July 3, 2023 in Consumer Banking Suite

Your secret weapon in the battle for deposits

Explore the power of cross-sell within the mortgage application.

There is a secret weapon that modern financial institutions can leverage in the battle for deposits: timing.

Just like landing a good joke or a quick jab, timing is everything. Cross-sell offers are no different.

That’s why at Blend we built cross-sell for deposits into the mortgage application experience itself. The process is seamless, simple, and it works: customers convert. For credit unions, cross-selling deposits is a natural piece of the mortgage experience, but every financial institution (FI) can benefit from net new deposits.

Deposit accounts not only bolster your assets and cash flow, but also strengthen the overall health of your FI through optimized operations, critical automation, and of course, stronger customer relationships.

The end of channel hopping

Forced channel hopping can often be the kiss of death with new customers. Moreso, when borrowers can stay in their channel of choice, credit unions can ensure membership requirements are met before closing day. For all FIs, Blend’s Mortgage to Deposit Accounts cross-sell eliminates interdepartmental hand-offs when opening accounts, streamlining the entire process.

For the borrower, it’s simple and easy: everything they need to do is directly in the application. For the mortgage team, the process is easier because we’ve eliminated some tasks so they can focus on mortgage fulfillment. And for the FI itself, the cross-sell process is all that much easier because they no longer rely on mortgage teams to close those new deposits. It’s all built-in.

All of these benefits add up to improved profitability and revenue growth beyond the inherent value of net new deposits. With Blend’s Mortgage to Deposit Accounts cross-sell, FIs can convert new deposits while cutting costs, increasing operational efficiency, and streamlining workflows.

The right offer at the right time

If we put the customer first, everyone benefits.

The timing of deposits cross-sell within the mortgage application experience is successful because that’s when the customer is engaged and ready to convert. It works because that’s when the customer wants it to work.

Not only does this approach to cross-sell increase conversion and capture new deposits, but it also unlocks operational efficiency. Your mortgage teams can now focus on delivering excellence in mortgage experiences while deepening engagement and earning trust.

In today’s market, this is more important than ever. Of course, credit unions can leverage the integration of mortgage and deposits for their new members, but all financial institutions can benefit from implementing effective cross-selling strategies in the race for deposits. Deliver customer satisfaction, drive growth, and streamline your operations.

Looking to learn more on unlocking PFI status?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

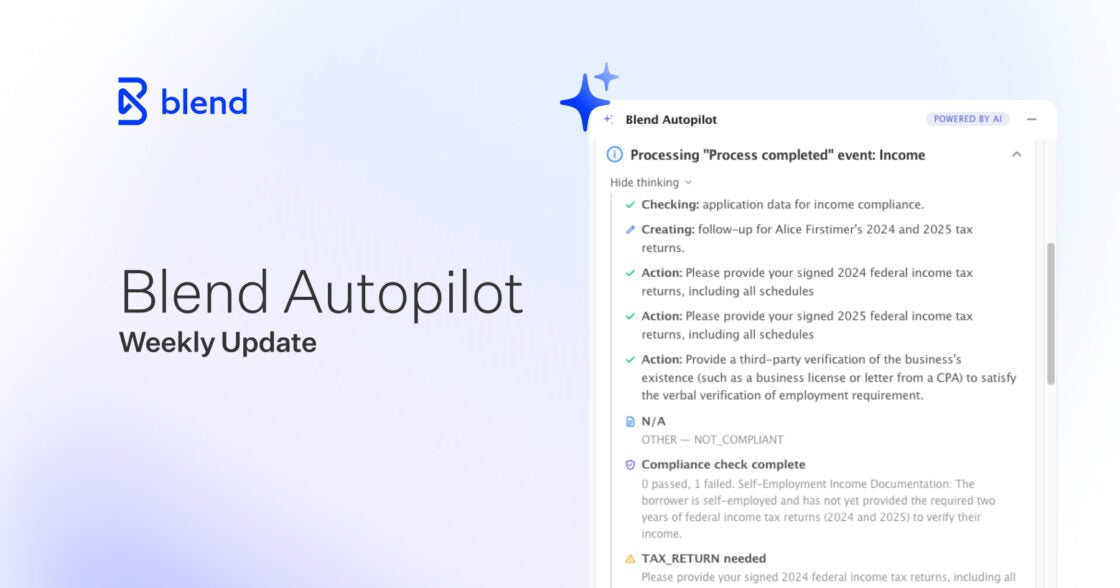

Blend Autopilot Week 2 Update: A Smarter Agent, Gift Fund Detection, and Transparent Income Calculations

This week’s Autopilot update brings a faster agent, gift fund detection, step-by-step income breakdowns, and native routing.

Read the article about Blend Autopilot Week 2 Update: A Smarter Agent, Gift Fund Detection, and Transparent Income Calculations

Blend Autopilot Week 1 Update: Pre-Underwriting Summaries, Income Calculation, and Smarter Follow-Ups

Reduce manual touchpoints. See how this week's Autopilot feature updates accelerate your time-to-close.

Read the article about Blend Autopilot Week 1 Update: Pre-Underwriting Summaries, Income Calculation, and Smarter Follow-Ups

Turning Home Equity Into a 2026 Growth Engine for Share, Loyalty, and Revenue

See how banks and credit unions can turn home equity into a 2026 growth engine with rapid, digital journeys that compete with fintechs and strengthen loyalty.

Read the article about Turning Home Equity Into a 2026 Growth Engine for Share, Loyalty, and Revenue