March 25, 2026 in Blend momentum

Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation

Autopilot Weekly Update: Week 3

Last week we took Blend Autopilot on the road to Las Vegas for the ICE Mortgage Technology Experience conference and caught up with many of you in person. The reception was overwhelming: lenders already running Autopilot wanted to talk about what they’re seeing, and lenders who haven’t yet wanted to know how quickly they could get started.

While we were there, Nima sat down with HousingWire to talk about the vision behind Autopilot. At the same time, the team kept rolling out new capabilities. Keep reading for highlights from that conversation and what’s new in Autopilot this week.

Subscribe to Autopilot updates

Nima Ghamsari on why Blend built Autopilot

At ICE Experience, Co-Founder and Head of Blend, Nima Ghamsari, sat down with HousingWire’s Allison LaForgia to talk about where AI is actually delivering value in mortgage origination, and where the industry still has a long way to go.

The full conversation is worth watching. Here are the key ideas.

Ghamsari describes Autopilot as a system of “ambient agents, agents that are working in the background as the consumer is entering any data field, as they’re uploading any document.” As that happens, “Autopilot is reading it, understanding it, underwriting against the guidelines and other fraud and other kinds of things that have to be checked.”

The shift, as he sees it, is from rules-based automation to agents that handle complexity. “If you ask any underwriter, they say they spend all of their time on the edge cases,” he said. Older automation could only handle the majority cases. With Autopilot: “We don’t care what kind of document it is, we don’t care what kind of data it is, we don’t care how complex the person’s income is. We’re going to solve this for you.”

On consistency: “You don’t want AI to hallucinate.” After running his own complex financial profile through the system repeatedly, “I ran it through 100 times, I got the same exact answer from the AI every single time.”

And on where this is going: “Every single consumer has a very personalized, very tailored experience that’s generated on the fly for them.” The goal is to make “the underwriters and processors and the consumer … 100x more efficient.”

