October 9, 2020 in Challenges and solutions

Digital experiences and the factors affecting customer loyalty in banks

Due in part to the competitive and crowded nature of the industry, banks have long recognized the importance of providing a delightful experience for customers. But the fight for loyalty and retention is intensifying. While many retail banks are focusing on improving digital experiences, an increasing number of fintech and digitally native companies are stepping up their customer-centric offerings.

Consumers today have high expectations, which often surpass their bank’s current digital agility capabilities. When there is a disconnect between a bank’s offering and the personalized service and seamless experience their customers expect, there is a risk that the relationship will be damaged. It’s never been easier for consumers to change banking providers with products and offering information readily available online. With many customer-centric offerings entering the market and the world at their fingertips, consumers don’t need to settle for a subpar experience.

So how can banks impress their customers and meet their customer loyalty goals?

Understanding the factors affecting customer loyalty in banks

Research from BAI in 2019 found that the most common reason customers switch from a traditional financial institution to a new competitor in the space is convenience. More than 50% of Gen Z, Millennials, and Gen Xers said they would switch for better mobile banking apps and online capabilities. A few of the top activities that customers reported wanting to be easier:

- Filling out applications

- Waiting for credit/loan decisions

- Opening new deposit accounts

Not long ago, bank customers probably would have offered a definition of convenience centered around branch locations. Today, that convenience is almost always related to digital capabilities. Consumers expect easy-to-use self-service options and rapid results from every potential business engagement.

And according to a consumer banking survey by Bain & Company, the events that irritate customers often require a personal response, which can make the resolution more costly for the bank. The most commonly cited activities that make customer less likely to recommend a bank are:

- Dispute a bank fee

- Address a point-of-sale decline

- Dispute a charge

- Resolve a log-in issue

How loyalty-leading banks succeed

Banks with the highest level of customer satisfaction have fewer episodes in which customers need to dispute or resolve an issue. For example, the average number of bank fee dispute instances was 0.14 for a loyalty leader bank compared to 0.28 for a loyalty laggard bank (average number of episodes annually per US respondent). Loyalty leading banks often excel at straightforward and accessible digital processes, allowing their customers to use digital channels first and enabling their customers to resolve an issue at first contact.

Another survey of U.S. consumers by Cornerstone found that across every income level, a nearly equal percentage of consumers cited “digital banking tools” as one of the most important factors influencing their choice of banks. While younger generations may be leading the charge in demanding better digital capabilities, bank customers of all ages understand and recognize the importance of accessible digital banking.

3 ways a Digital Lending Platform supports banks’ customer retention goals

Blend’s Digital Lending Platform provides financial institutions with endless benefits — many of which can support and improve customer retention. Let’s take a closer look at three ways Blend can positively impact a bank’s customer loyalty goals.

1. Improved customer experience

Blend’s white label lending platform allows banks to offer a variety of digital capabilities that vastly elevate the customer experience. Our digital application is easy to navigate with a conversational interface designed to guide borrowers through the process. With an emphasis on mobile-friendly optimization, our omnichannel functionality allows the borrower to start and stop the account opening process across devices. Up to 60% of Blend applications can come through a mobile device, which proves the demand for flexibility across channels.

2. Greater efficiency for lenders

A unified Digital Lending Platform like Blend can dramatically cut down on time-intensive tasks like processing paperwork and manual data verification. By intelligently analyzing application data, Blend identifies issues that could cause delays, automates some resolution tasks, and drives predictive conditioning. Blend Verification empowers data to do the work for your teams so they can focus on what truly matters: building and expanding customer relationships.

3. Better visibility with system integrations

While Blend has many powerful integrations, including the GSEs and a wide variety of data providers, the customer relationship management systems may be the most beneficial to customer loyalty. Connecting a digital lending platform with a CRM can give lenders an immense advantage over competitors. Utilizing customer journey data allows lenders to create more personalized marketing offerings for their borrowers at the right time.

With a superior digital application experience, financial institutions can put their best foot forward and begin building customer loyalty on day one.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

Reduce Pre‑Closing Delays with Refreshable Asset‑Based Employment Checks

Learn how refreshable, asset‑based employment checks can reduce pre‑closing delays, cut last‑minute outreach, and align with DU®, LPA®, and agency expectations.

