March 3, 2026 in Blend momentum

From Upload to Underwriting in 15 Seconds: Introducing Blend Autopilot

Borrowers don't wait until business hours. Your origination workflow shouldn't either. Blend Autopilot is an intelligent agent that reviews documents, generates needs lists, and keeps loans moving forward in real time.

Every loan officer knows the feeling. A borrower uploads their W-2 at 10:47 PM on a Tuesday. The document sits in a queue. The next morning, someone reviews it, notices the stated income doesn’t match, creates a follow-up, and emails the borrower. Three days later, the borrower responds. A week has passed. One document.

At Blend, we believe the workflow shouldn’t pause when the loan officer closes their laptop. It should keep moving. Every document uploaded, every section completed, every condition returned from AUS. These are moments of momentum, and momentum shouldn’t have to wait until morning.

That’s the Blend thesis: the origination workflow should be powered by agents running continuously in the background, reading documents, checking compliance, creating follow-ups, and updating application data. So that when a borrower acts at 10:47 PM, the process responds in seconds, not the next business day. AI working in collaboration with the borrower as part of the loan team.

Today we’re shipping the first agent built on that thesis: Blend Autopilot.

If you’re already a Blend customer, you can turn Blend Autopilot on right now with a single toggle in your Blend Setup Center, and during the preview period it is free to activate and use. This is the first of many. Our commitment to our customers is to be the partner that brings agents across every step of the origination lifecycle, continuously shipping, improving, and expanding what’s possible.

The problem with manual mortgage origination

Mortgage origination still runs on a manual, turn-taking process in which borrowers act, then lenders review, then borrowers respond again. They can’t move in parallel, and despite decades of technology investment, that fundamental problem hasn’t been solved.. The result is a process that takes 30 to 60 days, costs $11,000+ per loan, and loses borrowers along the way. Borrowers act in bursts. They upload three documents at midnight, complete their income section during lunch, respond to a follow-up on the bus. But the review process is batch-oriented: a human reviews the queue the next business day.

This creates three compounding problems:

- No Feedback at the Moment of Engagement. Borrowers are most motivated at the moment they’re actively engaged in the application, ready to take the next step immediately. But nothing comes back. Did it work? Do I need to do anything else? Review happens the next business day. By the time a follow-up is created, the borrower has moved on. 53% of borrower interactions happen outside of business hours.

- LOs Stuck on Low-Value Work. Loan officers spend hours each day on routine document review and follow-up creation. It is work that does not require judgment, just attention, and it is the most expensive attention in your pipeline.

- Inconsistent Loan Quality. Two loan officers reviewing the same W-2 might create different follow-ups, cite different guidelines, or miss different discrepancies. The quality of the underwriting depends on who’s working that day.

Blend Autopilot eliminates all three.

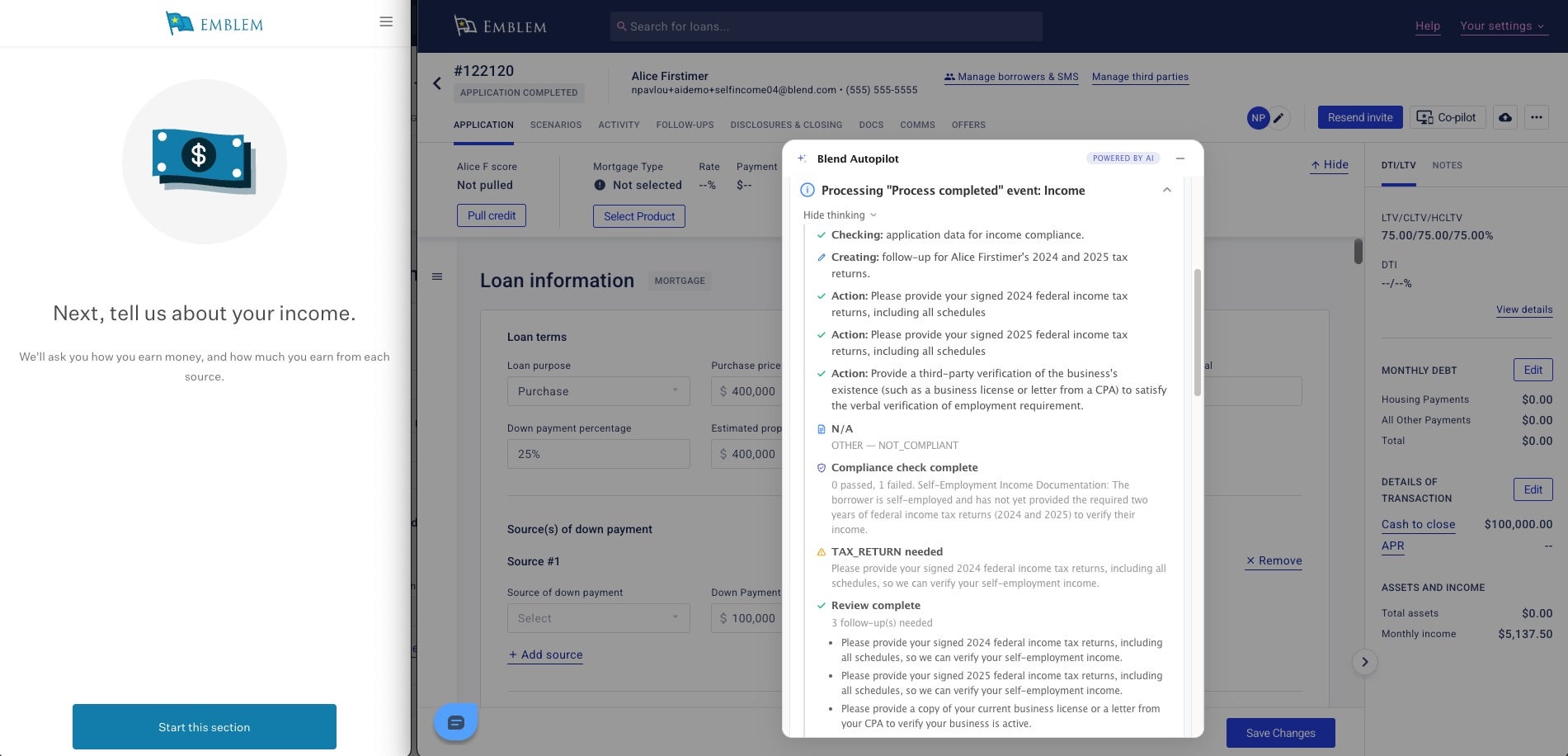

How Blend Autopilot automates mortgage document review in seconds

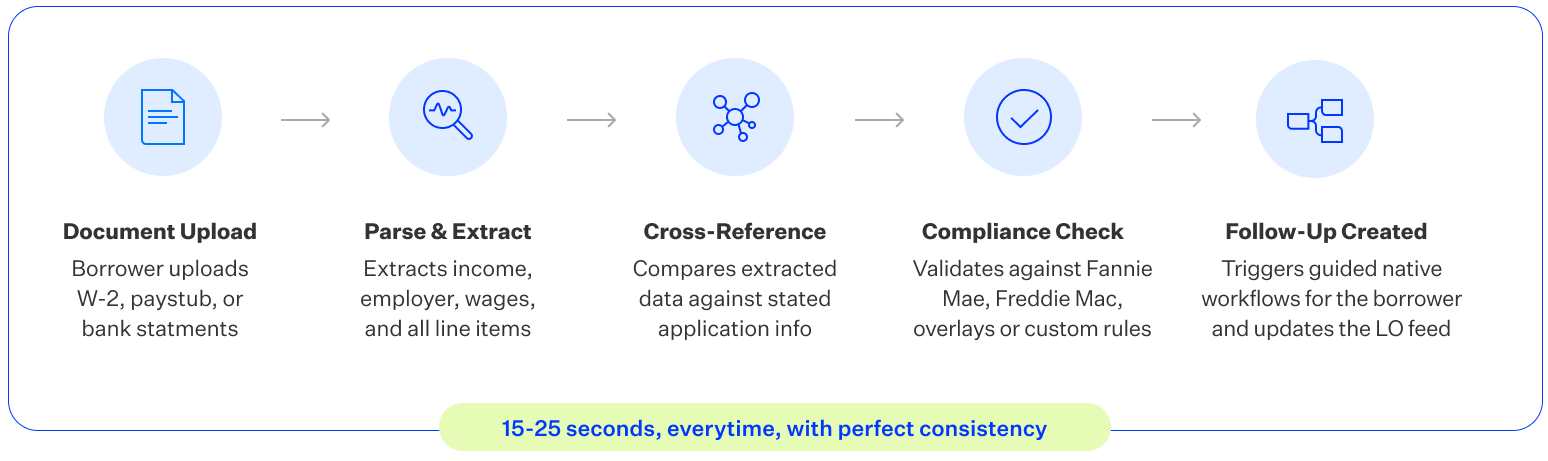

Blend Autopilot activates automatically when a borrower takes action on their application. It performs the same compliance review your team does manually, checking documents against guidelines, identifying discrepancies, creating follow-ups, and updating application data, but it does it in 15-25 seconds, every time, with perfect consistency.

Here’s what happens when a borrower uploads a W-2:

Within 15 seconds, the agent:

- Parses the document: Extracts employer name, wages, withholdings, bonus income, and all line items.

- Cross-references against the application: Compares extracted income ($231,000) against the borrower’s stated income ($230,400). If the numbers differ, it updates the application data to match the documentation.

- Checks compliance: Consults the applicable guidelines (Fannie Mae, Freddie Mac, your overlays, or your custom rules) and identifies issues. For example: “$38,000 in bonus income requires 2-year verification per Fannie Mae B3-3.1-01.”

- Creates follow-ups: Triggers the right native workflow. Instead of a generic “please upload a document” email, it provides a guided, in-app experience that tells the borrower exactly what is needed and why.

- Streams results in real time: The loan officer sees a rich activity feed with income breakdowns, compliance citations, and follow-up details. The borrower sees a status banner and a badge on their To-Do tab.

And this doesn’t just happen for document uploads. The agent activates on four types of borrower events:

| Trigger | What the agent does |

|---|---|

| Document upload | Parses, extracts, cross-references, creates follow-ups |

| Section completion | Reviews stated info, generates initial needs list immediately |

| Follow-up response | Re-reviews with new info, computes deltas, resolves items |

| AUS submission | Maps AUS conditions to borrower-actionable native workflows |

53% of borrower interactions happen outside of business hours. The agent doesn’t have business hours.

Why Blend Autopilot is different from rules-based mortgage automation

Contextual intelligence, not rules.

Most automation in mortgage is rules-based: “If deposit > 50% of monthly qualifying income, trigger LOE.” The problem with rules is they can’t think.

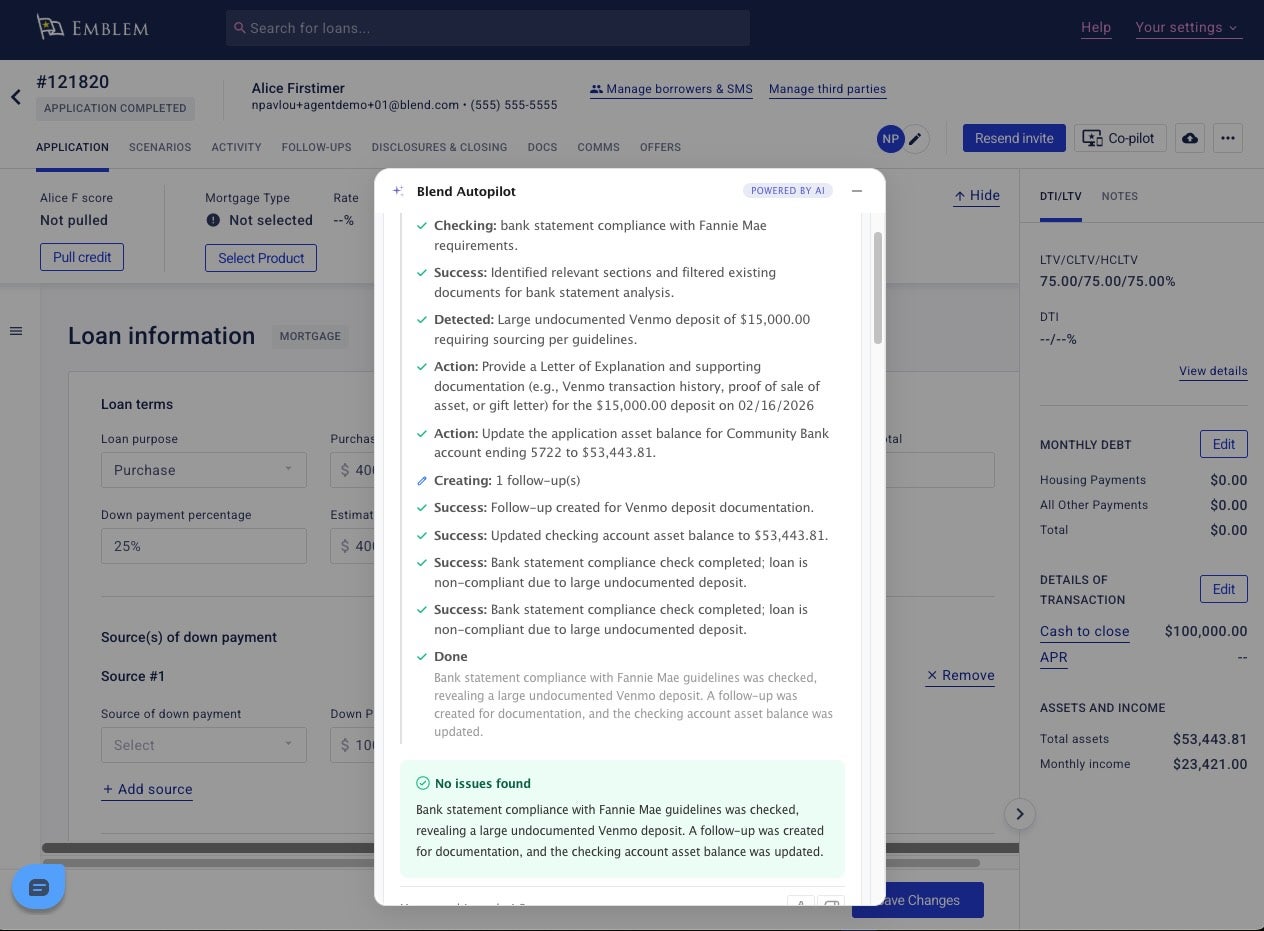

Consider a bank statement with two deposits: a $15,000 Venmo transfer and a $12,000 direct deposit from “ACME CORP PAYROLL.”

A rules engine triggers a Letter of Explanation for both deposits because both exceed the threshold. The borrower gets two LOE requests, one of which is completely unnecessary. They’re confused, they call their loan officer, the process slows down.

Blend Autopilot reads context. It recognizes that “ACME CORP PAYROLL” is a payroll deposit and skips the LOE. It triggers a Large Deposit LOE only for the Venmo transfer, the one that actually requires sourcing. Just like a human would.

The same intelligence applies everywhere:

Credit inquiries: Two mortgage-shopping inquiries from other lenders? Skipped, because the agent recognizes rate-shopping related to the current application. A credit card inquiry from a department store? That gets an LOE.

DU conditions: Three conditions returned from Desktop Underwriter, but only two are borrower-actionable? The agent creates guided workflows for those two and keeps the lender-internal condition where it belongs, with the lender.

The result: Up to 50% fewer unnecessary follow-ups compared to a rules engine. This matters. Stratmor data shows 36% of borrowers report having to provide the same document multiple times, causing an 11-point NPS drop. Even worse, 9% considered their lender’s document requests unreasonable, resulting in a 70-point NPS drop, the most significant negative impact to borrower experience of any phase in the mortgage process. Fewer follow-ups means less borrower fatigue, faster closings, and lower fall-out rates.

Supporting agency, overlay, and custom mortgage guidelines

Every lender is different. Some are pure Fannie Mae shops. Some run Freddie Mac. Some have overlays on top of GSE guidelines. Some have entirely custom guidelines for portfolio products.

Blend Autopilot supports four guideline modes, configurable per product type:

| Mode | How it works | Best for |

|---|---|---|

| Fannie Mae | Live Selling Guide lookup | Conventional mortgages |

| Freddie Mac1 | Live Seller/Servicer Guide lookup | Freddie Mac loans |

| Overlay | GSE base (Fannie or Freddie) + your custom overlay rules | HELOANs with custom CLTV limits |

| Custom | Your guidelines only, with no external lookups and the fastest processing | HELOCs, portfolio products |

1 Freddie Mac support coming soon.

A multi-product lender can run Fannie Mae for conventional mortgages, Freddie Mac with an overlay for HELOANs, and fully custom guidelines for their HELOC portfolio, all from the same agent, configured per product type.

The agent correctly cites its sources. When it flags an issue under Fannie Mae mode, the citation reads “(Fannie Mae B3-3.1-01).” Under overlay mode, you’ll see both “(Freddie Mac 5601.1)” and “(Lender Overlay)” depending on which rule applies. Your loan officers always know where a finding came from.

Intelligent native workflows for modern mortgage lending

When the agent creates a follow-up, it doesn’t send a generic email saying “please upload a document.” It triggers Blend’s native guided workflows, the same structured experiences your borrowers already know.