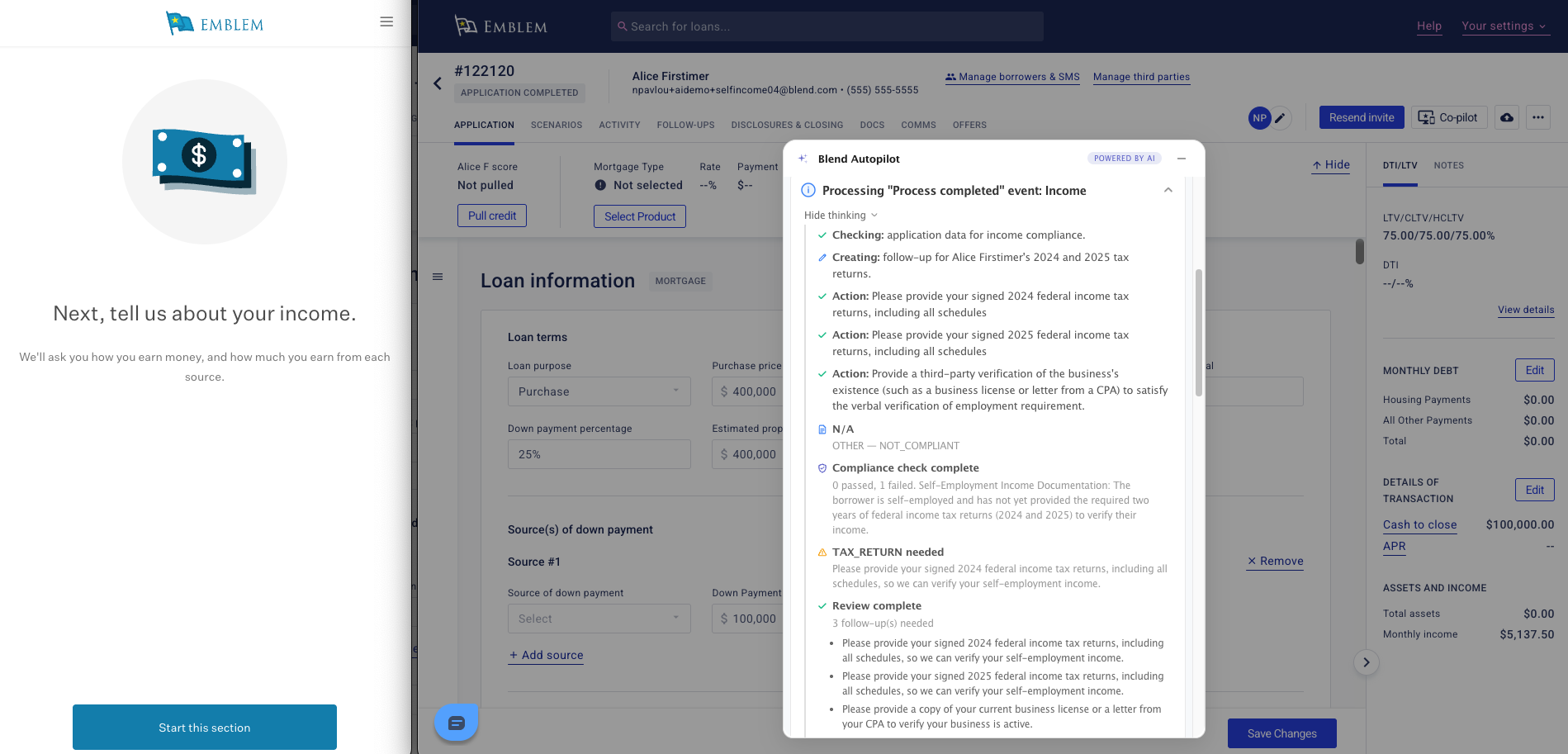

The pre-underwriting summary now ships in the product

Two weeks ago, we introduced the Pre-Underwriting Summary: a structured PDF that distills every finding, calculation, and recommendation into one document. We shared it with lenders and started collecting feedback.

This week, it ships into the product, with significant enhancements based on what we heard.

The summary PDF now renders full income calculation breakdowns directly in the document. When Autopilot calculates qualifying income from a W-2, Schedule C, or K-1, the PDF shows every step: the formula, the inputs, the result, the unit, and the guideline citation. For a self-employed borrower where the agent averages two years of Schedule C income, subtracts business use of home, and adds back depreciation, each of those operations is laid out in the PDF itself, not just referenced.

Income calculations now also carry GSE reference IDs, so every number in the summary is traceable back to the specific guideline rule that produced it. For underwriters, this means one document with everything: findings, methodology, and audit trail. For compliance teams, every calculation is citation-linked and reproducible.

Preview to production in two weeks. That’s the pace.

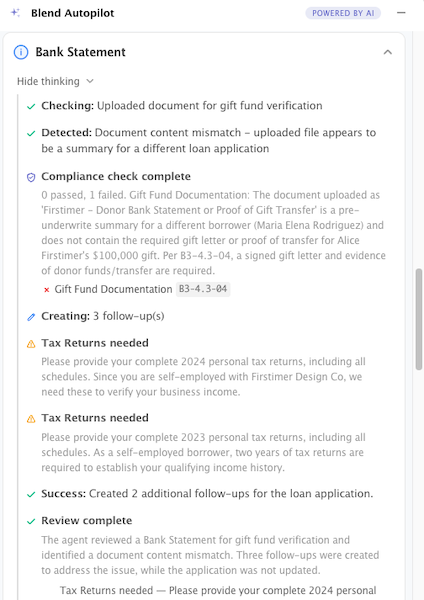

Document validation is smarter and more transparent

Two improvements this week to how Autopilot handles document review.

First, the document classification and validation prompts have been significantly improved. The agent is now more accurate at identifying document types and catching issues, particularly for edge cases where documents are incomplete, mislabeled, or not what was requested.

