May 5, 2023 in Consumer Banking Suite

How to attract deposits in a competitive banking market

Instant gratification and convenience.

There are some headwinds in the banking industry today that have put a greater emphasis on trying to capture the right customer while keeping existing customers happy, all while properly managing the balance sheet. When interest rates were low and steady, it didn’t matter as much for deposit accounts because there were fewer rate shoppers and people needed to put their cash somewhere. Account balances increased, credit rates were low, and all was good. That was then, but this is now.

Most customers have multiple relationships with different institutions, and choosing a primary institution can be challenging. Oftentimes it seems that FIs go out of their way to ensure that their institution does not earn primacy, simply by creating complex and inefficient onboarding processes that either lack modern technology or are hindered by bank policy. Too often, customers will open a new account with the best intentions, but then end up forgetting about it unless they’re able to see the value of putting your institution at the center of their financial journey.

Need help making a decision?

Subscribe for industry trends, product updates, and much more.

So, why aren’t customers aren’t making your bank their primary financial institution? It might have started at the very beginning. Of customers who opened a new account, 61% did not immediately fund their account and only 37% self-provisioned for mobile or online banking¹. It seems that this is a problem and should be a much higher percentage.

If banks want to capture customers at account opening, they must promote the account to fund and set up access at the time of account opening, not down the road when banks may have forgotten. Also, adding online and mobile banking with bill pay, switching over or setting up direct deposit, and providing digital wallet setup should happen before the customer navigates away from the onboarding process.

¹IDC Financial Insights North American Consumer Banking Channel Preference Survey, January 2023 n=2750

Here are a few ways to ensure that both new customer conversion and immediate onboarding are optimized:

- Personalized outreach that provides incentives that are suited to the needs of that individual and can deepen the relationship

- A modern website that adapts to the device being used by the individual at that time

- Efficient experiences with the ability to utilize multiple touchpoints to provide necessary documentation (i.e., camera on phone to upload license or desktop computer to upload PDF or scanned images)

- Workflow optimization that allows bank employees and customers to fully understand where they are in the process, particularly for those requiring approval and additional documentation

- Proven value propositions of working with your institution, including educating customers on the safety of banking with you, on your commitment to the community, and that you value their time

- Self-service provisioning with a few clicks to allow new customers to set up a digital wallet, which is particularly helpful for immediately funding a deposit account; if a debit card is provided, that can also be easily added to the digital wallet of their choice

- Investing in digital and finding ways to improve the digital experience by deploying innovation in a low-code environment that leverages existing workflows and the use of best practices learned

These are just a few ideas that will help institutions stay competitive and create more lifetime value for their customers in our current economic environment. Modern and efficient digital access that can leverage multiple touch points — mobile phone, website, tablets, branch visits, or conversations with a specialist — will mean the difference between having someone just add another checking account or having someone add their new main checking account relationship. Without a simple and intuitive process, the industry will struggle to get beyond the 61% of customers opting to not immediately fund their new deposit account. Once funded, give the customer an easy path to make your institution their go-to account for their current and future financial needs.

Curious to learn more about Blend’s Deposit Accounts solution?

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

How Lenders Can Reach More Bilingual Borrowers Without Adding Friction

Bilingual borrowers are a growing market. See how clarity, not just translation, builds confidence and keeps loans moving.

Read the article about How Lenders Can Reach More Bilingual Borrowers Without Adding Friction

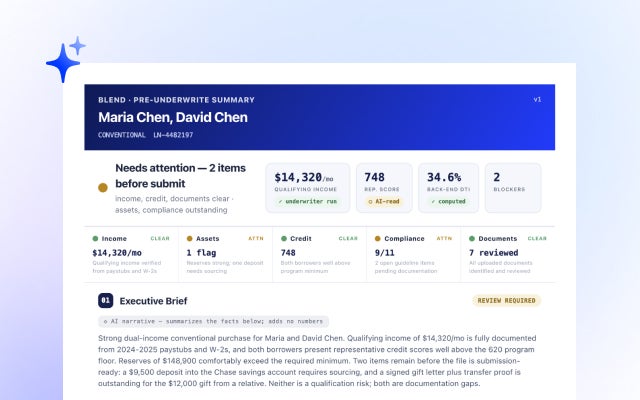

Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Every figure, every source. See how Autopilot's latest update makes pre-underwriting faster to act on.

Read the article about Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

The mortgage market is projected to reach $2.2 trillion in 2026, but flat isn't the same as easy. With per-loan costs exceeding $12,500, discover why cost per loan is the…

Read the article about Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan