December 16, 2025 in Blend momentum

5 Ways Blend Customers Transformed Their Operations in 2025

From accelerating loan decisions to pioneering AI-powered quality control, Blend customers delivered breakthrough results that drove operational transformation in lending and consumer banking.

The best measure of innovation isn’t what gets built. It’s what customers achieve with it. While the lending industry buzzed about AI announcements and digital transformation roadmaps, Blend customers quietly delivered breakthrough results that redefined what’s possible in origination.

From faster close times to increased loan funding to the near-elimination of one of the industry’s biggest headaches, Blend’s updates in 2025 empowered customers to turn industry challenges into competitive insights.

1. Twelve customers accelerated loan decisions with personalized workflows

Customers eliminated pipeline losses stemming from unsure prospects.

When borrowers can’t immediately see how a loan benefits their specific situation, they abandon applications or delay decisions. Over a dozen Blend customers solved this problem by implementing Rapid Home Lending products that delivered personalized financial impact within the first session.

The results were measurable. Early adopters reported 20% higher pull-through rates and 50% faster time to close, delivering 2x more value per funded loan versus their prior processes. Borrowers viewing their exact before-and-after payments and cash-out potential reached intent-to-proceed decisions faster. No more losing prospects to competitors while customers calculated benefits manually.

The operational impact extended beyond individual conversions. Faster decision-making accelerated entire pipelines, reducing the time loans spent in processing and improving capital efficiency. For lenders managing capacity constraints and portfolio risk, this velocity improvement translated directly to profitability.

2. Credit unions captured 90-second account openings during peak intent moments

Institutions transformed deposit gathering from administrative overhead into competitive advantage.

Opening deposit accounts used to mean choosing between speed and security—fast processes risked fraud, while secure processes frustrated potential members with lengthy applications. Credit unions using Blend’s latest deposit solution proved this tradeoff was unnecessary, achieving seamless 90-second account opening without compromising security.

For credit unions competing against banks and fintechs on member experience, this speed became decisive for competitive differentiation. They could capture membership opportunities at the moment of intent rather than losing prospects during multi-day approval processes that frustrated the customer experience. And real-time funding meant new members could use their accounts immediately rather than waiting for traditional clearing processes.

Early users reported a 50% reduction in borrower withdrawal rates and a 15% lift in funded loan volume. The flagship mortgage improvements delivered 3.5 hours of processing time saved per loan and 25% fewer underwriting turns per application.

3. Lenders positioned themselves as financial problem-solvers through intelligent debt solutions

Early adopters strengthened customer relationships during economic uncertainty.

With consumer debt at historic highs and elevated rates creating payment stress, borrowers increasingly sought consolidation solutions. But most lenders made customers calculate benefits themselves—comparing rates, terms, and potential savings across multiple obligations. Blend customers took a different approach.

Using intelligent debt consolidation capabilities built into Blend’s personal loan and home equity workflows, these lenders automatically analyzed borrower trade lines and identified higher-rate debts that made sense to consolidate. Instead of forcing customers to do complex calculations, borrowers simply selected which debts to pay off to see exact monthly payment reductions and total interest savings.

The positioning shift was profound. Rather than being seen as just another capital provider, these lenders became financial problem-solvers. When borrowers could see concrete monthly payment improvements and understand their total savings, they moved forward with confidence and viewed their lender as a trusted partner.

The strategic value extended beyond individual transactions. Institutions helping customers manage debt effectively built loyalty that survived rate cycles and competitive pressures. When borrowers experienced their financial institution as a partner in improving their situation, rate shopping became less relevant.

4. Forward-thinking institutions accelerated innovation through strategic partnerships

Ecosystem approaches delivered best-in-class capabilities faster than internal development.

Ecosystem collaboration enabled institutions to adopt best-in-class capabilities far faster than internal development. Rather than waiting years for vendors to build new features, leading Blend customers leveraged the platform’s growing partner ecosystem—activating solutions from partners like Covered for insurance shopping, Doma for title and settlement, and Truework for income and employment verification—directly within their existing workflows.

