April 4, 2023 in Thought leadership

eNotes: Fact vs fiction

Take a deep dive into five of the most common eNotes myths as we separate fact from fiction.

As lenders trade paper-based and manual processes for the enhanced speed, convenience, and security of digital loans, the demand for digital assets has only increased. eNotes are integral to the digital closing process. In its simplest definition, eNotes are the electronic version of a paper promissory note, and if a very specific process — outlined here — is followed, they are as legally enforceable as their paper counterparts.

Although eNotes aren’t necessarily new to the digital mortgage scene, the recent uptick in their usage has prompted some frequently asked questions about their implementation and usage guidelines. Check out our list below of five of the most common eNotes myths and their clarifications.

Setting the record straight

1. Fiction: Switching to eNotes can be costly and time consuming.

Fact: Not only is there no upfront cost for eNotes, but using eNotes can actually reduce costs by shortening the length of time between origination and selling in the secondary market. Plus, by being inherently more secure, eNotes can also reduce costs associated with loss mitigation activities and saves lenders money by eliminating the need for a paper trail.

The majority of lenders already offer hybrid closings. And even if you don’t, starting with hybrid closings can help you take advantage of electronic document efficiency and streamline the closing process for borrowers. From there, adding eNotes to the closing process is a quick and natural transition.

2. Fiction: eNote adoption and use isn’t widespread.

Fact: As more lenders move beyond hybrid eClosings to fully digital eNote closing processes, the list of organizations that can originate, fund, and purchase eNotes has grown substantially. In fact, the number of companies completing transactions on the MERS eRegistry continues to grow, with a 47% YOY increase since 2022. Plus, over 1.1M eNotes have been registered since the MERS® eRegistry was established.

The COVID-19 pandemic seemed to accelerate eNote adoption, while contributing to the perception that eNote technology was new too. But believe it or not, Fannie Mae has been accepting digital closings for close to 20 years, and eNote laws have been in effect for almost 17 years.

3. Fiction: eNotes must be notarized.

Fact: This is a common misconception, and is actually incorrect for both paper notes and eNotes – neither has ever had to be notarized. In the future, some lenders may want the note to be electronically signed in front of a notary during a RON ceremony, but eNotes currently do not require notarization in order to be considered valid and legally binding. In fact, Fannie Mae and Freddie Mac even recommend and encourage eNotes to be signed before the closing date.

4. Fiction: Investors in the secondary mortgage market don’t accept eNotes.

Fact: The pathway to paperless closings keeps getting wider as private investors, funding providers, and services on the secondary market have started to accept eNotes. Fannie Mae and Freddie Mac are the largest mainstream investors, and in 2020 expanded eNote acceptance to include 45 states plus Washington DC.

5. Fiction: eNotes are just paper notes that can be eSigned.

Fact: While all eNotes are promissory notes, not all promissory notes are eNotes. While a paper note is a physical piece of paper that a borrower wet signs during the closing ceremony, an eNote is not a document in that traditional sense. With its PDF representation, in many ways eNotes look like paper versions of promissory notes, but the data underneath tells a different story.

eNotes are created in a specific file format: XML data. XML (extensible markup language) is text-based code and is actually one of the most common formats used to store content online, especially since it can be easily read and shared between software applications. The Mortgage Industry Standards Maintenance Organization (MISMO) has its own technological framework for digital. documents, which has become the standard in the mortgage industry: SMART Doc.

eNotes at Blend

Now is the time to prepare for the future. Our market is cyclical and ever-shifting. But you can be ready for what comes next by investing in innovative technology and strengthening your existing infrastructure.

We’ve seen our partners reap the benefits of Blend eNotes technology. And now that some of your most common questions have been answered, you can learn more about the eNotes opportunity and how Blend’s hands-on training and support throughout implementation can put you on the road to a more streamlined closing process.

Ready to learn more about the eNote and eVault opportunity?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

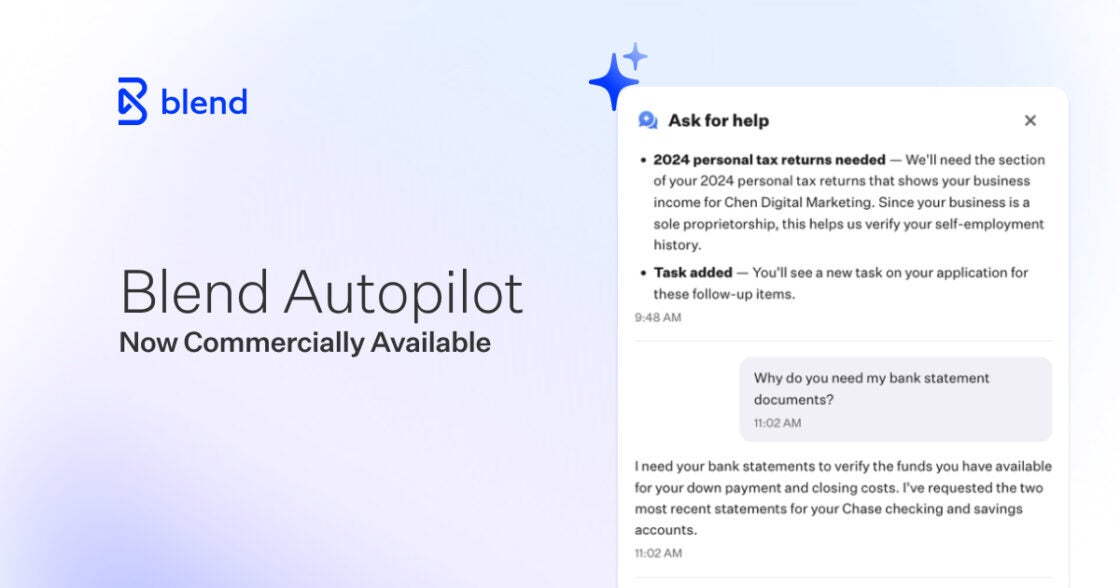

Autopilot Enters Its Next Chapter

16 weeks. 25,500 loans. See what early adopters helped Autopilot become.

Read the article about Autopilot Enters Its Next Chapter

The Question IMBs Should Be Asking Before Their Next AI Investment

For IMBs, the question isn't whether AI looks strong in a demo. It's whether it can reduce cost per loan, manual rework and margin pressure.

Read the article about The Question IMBs Should Be Asking Before Their Next AI Investment

15 Seconds to Clear: A Deep Dive & AMA on Blend Autopilot

An AMA with Co-founder and Head of Blend, Nima Ghamsari, on how Autopilot is reshaping mortgage origination with agentic AI.

Watch video about 15 Seconds to Clear: A Deep Dive & AMA on Blend Autopilot