February 27, 2023 in Consumer Banking Suite

Your digital account opening process is key to winning back customers

How traditional banks are competing for (and winning) customer loyalty in an increasingly digital landscape.

Key Takeaways

-

Traditional banks have new and surprising opportunities to build long-term loyalty with their customers.

-

A successful deposit accounts solution can bring immense value to the relationship with your customers through rich data, personalized offerings, and deeper engagement.

In the race for customer loyalty, traditional banks are facing increased competition from fintechs, challenger banks, and other non-bank financial providers. Despite modernizing their financial products and delivering services across various channels, many of today’s banks are hamstrung by older technology that isn’t fully integrated. And many are unable to build new systems due to limited internal IT resources — often forced to rely on multiple software vendors for numerous point solutions while a rising swathe of competitors operate on a digital-first model that increasingly appeals to modern consumers.

Traditional FIs have the advantage for building long-term customer relationships

Nevertheless, financial institutions have several advantages that can be leveraged when competing against newer financial services providers. One of the key advantages that traditional FIs have is their ability to build and maintain relationships with customers over the long term. Unlike newer fintechs that are mainly used by consumers for transactional convenience such as digital payments or for high-yield, short-term hot money storage, traditional financial institutions have a unique opportunity to serve as trusted financial advisors and help consumers with their long-term financial wellness goals. Through building this level of trust, financial institutions can unlock more opportunities to deepen engagement with their customers and drive business revenue through cross-sell of additional products, rich data, and customer referrals.

If a traditional FI has the primary deposit account with a customer — where that customer receives their direct deposit and uses that account as a top-of-wallet card — they have a wealth of customer data to leverage. Personalized product offerings and proactive service, which can only come from rich data that a primary financial institution would have, is precisely what builds customer loyalty and wins against the competition in today’s market and beyond.

The pathway to winning customers for life

By delivering a personalized experience and ensuring the account opening process is uninterrupted, financial institutions can become top-of-wallet for their customers. In many cases, this begins with a deposit account. But if your deposit account opening process does not meet the digital demands and expectations of today’s consumers, you’ll continue to lag behind the competition.

A successful deposit accounts solution can bring immense value to the relationship with your customer through rich data, personalized offerings, and deeper engagement. For today’s consumers, the pathway to winning customers for life is through deposit accounts.

The right deposit account solution is driven by an intuitive, digital experience that guides the consumer through the entire process. And this process needs to be uninterrupted. At any point along the way, any friction, any manual elements that may slow or hamper the process are all brick walls for the consumer.

Blend Deposit Accounts solves for these barriers and pitfalls through a number of automated systems including a decision engine and identity verification that is nearly instant. Blend builds products that service today’s modern consumers delivering fast, simple, and uninterrupted service.

The pathway to PFI status

By delivering a personalized experience and ensuring the account opening process is uninterrupted, financial institutions can gain PFI status and become top-of-wallet for their customers. In many cases, this begins with a deposit account. But if your deposit account opening process does not meet the digital demands and expectations of today’s consumers, you’ll continue to lag behind the competition.

A successful deposit accounts solution can bring immense value to the relationship with your customer through rich data, personalized offerings, and deeper engagement. For today’s consumers, the pathway to PFI status is through deposit accounts.

Learn how to build loyalty and deepen engagement with your customers

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

How Agentic AI Can Transform Mortgage Fulfillment and Cut Cost per Loan

The average mortgage still takes 38 to 42 days to close and costs over $12,500 to produce. Agentic AI changes that by transforming every phase of fulfillment.

Read the article about How Agentic AI Can Transform Mortgage Fulfillment and Cut Cost per Loan