These integrations delivered immediate capability enhancements: fraud detection automatically strengthened every application, income verification improved underwriting accuracy across loan types, and AI tools accelerated document processing and quality control without requiring additional implementation effort.

The time-to-market advantage was decisive. By avoiding lengthy development cycles and eliminating integration complexity, institutions were able to deploy proven solutions instantly—accelerating innovation while preserving internal resources.

5. CrossCountry Mortgage piloted intelligent AI that aims to redefine quality control

Strategic partnership demonstrates AI’s potential to transform quality control operations.

Early pilot partners are already seeing what Intelligent Origination can unlock. At CrossCountry Mortgage, the technology is being evaluated for quality control, a function that traditionally requires heavy manual review and deep regulatory expertise.

Today, most lenders can only review a small percentage of loans due to the time required. During testing with Intelligent Origination, compliance checks that used to take analysts 15–20 minutes per task were completed in under 30 seconds. The system automatically flagged discrepancies, surfaced the relevant source documents, and showed the reasoning behind every recommendation, all in a format that meets investor and examiner standards.

According to Rebecca Blabolil, Chief Compliance Officer at CrossCountry Mortgage, the impact extended beyond speed. The AI caught compliance issues that human reviewers had missed, including subtle violations such as processor certifications that did not explicitly satisfy FCRA requirements, loans that had previously been marked as “pass” by the QC team.

“For the first time, we can see a path to full-file QC before funding,” Blabolil said. “Individual checks that once took analysts 20 minutes per task now happen in seconds. That speed doesn’t just reduce costs—it may allow us to review every loan in the future, turning quality control from a reactive process into a proactive safeguard.”

This pilot is just the beginning. It demonstrates how embedding intelligence into core workflows can transform oversight from a bottleneck into a strategic advantage—delivering both greater operational efficiency and stronger compliance outcomes.

Measurable impact, not marketing promises

2025 wasn’t just a year of product launches. It marked a fundamental shift in how financial institutions operate. Blend customers didn’t wait for the future of lending to arrive; they built it. By embedding intelligence, automation, and ecosystem capabilities directly into core workflows, they created origination models that are faster, more profitable, and deeply customer-centric.

These advancements didn’t happen in isolation, they reinforced one another. Document intelligence didn’t just improve quality control; it accelerated underwriting, streamlined processing, and reduced loan fallout. Expanded partner integrations didn’t just enhance fraud detection; they elevated trust and security across every product line, from mortgage and home equity to consumer lending and deposits. Each improvement multiplied the value of the next.

The institutions that will lead in 2026 won’t be defined by the technology they purchase, but by how effectively they operationalize it. What Blend customers proved this year is clear: when innovation meets execution, transformation isn’t theoretical. It’s measurable, scalable, and already underway.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

