April 26, 2021 in Thought leadership

In conversation with Forrester: Closing the gaps in digital transformation

Forrester’s Jost Hoppermann details the state of digital transformation in banking and outlines potential solutions for banks to reach digital agility.

This Q&A with Forrester’s Jost Hoppermann was commissioned by Blend. The views of Jost Hoppermann do not necessarily represent the views of Blend.

In our recent webinar, “Beyond transformation: The digitally agile bank,” Blend Head of Product Erik Wrobel invited guest speakers to discuss how the pandemic has accelerated the industry’s shift to digital. Jost Hoppermann, Forrester VP and principal analyst, brought an industry research perspective, and Tom Bianco, SVP, head of innovation and commercial digital at Fifth Third, talked about his experience leading digital transformation efforts in an increasingly digital world.

If you missed the webinar, you can watch the on-demand recording here. In the meantime, we followed up with Hoppermann for a Q&A to further unpack proprietary Forrester survey data and insights that help explain how we got here — and what banks should prioritize next. Hoppermann dives into the gaps banks felt as the pandemic hit and what capabilities they have been investing in to adapt to an increasingly digital landscape.

On digital preparedness and the momentum imperative

Blend: According to Forrester survey data, 88% of financial services firms worked on transformation or planned to start doing so soon prior to the pandemic. Why wasn’t the industry better prepared to cope with the pandemic’s digital requirements? Where did these firms fall short in their digital transformation initiatives that caused them to be caught flat footed, and what can they do better to avoid it in the future?

Want even more insights like this in your inbox?

Subscribe for industry trends, product updates, and much more.

Hoppermann: Let us use an additional data point to put this into perspective. In the same Forrester survey, the Global Financial Architecture Survey Q3 2019, 81% of respondents explained that their firm did not have the right technology infrastructure and banking applications in place to deliver great, differentiating experiences that meet the needs of their customers. A mere 5% of financial services firms told Forrester that they already finished their digital transformation initiative. Further, only 43% of financial services firms expected to be digitally ready in 2021.

What were the reasons for this not very optimistic scenario? The share of institutions that explained that they were already working on transformation or intended to start soon has been stable for about a decade, but without much to show for it. Banks remain reluctant to fully transform their application landscapes, easily getting stuck in the planning phase or focusing their transformation efforts on a single functional or organizational area. Reasons include a perception of transformation risk that is too high to be manageable, the lack of necessary skill sets to drive a transformation program, and business priorities that change too rapidly. However, banks also need to consider the fallout of delayed and canceled projects. For example, I have seen banks losing frustrated key experts after a carefully planned transformation initiative got stalled for the second or third time.

So, it’s no huge surprise that many banks were ill-prepared for the requirements of the pandemic. During the first few moments of the pandemic, plenty of gaps were revealed related to the scalability of banking applications, the breadth and depth of digital banking services, the ability to support a work-from-home model, and even secure remote operations of systems and applications. But then, many banks got rid of their initial apathy and started to close these gaps. Moving forward, banks not only need to accept the transformation initiative as a general principle but also make digital transformation real — despite all obstacles.

Urgency drives action, but not always holistically

Blend: Is it true that banks delivered more digital transformation in three months during the pandemic than in three years before?

Hoppermann: To some extent, yes. Many decision makers in banks and representatives in consulting firms and software companies share this opinion. After all, the pandemic caused banks to extend the breadth and depth of their digital services quickly and provide scalable environments for employees to work from home rapidly.

For example, some banks did not even have the infrastructure in place to support all their employees working from home — it had never been designed for anything beyond a defined manageable group of business travelers. Some banks also introduced cloud-based customer onboarding and loan origination solutions and combined them with more powerful credit risk systems to keep their loss-given-default manageable. This indicates that banks accelerated their digital journeys in selected areas.

However, considering the starting point that many banks were in prior to the pandemic, this acceleration did not take effect on the entire application landscape of a bank or for all banks. Exceptions exist on both sides: economically weak banks focused on the most crucial gaps to stay in business during the pandemic or are still struggling to close their individual gaps. Banks in a more favorable situation are preparing their future transformation plans or even increasing the speed of their transformation initiatives.

The bottom line: The state of digital transformation in the banking industry remains as heterogeneous during the pandemic as it was prior to it. While plenty of business areas need to work with the same set of legacy applications and broken business processes they had to use prior to the pandemic, many banks and their technology teams did a great job of enhancing digital services where they were needed most. Banks need to keep up the pace of this today only partial digital transformation and broaden its scope. Successful banks will be in a good position to remain competitive in the future.

Seeing through the facade of a a digital front-end

Blend: How do the most sold functional areas in the 2020 banking platform deals align with pandemic-specific needs of banks?

Hoppermann: Forrester has run its annual Global Banking Platform Deals Survey for the last 16 years. One focal aspect of the survey is to identify which functional areas financial institutions purchased in the surveyed year. For 2020, the survey showed that lending was the functionality that was included in most 2020 banking platform contracts (17%). Mobile banking remained stable, while digital banking (embracing a variety of channels) increased its share by one percentage point.