Second, when a document doesn’t pass validation, the borrower now sees specific reasons why. Instead of a generic “please re-upload” message, the borrower gets actionable feedback tied to what was actually wrong with their submission. Wrong document type? Missing pages? Illegible scan? The system tells them exactly what to fix.

This matters because vague document requests are one of the biggest drivers of borrower confusion and follow-up abandonment. Specific, clear feedback means faster re-uploads, fewer support calls, and fewer loans stalling on document collection.

Loan officers now see a full Autopilot activity history

When Autopilot processes documents, creates follow-ups, calculates income, and resolves tasks on a loan, every action is logged. Loan officers could already see this activity, but on complex loans with many documents and borrower interactions, the list could get long.

The agent activity feed now supports full pagination. Loan officers can scroll through the complete history of what Autopilot did on a loan, from first document to latest follow-up, without hitting a wall. For operations teams processing high volumes, this means complete visibility into agent behavior on every loan, no matter how many actions were taken.

Improvements under the hood

Beyond the headline features, the team shipped a series of quality, reliability, and infrastructure improvements this week:

- Per-lender feature flags: Autopilot now supports tenant-based feature flags with automatic updates, giving lenders granular control over which capabilities are active in their environment.

- Expanded evaluation coverage: New eval scenarios for wrong-document detection (incomplete and dummy uploads) and bank statement account ownership verification. These evals run continuously to catch quality regressions before they reach production.

- Summary generation reliability: Fixed edge cases that caused summary PDF generation to fail in certain sandbox configurations.

- Asset data pipeline: Restored asset data fetching in application data retrieval, ensuring the agent has complete financial context when processing documents.

- 10+ internal improvements across CI pipelines, test coverage, tracing, and code quality.

What’s coming next for Autopilot

Four new capabilities and a full slate of reliability improvements this week, shipped while the team was on the road at ICE Experience.

The reception from lenders has been strong. Dozens of lenders have activated Autopilot since launch, many self-serving directly into production without an onboarding call. The conversations at ICE Experience reinforced what we’re seeing in the data: lenders want this, and the ones who’ve turned it on are seeing results immediately.

Looking ahead, we’re continuing to expand what Autopilot understands. Credit analysis, pricing, fees, and DU results are on the roadmap, giving the agent a fuller picture of each loan. And borrower chat is coming, where borrowers can interact with the agent directly about their loan, their documents, and what’s needed next.

Every improvement ships automatically to every lender with Autopilot activated. No upgrade cycles. No implementation projects. The agent gets better every week.

We’ll be back next Wednesday with what’s new.

Blend Autopilot is currently in preview and free to activate and use during the preview period for all Blend customers. To get started, visit your Lending Config Center or contact your Blend account team.

We publish a new update every Wednesday. Subscribe to the Autopilot weekly update to make sure you stay up to date with everything we are shipping.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

Embedded Insurance Infrastructure: A Blueprint for Reducing Loan Fallout

Learn how embedded insurance infrastructure reduces loan fallout, cuts origination costs, and creates a seamless borrower experience inside your existing mortgage workflow.

Read the article about Embedded Insurance Infrastructure: A Blueprint for Reducing Loan Fallout

Blend Autopilot Week 5 Update: Autopilot MCP Server Ships, Opening the Full Lending Platform to AI Agents

One connection. Full platform access. Here's what Autopilot MCP means for your institution.

Read the article about Blend Autopilot Week 5 Update: Autopilot MCP Server Ships, Opening the Full Lending Platform to AI Agents

Next-Level Growth: Closing the Execution Gap in 2026

Join Blend, Cornerstone Advisors and, People First FCU, as they operationalize the findings of the Next-Level Growth: Credit Union Opportunities in a Changing Market report.

Watch video about Next-Level Growth: Closing the Execution Gap in 2026