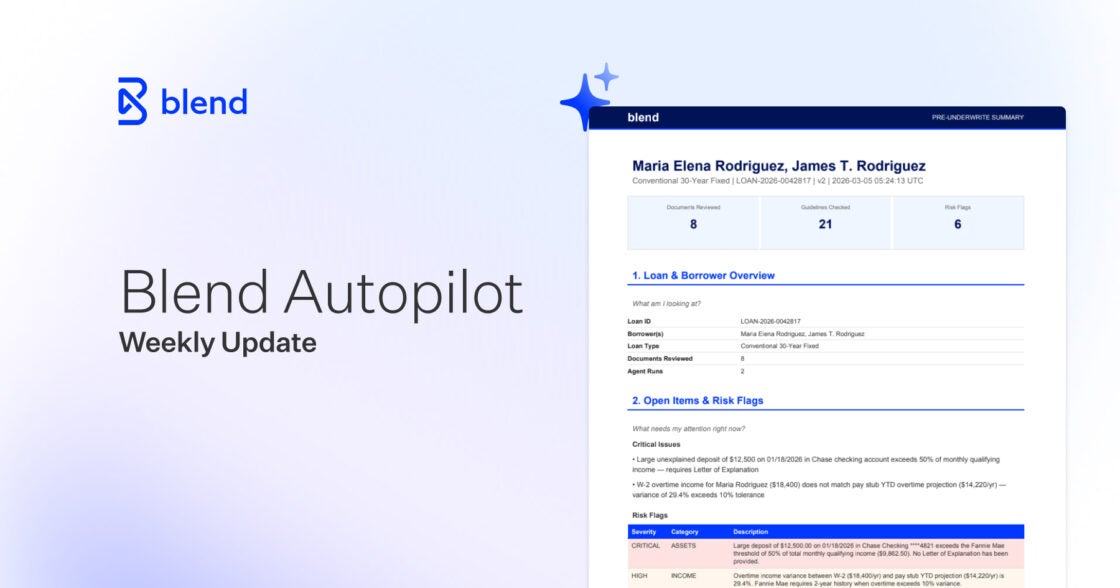

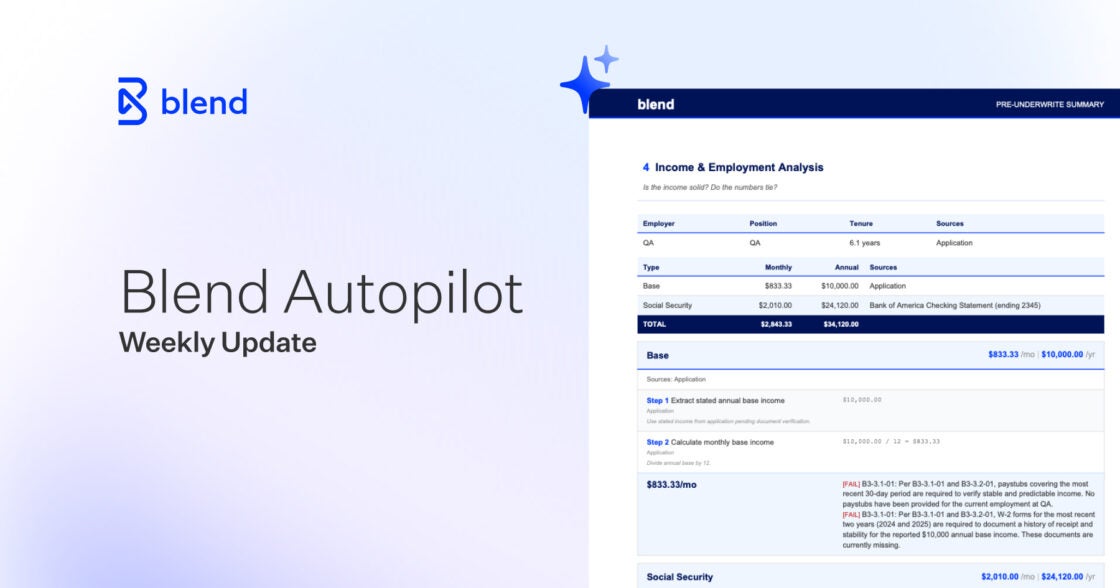

Blend Autopilot Week 4 Update: Borrower Chat Is Coming, API-Uploaded Documents Now Visible to Autopilot, and Smarter Cross-Document Analysis

Real adoption, real feedback. See how lenders are shaping what Autopilot has become this week.

Read the article about Blend Autopilot Week 4 Update: Borrower Chat Is Coming, API-Uploaded Documents Now Visible to Autopilot, and Smarter Cross-Document Analysis

Reduce Pre‑Closing Delays with Refreshable Asset‑Based Employment Checks

Learn how refreshable, asset‑based employment checks can reduce pre‑closing delays, cut last‑minute outreach, and align with DU®, LPA®, and agency expectations.

Read the article about Reduce Pre‑Closing Delays with Refreshable Asset‑Based Employment Checks

Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation

AI that handles edge cases automatically. See what shipped in Autopilot's third week of production.

Read the article about Blend Autopilot Week 3 Update: Nima Ghamsari on Why Blend Built Autopilot, the Pre-Underwriting Summary Ships to Production, and Smarter Document Validation