However, for the first time, Forrester looked at loan origination as a separate category. This new category that was formerly part of the broader digital banking category was sold in 9% of all banking platform deals. This shows both the relevance of the broader lending space as well as the need to broaden digital services offerings, particularly for loan origination. Because these numbers do not include the 2020 contracts of banking software vendors focusing on digital services, lending, and loan origination (as opposed to offering an end-to-end banking platform), it is reasonable to assume that all three areas saw even higher demand in 2020.

At the same time, transactional capabilities like core banking defended their territory. This space remains very relevant but experienced a few dents. Reasons include banks focusing more on closing immediate gaps than on strategic initiatives. Thus, banks may have decided in favor of dedicated, likely cloud-based, solutions that they could deploy more rapidly than potentially broader and richer back-end capabilities within a banking platform. During the early days of the pandemic, daily needs likely overrode established and agreed-upon business and technology strategies.

While this is a feasible approach in the short-term, it can become a crucial issue in the long-term. If banks return to focusing on the “digital front-end” as opposed to supporting true digital banking — delivery of seamless end-to-end processes and services to bank customers — they may again face a situation characterized by glossy facades without supporting back-end capabilities. This focus on fancy user interfaces that do not deliver great CX (as in end-to-end digital banking) is a situation that Forrester calls the Potemkin effect in banking.

Getting to the core of the problem

Blend: Why is a digital architecture important for a bank to remain competitive in the future?

Hoppermann: Forrester has worked on a concept for some time that we call digital banking platform architecture (or DBPA). It is about splitting what’s traditionally considered core banking (and further back-end solutions) into two decoupled elements: the lean core and the digital core.

The lean core focuses on data availability and consistency. It would, for example, shrink core banking in a lean fashion in that it would focus on data storage plus basic accounting and consistency rules. On top, the digital core delivers domain-driven, highly coherent business capabilities (for example, for the customer domain) using data that the lean core provides via APIs. Again on top, two architectural building blocks allow banks to deliver all these flexible business capabilities to customers, employees, and particularly via APIs to partners. This architectural approach offers several benefits.

Transformation: The highly decoupled and coherent nature of this type of digital architecture allows banks to buy or build new business capabilities independently, also using different technology stacks and delivery models. For example, a bank could introduce a new microservice or bundle of microservices representing a new origination capability that both its own digital apps and partner solutions can consume. However, it would not need to start from scratch — it could reuse domain-specific capabilities like customer, deposit, and loan and assemble them leveraging workflows and events.

Innovation: This type of architecture embraces innovation via its design. It allows banks to use new capabilities such as AI and advanced analytics via different types of APIs. For example, a bank’s technology team could use an AI-powered KYC solution or partner-provided service within an onboarding process. Or the team could hook journey analytics into its digital engagement platform to provide more immediate and insightful data to business teams. Opportunities are plentiful, and digital architecture offers the necessary level of agility to make them real without large-scale transformation projects.

Coexistence: Digital architectures don’t demand any big bang type migration. In fact, it’s just the opposite — they can coexist with traditional systems. Solutions designed in line with the idea of DBPA can use data residing in traditional systems via data APIs as well as event-driven replication and streaming. Thus, a technology team only needs to tweak its traditional systems once and then can build or buy new business capabilities outside of the traditional systems. As long as the new systems cannot yet provide all needed business capabilities, the bank continues to use the traditional systems to close the gap. At the end of the transformational journey, the bank can shut down the traditional systems.

Ecosystems: Banks will increasingly become members or centers of banking ecosystems, and digital architectures need to support this approach. The structure of digital architectures like Forrester’s DBPA allows banks to consume business capabilities from partners and service providers and expose bank internal capabilities to the outside world, thus supporting different constellations of business scenarios. In an endgame situation, digital banking engagement platforms (also known as the “digital front-end“ or the upper layers of DBPA) will become the anchor point for banking application ecosystems and help banks thrive. Engagement platforms will be the new high ground in a bank’s application landscape.

The shift to digital continues, and we have you covered.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

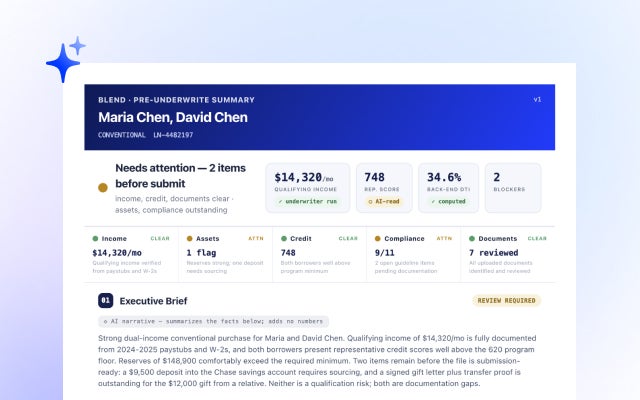

Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Every figure, every source. See how Autopilot's latest update makes pre-underwriting faster to act on.

Read the article about Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

The mortgage market is projected to reach $2.2 trillion in 2026, but flat isn't the same as easy. With per-loan costs exceeding $12,500, discover why cost per loan is the…

Read the article about Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

Five-Minute Home Equity: How to Outpace Fintechs and Win Member Loans

How credit unions are using AI to close HELOCs in minutes and outcompete fintech lenders.

Watch video about Five-Minute Home Equity: How to Outpace Fintechs and Win Member Loans