March 21, 2023 in Consumer Banking Suite

Bridging the digital gap

The rise of mobile and the importance of hybrid experiences.

Successful onboarding with new account customers is absolutely crucial to building a strong relationship and gaining primary financial institution (PFI) status. Many financial institutions focus on conversion, but conversion without utilization will only get you so far. And oftentimes, the path to high utilization is blocked by a complex customer experience or a digital gap in the customer journey.

According to a report from PwC in 2021, 21% of surveyed consumers would prefer to open a new deposit account digitally but are unable to do so. Whether that customer is then directed to visit a banking branch or forced to channel hop to a call center, that customer journey is interrupted. And interruptions, obstacles, or detours cause abandonment.

A few more ways to bridge your knowledge gap…

Subscribe for industry trends, product updates, and much more.

Today’s financial institutions need to meet consumers where they are. And that’s increasingly online. The majority of consumers (61%) use digital banking services at least once a week. And 22% of new checking account owners chose a digital-only bank (with no physical branches) during the last 12 months. For many FIs, this digital gap is growing.

And the rising cadre of neobanks are reaping the rewards. In fact, 57% of millennials and 64% of Gen Z consumers now say they have a financial account with a nontraditional institution. And perhaps more importantly, 17% of consumers holding accounts with nontraditional financial institutions identify that digital bank as their primary financial institution — a sentiment within this segment that has doubled in the last year.

All of these insights point to a single conclusion: today’s consumers are looking for a simple, digital new account opening solution that guides them through onboarding to high utilization. Blend recently published an ebook exploring this solution: Seize the opportunity to gain PFI status with modern consumers.

Not only are we seeing financial institutions struggle with digital and omnichannel engagement, but the path to PFI status is increasingly challenging. The average banked U.S. consumer has 14 accounts held across 4.4 financial service providers, including credit card companies, person-to-person (P2P) providers, and buy now, pay later (BNPL) services.

That said, achieving PFI status is possible with the correct strategy. One differentiating advantage that traditional providers can leverage is their hybrid service, including human engagement in branch and on the phone. This is one channel the neobanks don’t have, and the best opportunity to build loyalty. One meaningful, in-person interaction can drive emotion more than hundreds of digital interactions.

At Blend, we explored this hybrid experience advantage in our webinar, “The surprising opportunities to gain trust in our post-loyalty economic downturn,” which is now available to watch on demand.

Whether in person or online — whatever channel the consumer chooses to engage through — it’s critical that FIs provide a seamless, simple process for new account opening. This is the entry point that will define the entire customer relationship. It’s true what they say — you only get one chance to make a first impression.

With today’s modern consumers, that first impression is often digital. And if it’s not where they first engage with an FI, it’s most certainly part of an omnichannel, hybrid journey.

At Blend, we build digital products to make banking simple. And part of what that means is providing seamless, omnichannel customer experiences. It’s the straightest path to PFI status. And it begins with a digital account opening solution like Blend Deposit Accounts.

Are you ready to bridge the digital gap for new accounts?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

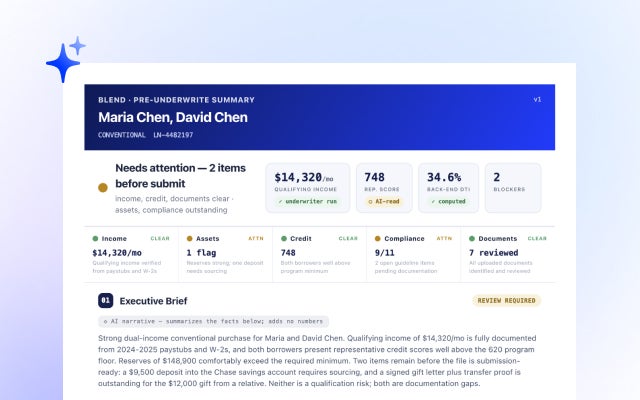

Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Every figure, every source. See how Autopilot's latest update makes pre-underwriting faster to act on.

Read the article about Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

The mortgage market is projected to reach $2.2 trillion in 2026, but flat isn't the same as easy. With per-loan costs exceeding $12,500, discover why cost per loan is the…

Read the article about Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

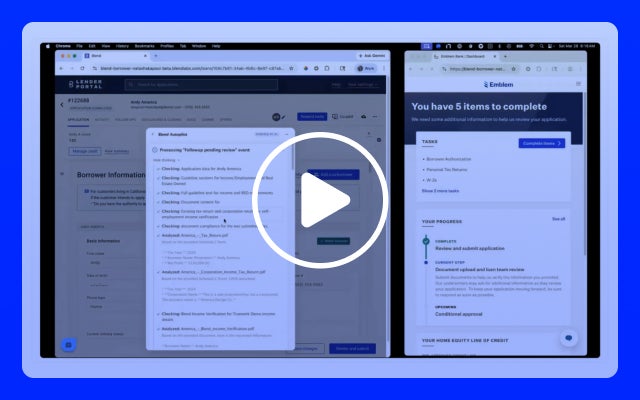

Five-Minute Home Equity: How to Outpace Fintechs and Win Member Loans

How credit unions are using AI to close HELOCs in minutes and outcompete fintech lenders.

Watch video about Five-Minute Home Equity: How to Outpace Fintechs and Win Member Loans