July 10, 2025 in Thought leadership

Consumer banking survey reveals onboarding friction remains a key challenge

New benchmarking data and actionable insights for banks and credit unions looking to drive growth in consumer banking and lending.

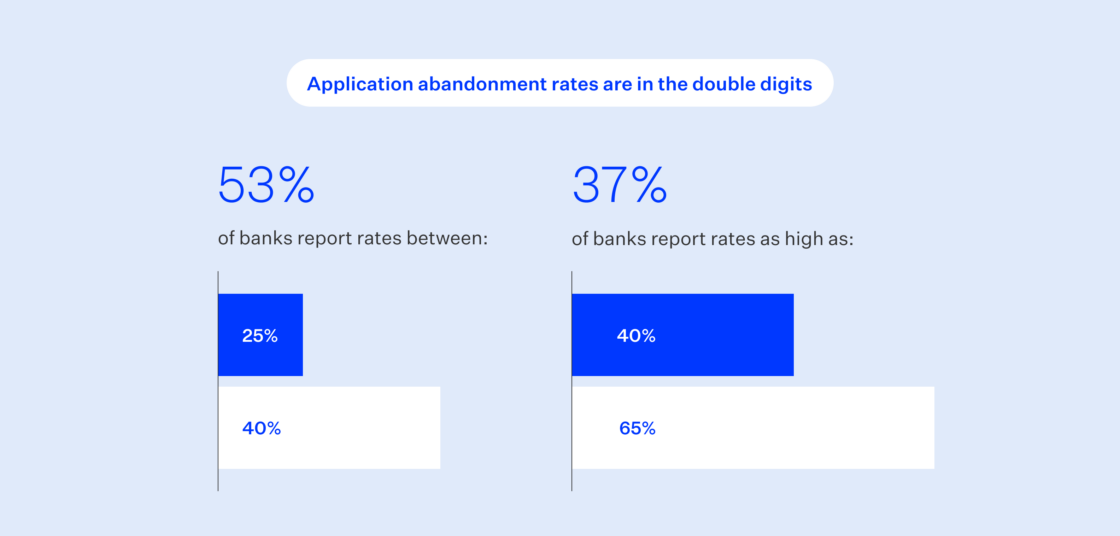

A new study of leaders at banks and credit unions by Future Branches revealed that customers and members continue to experience significant friction during the account opening and loan origination processes.

This matters because onboarding friction impacts both operational efficiency and customer satisfaction, both key factors in enabling growth. Today’s digitally savvy consumers don’t have the patience for clunky processes because they have so many other options. A frustrated potential customer will simply abandon their application and go elsewhere. With increasing competition from agile fintechs, banks and credit unions can’t afford this churn.

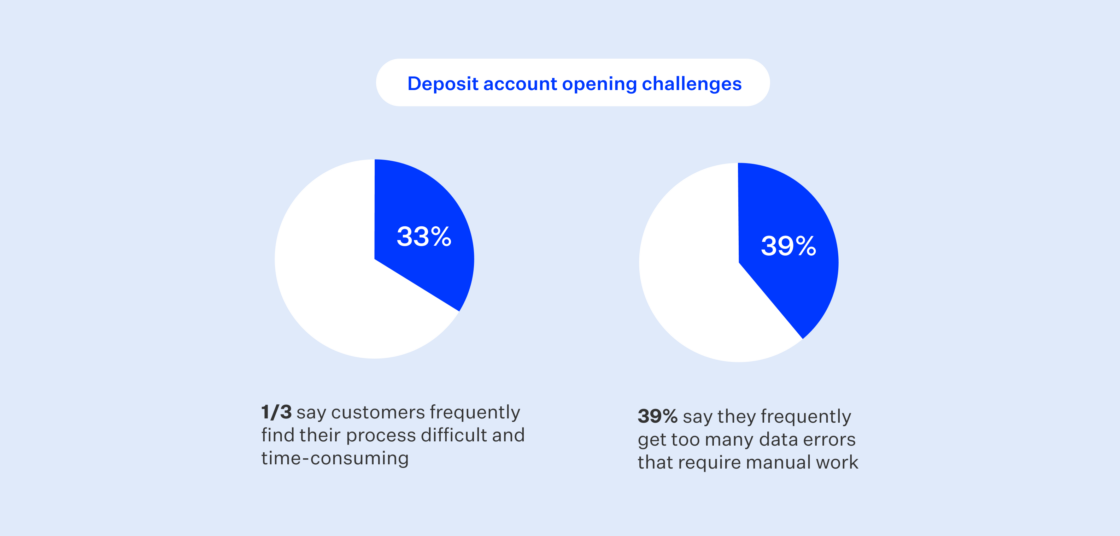

Clunky account opening is costing banks and credit unions

Opening a deposit account is often the first step to becoming a customer with a new bank or credit union. However, the report revealed that more than one-third of the respondents said they had “frequent” issues with customers finding the account opening process difficult and time-consuming. Survey respondents (51%) also said that customers occasionally needed human support due to limited self-service options.

On the operations side of the equation, 39% of respondents cited “frequent” data errors requiring manual corrections, and 51% of institutions indicated that they were struggling to leverage data for customer experience improvements and fraud and compliance issues.

These survey results highlight the need for more streamlined, user-friendly onboarding processes, backed by robust data management systems and enhanced fraud prevention measures, both to reduce inefficiencies and bolster data security.

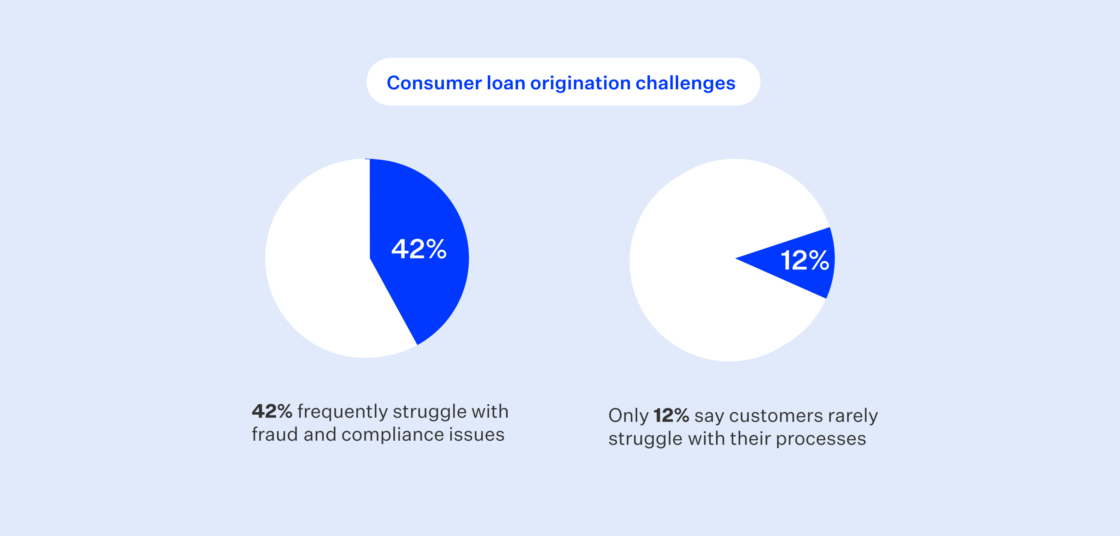

Operations can sit in the way of loan origination

Applying for a loan is often nervewracking for customers, so complications and delays can be particularly stressful. Yet, 41% of survey respondents said that customers are “frequently” frustrated with time-consuming procedures. On top of that, 42% of respondents reported that they “frequently” encounter fraud and compliance issues, making loan origination nervewracking for banks, too.

And customers aren’t the only ones impacted by delays. A whopping 61% of survey respondents say that excessive internal workflows “occasionally” impact loan origination efficiency.

These challenges emphasize the importance of balancing regulatory compliance with customer centric innovations to improve loan approval rates and funding timelines.

What’s causing onboarding friction?

In working with our customers at Blend, we’ve found that it’s generally outdated operations that are behind onboarding delays and complications. Banks and credit unions struggling with legacy infrastructure can find it difficult to keep pace with modern demands.