Read the article about Reduce Pre‑Closing Delays with Refreshable Asset‑Based Employment Checks

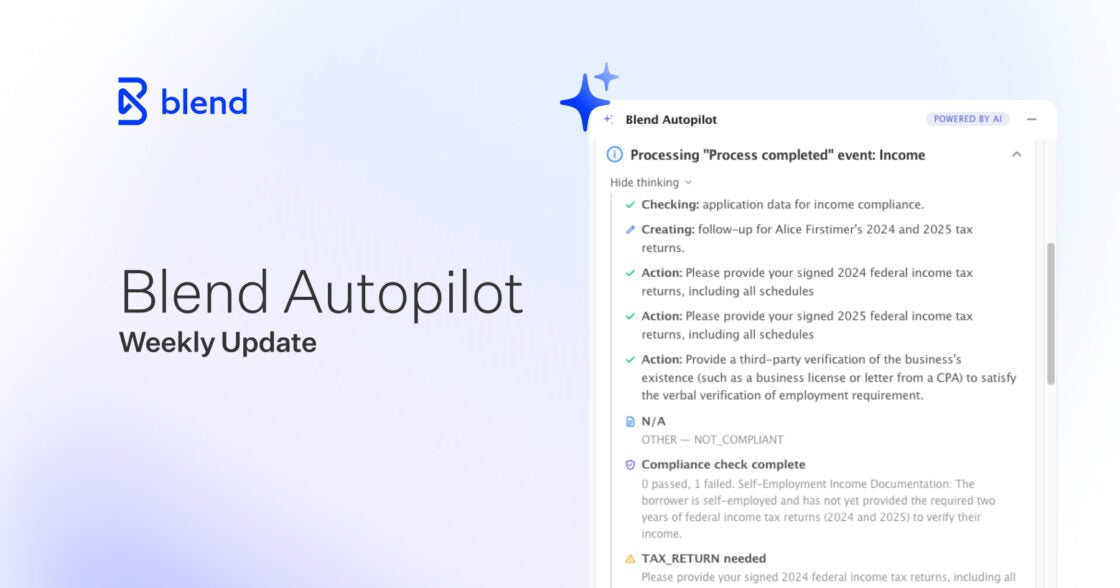

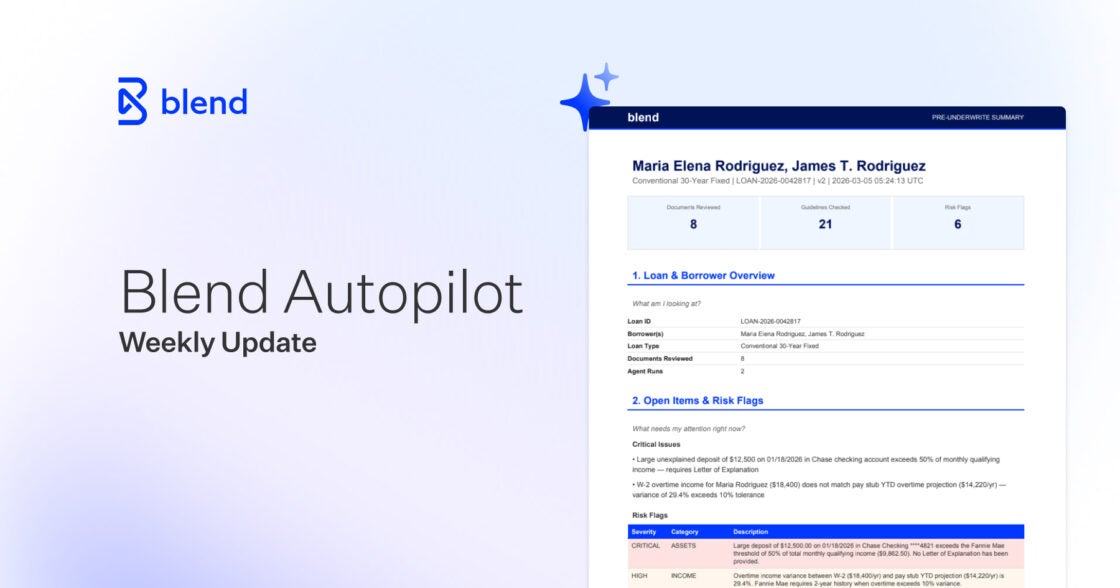

Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation

AI that handles edge cases automatically. See what shipped in Autopilot's third week of production.

Read the article about Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation

Blend Autopilot Week 2 Update: A Smarter Agent, Gift Fund Detection, and Transparent Income Calculations

This week’s Autopilot update brings a faster agent, gift fund detection, step-by-step income breakdowns, and native routing.

Read the article about Blend Autopilot Week 2 Update: A Smarter Agent, Gift Fund Detection, and Transparent Income Calculations