February 17, 2026 in Platform and services

From Reactive to Predictive: Unlocking Deeper Member Engagement

The shift to predictive banking allows credit unions to move beyond static product checklists, using integrated data and real-time signals to deliver personalized guidance that anticipates member needs.

A member walks into your branch after completing a car loan application online. Your team pulls up their profile: name, address, checking account balance. What they can’t see is that this member spent 20 minutes browsing home equity rates on your website last week, or that they’ve been price shopping on your mobile app every Tuesday for a month. Instead of connecting with their clear interest in tapping home equity, the conversation defaults to a standard product checklist.

This disconnect happens thousands of times daily across credit unions. Members expect the kind of personalized guidance they get from their favorite apps, but encounter experiences that treat them like strangers at every touchpoint.

Forward-thinking credit unions are changing this story. They’ve discovered how to move from reactive product recommendations to predictive member guidance, creating experiences that feel less like sales pitches and more like trusted financial opportunities. This enables them to meet members exactly where they are in their financial journey.

Why reactive cross-selling falls short

The traditional playbook made perfect sense when member expectations were simpler and competition came mainly from down the street. Train staff on product features, identify profitable offerings, then systematically present options during every interaction. Check the boxes, hit the targets, grow the business.

But this approach creates blind spots that modern members won’t tolerate:

Every channel treats members like first-time visitors

A customer might check their mobile banking app twice a day. Your loan system might show they’ve made two years of early payments. They may have even attended a first-time homebuyer seminar. But when that same customer calls your contact center, none of those signals connect.

Staff ask the same qualification questions, missing obvious opportunities to provide genuinely helpful guidance.

Institution priorities drive timing, not member needs

When your credit union focuses on home equity this quarter, every conversation steers toward HELOC products—even for members who just bought their house or are planning retirement next year. Members notice when offers feel like inventory management rather than personal financial guidance.

Valuable insights stay trapped in separate systems

Marketing platforms track website behavior. Core systems manage daily banking. Loan origination handles applications. CRM stores conversation history. Without these systems talking to each other, your team is having important conversations while missing the full picture of what members actually need.

These disconnected experiences don’t just create frustration, they erode the trust that makes credit unions special. When your institution can’t tap into previous conversations or acknowledge obvious member interests, people start questioning whether you really understand their financial goals.

Three paths to predictive success

Credit unions seeing breakthrough results in member satisfaction and cross-sell effectiveness are taking three distinct approaches to solve these challenges:

Creating complete member pictures

The most successful credit unions are connecting their systems so staff can see the full story during every interaction. Think of it like having a complete medical chart before a doctor’s appointment. Instead of repeating symptoms and history, conversations can focus immediately on solutions.

When systems connect properly, magic happens. Website browsing flows into CRM records. Mobile app usage informs phone conversations. Previous applications connect to new opportunities. A member calling about checking fees reveals they’ve been researching mortgage rates, naturally opening conversations about homeownership goals rather than just fee structures.

Peoples First Credit Union’s Howie Meller explains the transformation: “It’s really understanding what the consumer wants when they come to us, immediately being able to provide that without having to ask a lot of questions. We can act and offer what their need is as opposed to what our need was.”

This approach eliminates redundant questions while revealing natural transition opportunities. Members feel understood rather than interrogated. Staff focus on guidance rather than data gathering. The investment involves system integration, but the payoff shows in both member satisfaction and team effectiveness.

Timing offers with life moments

Smart credit unions use member data to recognize real life events and connect when interest is naturally highest. Rather than launching broad campaigns and hoping for engagement, they tailor outreach based on member behaviors and lifecycle signals. For example:

- A spike in spending at home improvement stores may indicate renovation plans, perfect timing for a HELOC offer.

- A savings balance reaching a new threshold may signal readiness for retirement planning.

- A new address near an elementary school could suggest a growing family, prompting conversations about college savings accounts.

One credit union increased push notification response rates from 2% to 18% simply by aligning outreach with member behavior instead of arbitrary marketing schedules.

Sri Aravamudan from BCU describes the evolution this way: “The goal is to move from reactive, to proactive, to predictive. Predictive is where the true differentiation happens. That’s when you’re no longer asking, ‘What should we recommend?’ but instead anticipating, ‘What does the member actually want?’”

The strength here is precision timing and proper analytics capabilities. Conversations that happen when member interest is already elevated make interactions feel helpful rather than intrusive.

Meeting members where they are

The third approach focuses on reducing friction through tools that make cross-selling feel natural rather than forced. Shopping carts, intelligent notifications, and embedded experiences help members explore options without pressure.

Shopping cart functionality exemplifies this philosophy perfectly. Instead of separate applications for checking accounts, savings, and credit cards, members add multiple products to one cart and complete everything together. Staff report that conversations become more consultative because technology handles workflow complexity while humans focus on member guidance.

Meller describes the impact: “Our team was able to drop the products in the cart and have the conversation. They were focusing more on what the conversation was than thinking ahead to the checklist. The information’s right in front of them and they’re moving forward with it.”

This approach reduces cognitive load for everyone involved. Complex processes feel simple. Relevant offers appear at natural decision points. The challenge lies in building seamless experiences that feel helpful rather than intrusive.

The predictive payoff

Credit unions implementing these approaches are seeing transformational results. NPS scores jump from the 60s into the 90s as members feel genuinely understood. Teams report higher job satisfaction because they’re solving problems rather than selling products. Cross-sell conversations become collaborative rather than transactional.

But the competitive advantage extends beyond immediate returns. In a market where members can switch institutions with a few clicks, predictive capabilities create sustainable differentiation. While competitors ask basic qualification questions, predictive credit unions are already discussing solutions aligned with life goals.

The shift requires investment in technology and process changes. Teams need training on new tools and approaches. Systems require integration work. But early adopters are building the kind of member relationships that turn transactions into lifelong partnerships.

The future belongs to credit unions that anticipate member needs before they’re fully articulated. Members don’t want to be sold to, they want guidance toward financial success. The institutions mastering predictive cross-selling will build trust that makes every other competitive advantage secondary.

Ready to move beyond reactive cross-selling?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

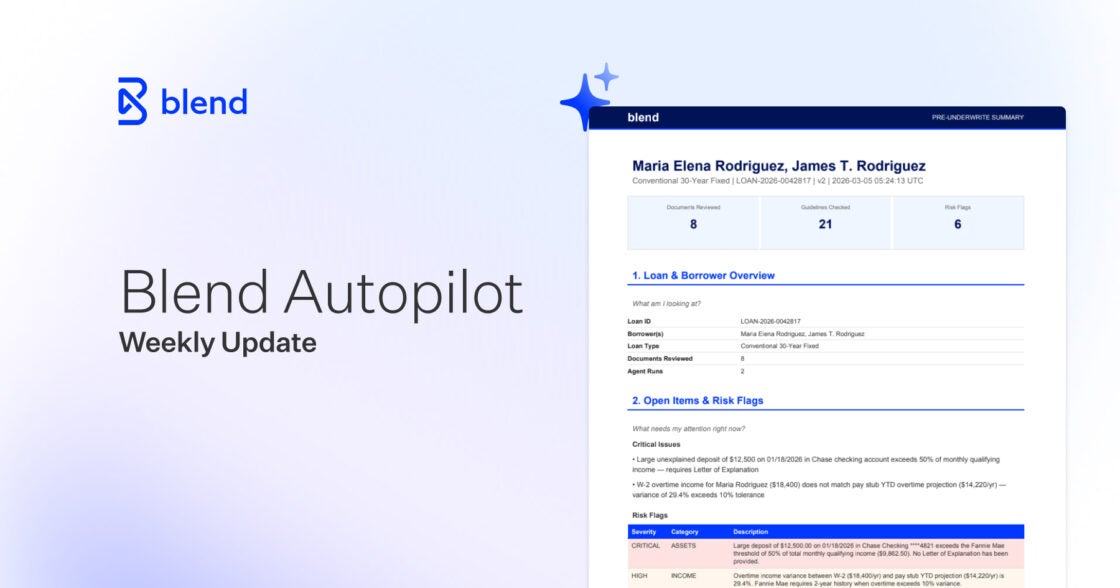

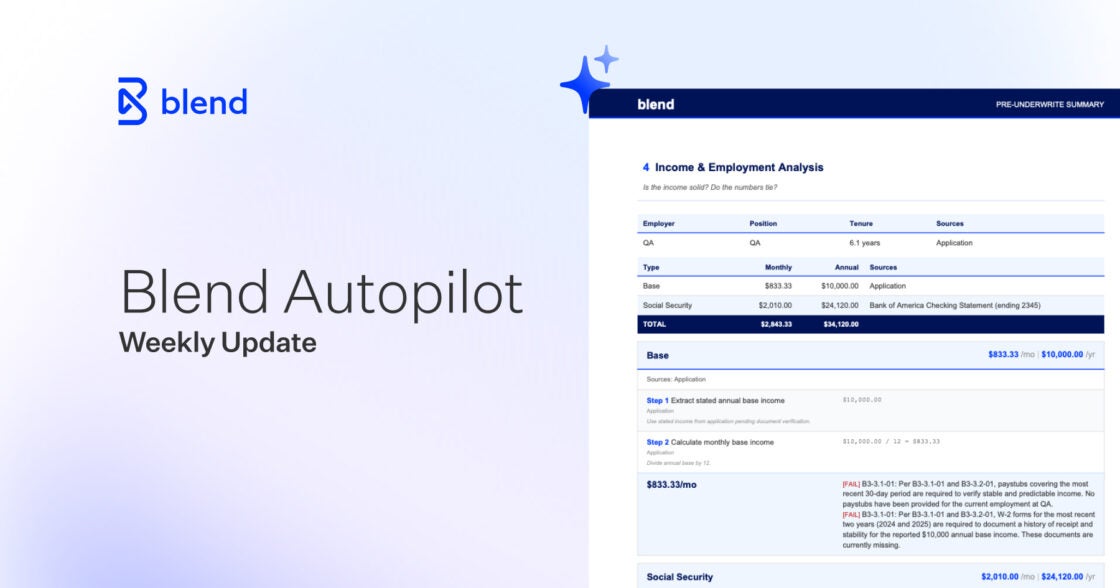

Blend Autopilot Week 4 Update: Borrower Chat Is Coming, API-Uploaded Documents Now Visible to Autopilot, and Smarter Cross-Document Analysis

Real adoption, real feedback. See how lenders are shaping what Autopilot has become this week.

Read the article about Blend Autopilot Week 4 Update: Borrower Chat Is Coming, API-Uploaded Documents Now Visible to Autopilot, and Smarter Cross-Document Analysis

Reduce Pre‑Closing Delays with Refreshable Asset‑Based Employment Checks

Learn how refreshable, asset‑based employment checks can reduce pre‑closing delays, cut last‑minute outreach, and align with DU®, LPA®, and agency expectations.

Read the article about Reduce Pre‑Closing Delays with Refreshable Asset‑Based Employment Checks

Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation

AI that handles edge cases automatically. See what shipped in Autopilot's third week of production.

Read the article about Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation