flow.

An ethical, borrower‑first design:

- Shows the borrower all their eligible debts in one place such as credit cards, installment loans, and other high‑interest balances.

- Lets them choose which balances to pay off with their new HELOC or home equity loan.

- Turns those selections into a structured utilization plan that funds at closing and immediately improves their monthly cash flow.

The result is faster time to utilization and higher, healthier balances. You are not forcing a product. You are helping borrowers solve a visible, urgent problem: expensive revolving debt. That deepens the relationship and makes home equity feel like a financial wellness tool, not just another line of credit.

How Blend helps lenders run the fintech playbook

Fintechs have shown what is possible with self‑service, automated decisioning, and rapid fulfillment. The opportunity for banks and credit unions is to deliver a similar experience that is powered by their own data, balance sheet, and brand.

Blend’s Rapid Home Equity capabilities are built to support that shift by helping institutions:

- Create prefilled, application‑light experiences that use existing customer data and external connections instead of long, blank forms.

- Use AI‑driven workflows and rules‑based decisioning to remove days from underwriting while keeping human judgment where it matters.

- Coordinate processing, fulfillment, and closing so the journey feels connected for both borrowers and staff.

- Embed a guided debt consolidation flow that speeds utilization and increases balances in a way that is transparent and beneficial for the borrower.

In practical terms, Blend gives banks and credit unions the tools to act like a fintech competitor while keeping the advantages that fintechs do not have, such as established trust, broad product sets, and deep customer histories.

Dig into the full home equity blueprint for 2026

If 2026 is the year you expect home equity to carry more of your growth strategy, the question is not whether to invest. It is how to do it better than your fastest‑moving competitors.

Dive deeper into the data, regional patterns, and lender examples behind these insights to pressure‑test your own approach in the home equity lending market.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

Reduce Pre‑Closing Delays with Refreshable Asset‑Based Employment Checks

Learn how refreshable, asset‑based employment checks can reduce pre‑closing delays, cut last‑minute outreach, and align with DU®, LPA®, and agency expectations.

Read the article about Reduce Pre‑Closing Delays with Refreshable Asset‑Based Employment Checks

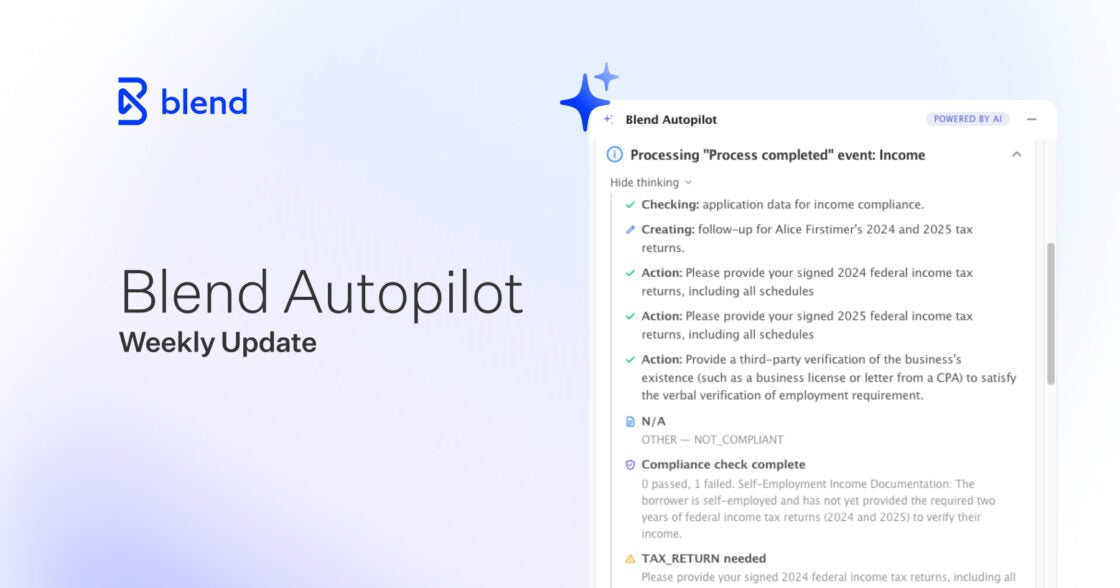

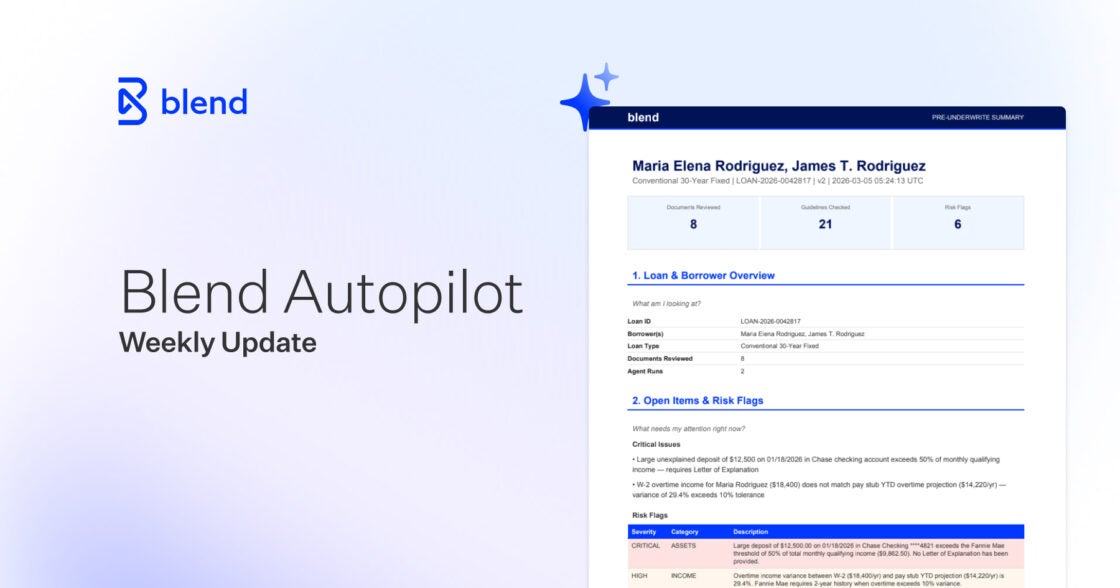

Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation

AI that handles edge cases automatically. See what shipped in Autopilot's third week of production.

Read the article about Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation

Blend Autopilot Week 2 Update: A Smarter Agent, Gift Fund Detection, and Transparent Income Calculations

This week’s Autopilot update brings a faster agent, gift fund detection, step-by-step income breakdowns, and native routing.

Read the article about Blend Autopilot Week 2 Update: A Smarter Agent, Gift Fund Detection, and Transparent Income Calculations