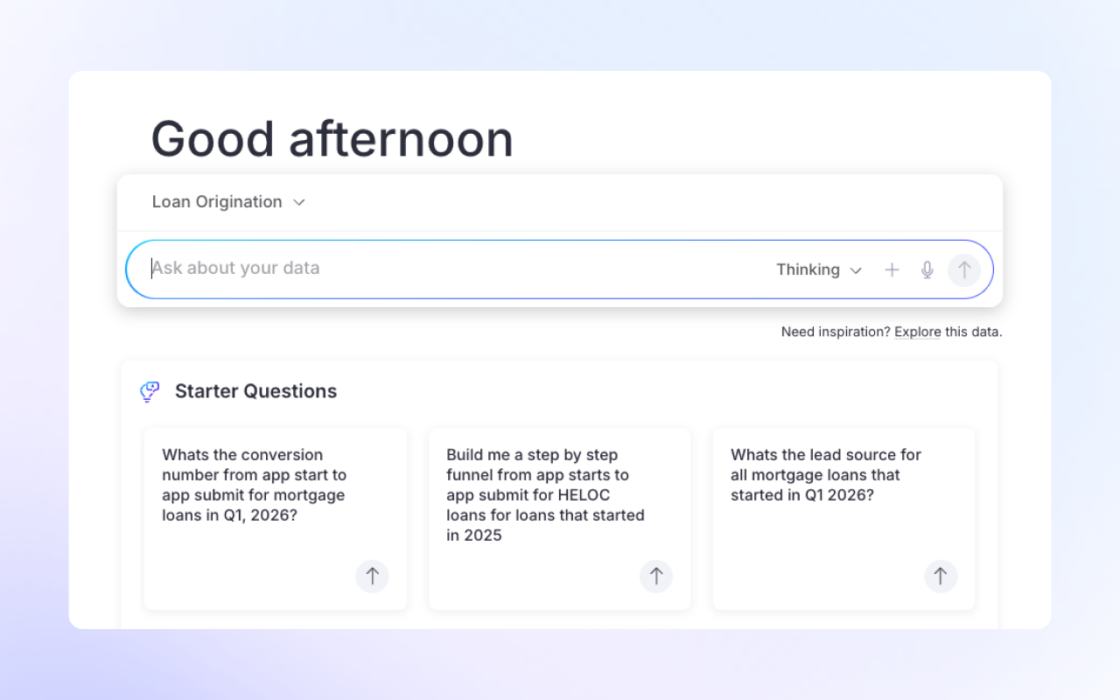

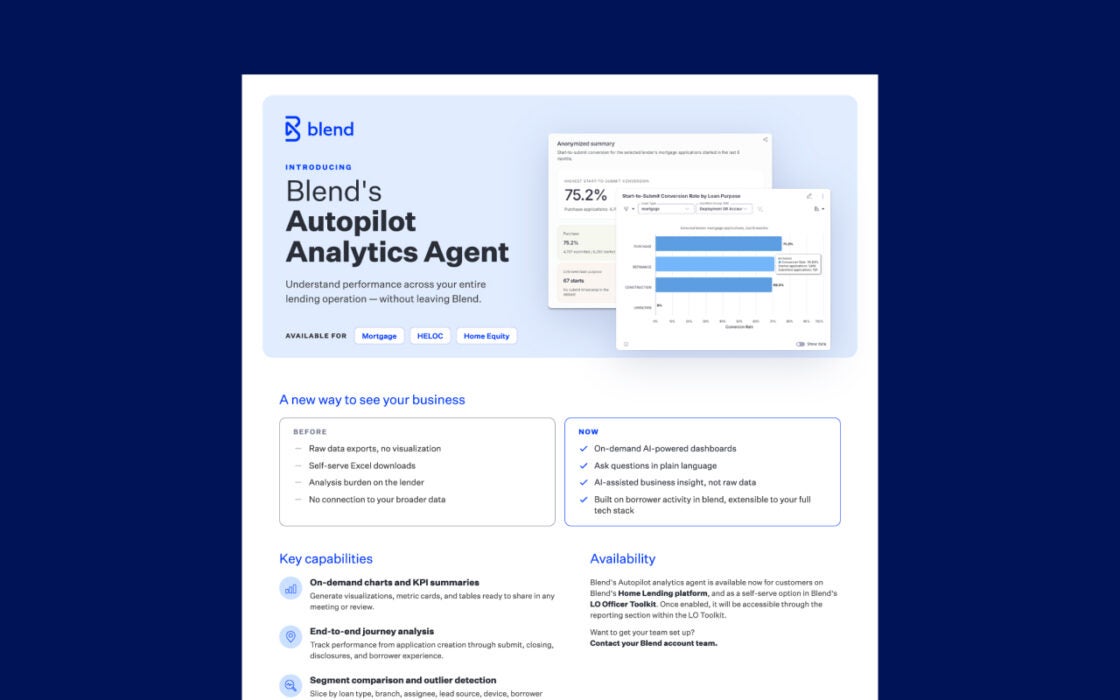

Blend’s Autopilot Analytics Agent

Understand performance across your entire lending operation — without leaving Blend.

Start learning about Blend’s Autopilot Analytics Agent

Make Every Data Question an Actionable Answer: Introducing Autopilot Analytics Agent

Autopilot analytics agent helps lenders act faster with plain-language answers, dashboards, and connected insight.

Read the article about Make Every Data Question an Actionable Answer: Introducing Autopilot Analytics Agent