- Cumbersome processes: Lack of pre-filled info, static forms, and manual reviews slow down applications

- Customer frustration: Digital dead ends, lost progress, and reauthentication disrupt the experience

- Missed opportunities: No personalization or dynamic suggestions limits conversion potential

Overcoming these challenges requires a fresh approach to onboarding and origination. Customers need streamlined, unified, and personalized experiences that encourage confidence and loyalty.

See how you compare to your industry peers.

What Blend offers

At Blend, we believe that legacy bank POS systems take too much time, too many steps, and too much redundant work. With the right solutions, you can grow your organization with a smooth onboarding experience, online and in-branch.

- Increase conversion and deepen relationships: Pre-filled applications, save-and-resume, and omnichannel functionality get consumers from application to funded in minutes.

- Reduce fraud and manual reviews: Built-in identity verification (IDV), fraud detection, and eligibility logic reduce risk and manual reviews.

- Fund accounts quickly: Multiple funding options including card funding, ACH, and manual ACH enable new customers to activate accounts for use in a single session.

- Improve banker efficiency: Deliver a consistent experience across digital, branch, and phone—with banker tools and automation allowing your teams to focus on the customer, not the data.

- Deepen relationships: Present tailored cross-sell offers—like credit cards or personal loans—at account opening to improve member experience and increase lifetime value.

Want to see for yourself how Blend can streamline your onboarding and origination processes?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

Reduce Pre‑Closing Delays with Refreshable Asset‑Based Employment Checks

Learn how refreshable, asset‑based employment checks can reduce pre‑closing delays, cut last‑minute outreach, and align with DU®, LPA®, and agency expectations.

Read the article about Reduce Pre‑Closing Delays with Refreshable Asset‑Based Employment Checks

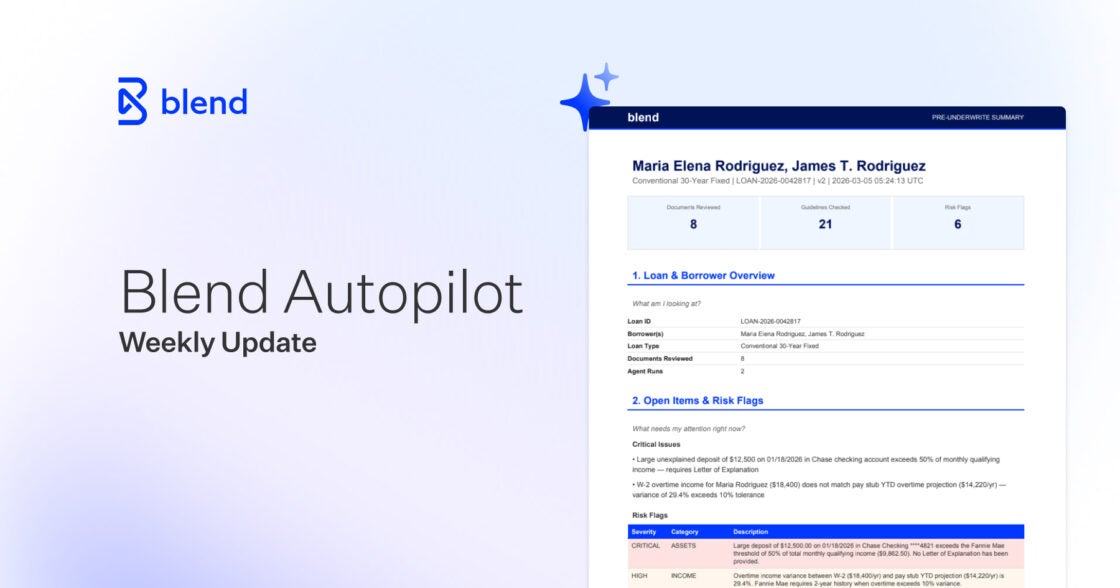

Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation

AI that handles edge cases automatically. See what shipped in Autopilot's third week of production.

Read the article about Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation

Blend Autopilot Week 2 Update: A Smarter Agent, Gift Fund Detection, and Transparent Income Calculations

This week’s Autopilot update brings a faster agent, gift fund detection, step-by-step income breakdowns, and native routing.

Read the article about Blend Autopilot Week 2 Update: A Smarter Agent, Gift Fund Detection, and Transparent Income Calculations