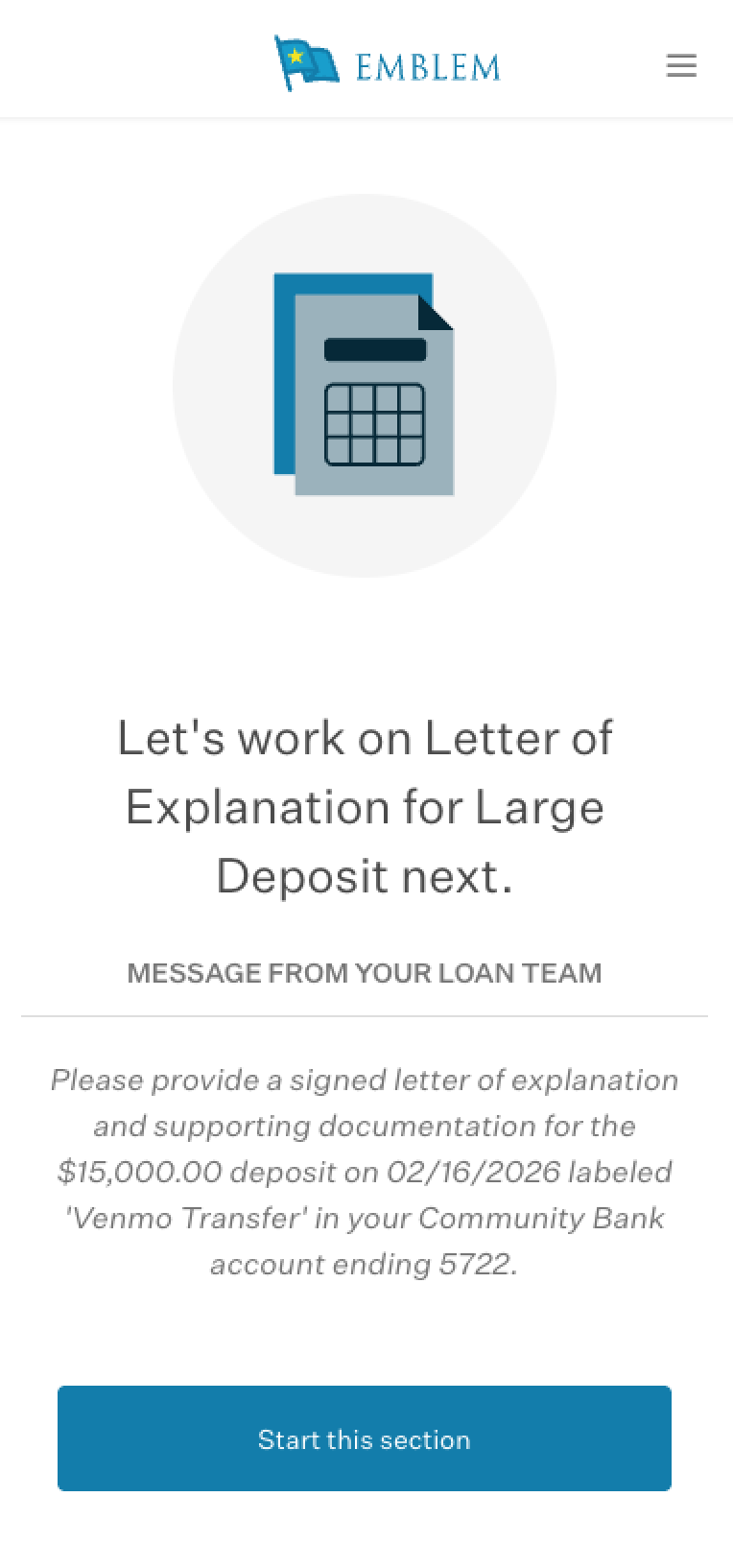

A Large Deposit LOE walks the borrower through a guided, in-app experience: “We found a $15,000 deposit on 1/15/2026. What is the source of this deposit?” with branching options (transfer, gift, sale of asset) that collect exactly the right information. A Credit Inquiry LOE is linked to the specific inquiry on the credit report. A Late Payment LOE is linked to the specific liability.

The agent links each workflow to the correct entity, the specific credit inquiry ID, the specific liability ID, the specific deposit. When the borrower completes the workflow, the data flows back to exactly the right place in the application. The difference between a generic email asking for a document and a guided workflow linked to the specific issue is the difference between a borrower who calls their loan officer confused and a borrower who completes the follow-up in two minutes.

Real-time borrower experience during mortgage journey

When the agent is working, the borrower knows. A status banner at the top of the screen shows the borrower what’s happening in real time:

- “Looks good! No issues found.”: The document checks out, no further action needed.

- “We’re reviewing your information…”: Appears while the agent is analyzing.

- “A few items needed.”: If follow-ups are created, with a direct link to view tasks.

When new follow-ups are generated, a badge appears on the borrower’s task list, using the same unread-notification pattern familiar from messaging apps. The borrower gets immediate confirmation that something happened — no waiting until the next business day to find out if their upload was received or if more is needed.

