June 12, 2020 in Thought leadership

Wells Fargo advances digital experiences and mortgages during COVID-19

As the lending community continues to find new footing in the evolving landscape, Blend President Tim Mayopoulos hosted a talk at LendIt Fintech Digital about using technology to stay nimble in a rapidly changing real estate market. Tim sat down with Nate Longfellow, head of digital, product strategy, and change delivery for home lending at Wells Fargo, to chat about how Wells Fargo is adapting during COVID-19 while maintaining its focus on customer experience.

How Wells Fargo pivoted lending during COVID-19

According to Longfellow, the transition to remote work for Wells Fargo was fairly smooth. He noted that many people think the mortgage industry is behind the times, but that the industry has overall responded very well on a global scale. From remote telephony to back office processes, Wells Fargo moved to a highly remote approach over the course of a few weeks. So far, Wells Fargo has seen an improvement in productivity and other aspects of performance and there is not any hurry to get back to the office yet. The company plans to wait for local geographies to provide the right guidance in moving forward.

Loan teams have been forced to adjust their mortgage closing process during COVID-19 by offering remote notaries and digital signing technology. Longfellow noted that both of these capabilities have been around for quite some time, but Wells Fargo had to mobilize very quickly to stand up solutions in that space. “That was probably the largest rapid development for us… that was the beginning of what’s next for us,” he said. “If the digital consumer wasn’t fully awake six months ago, they are fully awake now and we need to be much more prepared for it.”

When asked how Wells Fargo has seen consumer behavior change while the organization has been working remotely, Longfellow said that they’ve never been busier with customer engagement. There has been a strong desire to move toward digital service, with customers wanting to work with lenders on their schedule in the privacy of their homes.

Driving innovation by focusing on customer experience

The conversation turned to how consumer expectations have been reset by non-lending companies that truly understand their customers and deliver value. Longfellow shared his view that these top-tier companies are not driven by innovation, but rather by the customer first. “That’s what we’re trying to do at Wells Fargo,” he said. “Let’s really understand what our customers want and what they need. And then find a way to deliver that in a way that’s meaningful and impactful.”

Longfellow spoke about how the mortgage industry has not fully embraced the fact that it needs to focus on customer value. “Nobody wants a mortgage. They want a home,” he said.

Looking at how the mortgage industry measures customer experience, Longfellow shared his opinion that the 10-day mortgage should not be seen as a holy grail for lenders. “Customers are looking for certainty. They’re looking for speed to certainty,” he explained. The focus should be less about the timeframe of application to close and more about quickly giving customers confidence in both the transaction and their ability to trust their lending partner.

“It’s very uncertain times for a lot of folks,” he said. “Certainty is probably moreso relevant than any other emotions that our customers are going through … how do we give them trust and confidence in what’s to come?”

Advancing and automating digital lending

Automation plays a large role in accelerating that time to certainty. Longfellow spoke about the need to continue advancing digital engagement. “We’re doing some great things with Blend in this industry — we have the One-tap solution, which is probably the most innovative solution that’s out on the market.” He continued explaining that Wells Fargo is looking to step on the gas and move to more of a digital-first model.

In order to improve the lending process further, the organization is taking a data-driven mindset. Longfellow talked about the variety of touchpoints they have with customers, including wealth management, small business, banking, and home lending. “With that relationship comes a real unique opportunity to leverage our customers’ information in a way that serves them better — that automates their process, gives them a know-me experience, and really takes a lot of friction out of the process.”

Wells Fargo is taking a futuristic view of how it can drive automation for customers and make decisions for them. Longfellow acknowledged that both the customer relationship and the data inherent to it are perpetually present, yet constantly shifting, so the organization is moving to a world where they have the ability to decision customers at any time. “We’re going to build capabilities to be ready to lend, when the customer is ready to transact,” he said.

Longfellow spoke about the comprehensive set of capabilities this will require. “It’s really about knowing the customer and their data, knowing investor guidelines and rules and that data,” he explained. “And setting a model that allows it to constantly change. And that’s a fact within a real estate transaction — data will change. Our systems and our intelligence need to be smart enough to adapt to that change and that’s a big anchor point of strategy and solutions around it.”

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

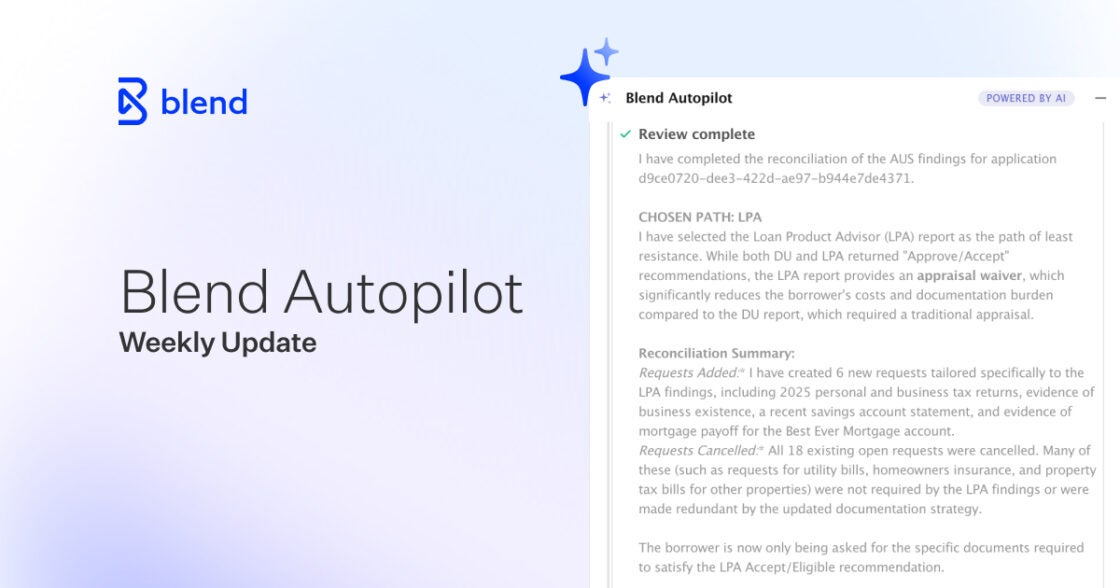

Blend Autopilot Week 9 Update: Autopilot Now Runs on Rapid Loans, Evaluates LO-Created Follow-Ups, and Refines Borrower Chat

More loan types, less noise. See how Autopilot keeps pace with your volume in week 9.

Read the article about Blend Autopilot Week 9 Update: Autopilot Now Runs on Rapid Loans, Evaluates LO-Created Follow-Ups, and Refines Borrower Chat

Blend Autopilot Week 8 Update: Autopilot Thinks Like an Underwriter, Borrower Chat Ships to Production, and New MCP Capabilities

Less prep work for underwriters. See how Autopilot thinks through AUS findings in week 8 updates.

Read the article about Blend Autopilot Week 8 Update: Autopilot Thinks Like an Underwriter, Borrower Chat Ships to Production, and New MCP Capabilities

Where AI Belongs in the Mortgage Origination Lifecycle

See where AI belongs across the mortgage origination lifecycle so you can lower cost per loan, speed cycle times, and raise loan quality.

Read the article about Where AI Belongs in the Mortgage Origination Lifecycle