Why this matters: Blend platform data shows that when borrowers receive automated follow-ups at the point of engagement, 65% are completed immediately. That’s proof that borrowers act when the process meets them in real time. With Blend Autopilot delivering faster, more contextual follow-ups, we’re targeting a 20% improvement in borrower engagement during the review window and a 30% reduction in time-to-follow-up-action.

The loan officer’s AI colleague

On the lender side, loan officers see a rich, real-time activity feed that narrates what the agent found with full detail.

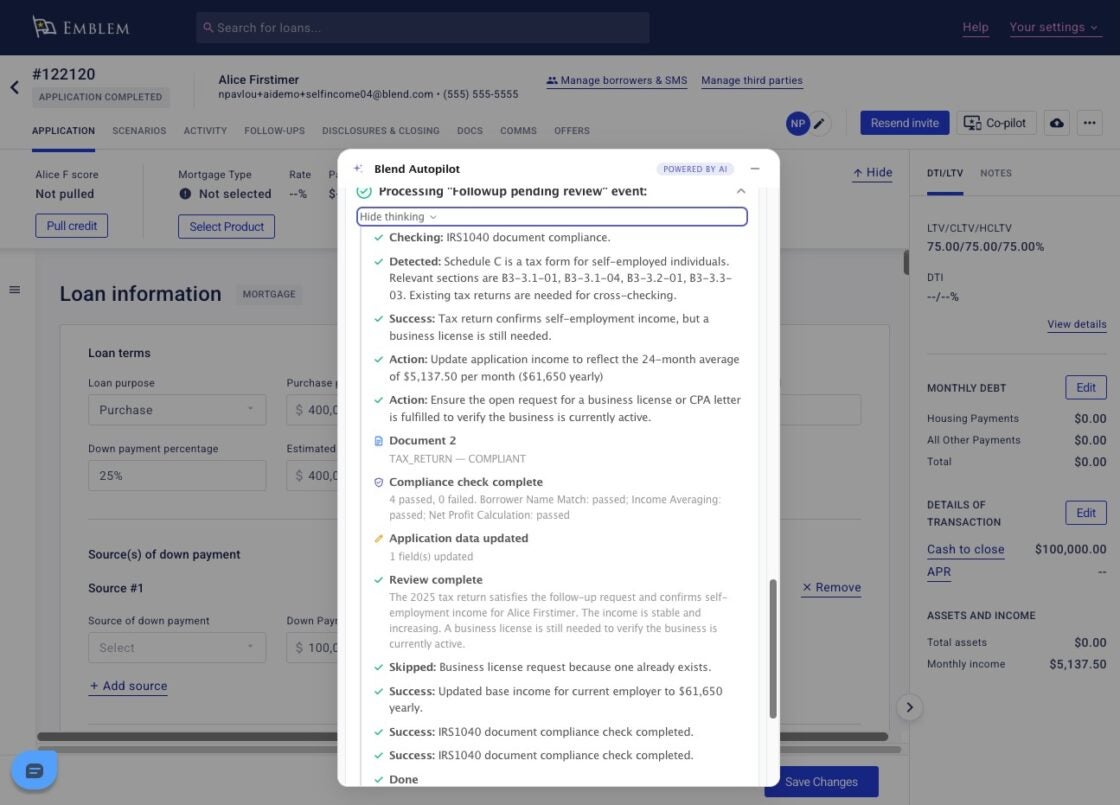

When a tax return is reviewed, the feed shows exactly what the agent extracted, what it calculated, and what it did about it, all within seconds.

Here’s what happens when a self-employed borrower uploads their Schedule C:

The agent immediately:

- Parses the document: Extracts gross receipts, itemized business expenses, net profit, and depreciation from the Schedule C.

- Applies GSE guideline logic: Depreciation is a non-cash expense that reduces taxable income but doesn’t affect the borrower’s actual cash flow. Per Fannie Mae B3-3.2-01, the agent adds it back — turning a $57,500 net profit into $59,350 in qualifying income.

- Cross-references against the application: The borrower stated $66,000 in annual self-employment income, but the Schedule C supports $59,350. The agent flags the discrepancy and updates the application to match the documented amount.

- Checks the two-year history requirement: Self-employment income requires a two-year history to be used as qualifying income. The agent requests the next year’s tax return to complete the verification.

- Skips what’s already done: A tax return follow-up already exists on the file? Skipped. The agent doesn’t create duplicate work.

When the second year’s Schedule C is uploaded, the agent doesn’t just replace the number, it averages both years, calculating a 24-month average of $5,137/month as the qualifying self-employment income. One calculation that would take a loan officer 15–20 minutes of manual review, guideline lookup, and data entry, done in seconds.

The loan officer doesn’t have to open the tax return. They don’t have to manually subtract expenses from gross receipts. They don’t have to remember which non-cash items to add back. They don’t have to look up Fannie Mae’s self-employment income requirements. The agent has already done all of it, with guideline citations, line-item numbers, and clear explanations.

And when it flags the income discrepancy, the loan officer instantly sees the stakes: the borrower stated $5,500/month, but the documented 24-month average supports $5,137/month. That clarity means the loan officer can have an informed conversation with the borrower instead of spending time reconstructing the math themselves.

Proactive mortgage needs lists before any documents are uploaded

Most AI document review tools are reactive: the borrower uploads something, the AI reviews it. Blend Autopilot goes further.

The moment a borrower completes a section of their application, whether income, assets, or employment, the agent reviews their stated information against guidelines and generates the initial needs list immediately.

Instead of waiting for a loan officer to review the application and create a needs list the next business day, the borrower knows what to upload within 15 seconds of completing a section: “Based on your income details, we’ll need your 2025 W-2 from Acme Corp, your most recent pay stub, and a year-end pay stub to verify bonus income.”

This eliminates the dead time between “application submitted” and “here’s what we need,” a gap that typically costs 1-3 business days and is one of the biggest drivers of borrower drop-off. The borrower just completed their income section. They’re still on their phone. Now they know exactly what to upload, and based on Blend platform data, 65% of the time they do it right then.

Activate Blend Autopilot yourself, today

No engineering tickets. No weeks of legal review. No implementation project.

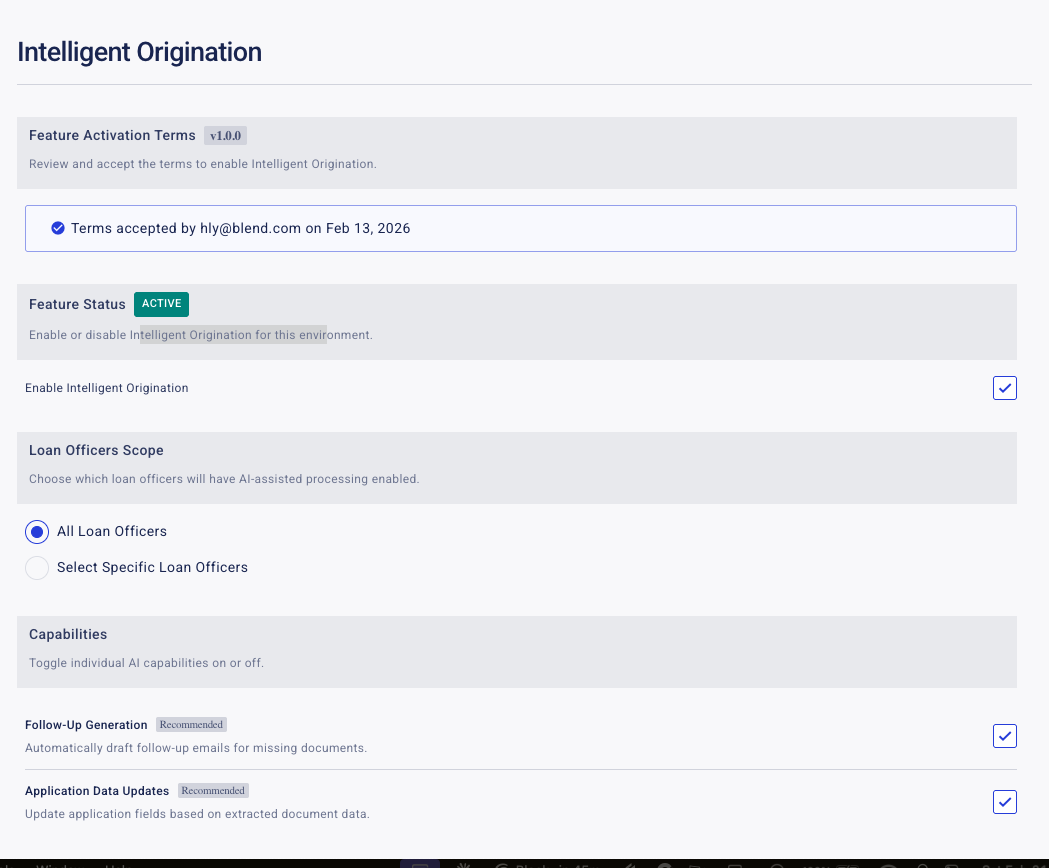

Blend Autopilot is activated through a self-serve panel in Blend’s Lending Config Center. A lender admin can go from “interested” to “live” in under an hour.

Blend Autopilot is currently in preview and free to activate for all Blend customers.

Getting started is as easy as:

- Review and accept terms: Structured as a feature activation under your existing MSA, not a new contract. Your legal team already approved the MSA. This is just turning on a feature.

- Enable the agent: A single toggle. Disable at any time, and the kill switch takes effect within 5 minutes.

- Choose your loan officers: Roll out to all LOs at once, or start with a pilot group using a searchable allowlist.

- Configure capabilities: Toggle Follow-Up Generation and Application Data Updates independently.

Every action is audited with a full trail: who accepted, when, what version. PDF receipts are generated and stored immutably for 7 years per banking regulations.

Measure the ROI and operational impact of Blend Autopilot

Every lender executive asks the same question: “How do I know this is working?”

The Agent Value Dashboard gives you the answer in real time. It tracks:

- Documents Reviewed: Every document the agent analyzed.

- Issues Detected: Compliance issues, discrepancies, and missing documentation flagged.

- Follow-Ups Created: Native workflows and document requests generated without LO involvement.

- Fields Updated: Application data fields corrected or populated automatically.

Filter by date range, see trends over time, and quantify the impact: “847 documents reviewed this week × 8 minutes average per manual review = 112 hours saved.”

These aren’t vanity metrics. Every number maps to work your operations team didn’t have to do and your borrowers didn’t have to wait for. In 2025, the Blend platform processed 3M+ home lending applications and 39.7M follow-ups. The Value Dashboard lets you see exactly how the agent is performing across your share of that volume.

AI mortgage automation built for bank and compliance teams

We built Blend Autopilot knowing it would need to satisfy bank compliance officers and regulators:

- Non-decisioning tool: The agent assists. It does not make credit decisions. All output is reviewed by a human loan officer before any lending decision is made.

- Ephemeral data processing: Borrower data is processed in real time and never used to train foundation models. Zero data retention by the AI provider.

- Full audit trail: Every activation, configuration change, and terms acceptance is logged with who, when, what, and how. 7-year retention per banking regulations.

- Kill switch: Disable agent processing in under 5 minutes. In-flight requests complete normally, with no data loss or orphaned state.

- Regulatory alignment: Designed for compliance with GLBA, ECOA, Regulation B, and FCRA.

- Pilot-friendly: Restrict agent to specific loan officers before rolling out organization-wide. Measure results before committing.

Why now is the time to activate Blend Autopilot

| Metric | Impact |

|---|---|

| Time from upload to review | 15-25 seconds (vs. next business day) |

| Time to activate | Under 1 hour (vs. weeks of legal + engineering) |

| Unnecessary follow-ups | Up to 50% reduction vs. rules engines |

| Guideline modes | 4 — Fannie Mae, Freddie Mac, Overlay, Custom |

| Trigger types | 4 — document upload, section complete, follow-up response, AUS submission |

| Kill switch | Under 5 minutes to take effect |

| Data training risk | Zero — all processing is ephemeral |

The mortgage industry has been waiting for AI that actually fits into the lending workflow, not a separate tool, not a chatbot, not a demo that looks great on stage but requires six months of integration work.

Blend Autopilot is different because it’s built into Blend. It uses the workflows your borrowers already know. It follows the guidelines you already use. It creates follow-ups through the native experiences your team already operates. And it gives both your borrowers and your loan officers real-time visibility into what’s happening and why.

Activate Blend Autopilot in the Lending Config Center today to start your free preview and bring real-time momentum to your origination workflow.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

Blend Launches Autopilot, Completing Loan Origination Reviews in 15 Seconds

The first AI agent of Blend Intelligent Origination works inside existing lender workflows and guidelines to deliver real-time compliance review, automated follow-ups, and full borrower visibility.

Read the article about Blend Launches Autopilot, Completing Loan Origination Reviews in 15 Seconds

Blend Autopilot: AI That Keeps Loans Moving Forward

The AI Agent that reviews documents, checks compliance, and created follow-ups in 15 seconds.

Start learning about Blend Autopilot: AI That Keeps Loans Moving Forward

From Rules to Reasoning: Intelligent Origination as the Next Chapter in Lending

Discover how agentic AI is making "self-driving lending" a reality. Blend’s Intelligent Origination gives AI the tools to execute end-to-end workflows with precision and oversight.

Read the article about From Rules to Reasoning: Intelligent Origination as the Next Chapter in Lending