November 25, 2025 in Thought leadership

Growth Engine 2.0: How Leading Lenders Are Turning Existing Demand into Real Revenue

Operational efficiency in lending is now driven by strategic activation, mobile engagement, and continuous funnel optimization—not by chasing more leads.

The mortgage market doesn’t have a lead generation problem. It has a conversion problem. Lenders are spending millions to drive awareness and fill the top of the funnel, yet the majority of prospects never make it to an application. As one executive put it during a roundtable, “We don’t need more leads. We need to stop losing the ones we already paid for.”

Across banks, credit unions, and independent mortgage lenders, the pattern was remarkably consistent: the biggest performance gap isn’t at the point of application submission, it’s in the moments before a borrower decides to engage. In fact, participants reported that up to 83% of fallout happens before a single field of the application is completed.

What separates the top performers isn’t marketing spend or brand recognition. It’s the ability to convert existing demand through better timing, better engagement, and better orchestration across channels, loan officers, and technology.

Here are the nine most practical strategies lenders are using right now to plug the leak, reclaim revenue, and build a modern growth engine backed by their real-world results and direct insights from the discussion.

1. Your funnel isn’t broken at the bottom. It’s bleeding at the top.

While many organizations focus their optimization efforts on application completion, the largest drop-off occurs before a borrower ever begins the application. Participants reported that as much as 83% of fallout happens between initial marketing engagement and first click. One executive noted, “We’re not losing borrowers during the application. We’re losing them before they even start.”

This early-stage attrition is now one of the biggest untapped growth opportunities. The institutions that are outperforming are not generating more leads; they are improving activation by closing the gap between initial interest and meaningful engagement.

Strategic shift: Growth is increasingly driven by how effectively institutions convert existing demand, not by how much new demand they generate. Lenders are deploying progressive activation strategies like lightweight entry points, immediate LO engagement via SMS, and AI-driven follow-up designed to convert curiosity into commitment.

2. Treat verification as a strategic lever for cost efficiency and conversion confidence

Verification isn’t just a procedural step, it’s one of the most influential drivers of both cost management and borrower commitment. Participants emphasized two key realities:

- Initiating full verification too early can create unnecessary expenses and cause prospects to drop off before they’ve signaled serious intent

- Delaying verification too long can create uncertainty, leading borrowers to keep shopping or disengage from the process altogether

As one participant put it, “The question isn’t whether to verify. It’s when it creates the most leverage.”

Institutions that are outperforming are using a progressive verification strategy:

- Starting with soft credit checks or asset connectivity to qualify interest at a low cost

- Layering in full income and credit verification when it strengthens borrower confidence, improves pull-through, or solidifies realtor relationships

Strategic shift: Leading lenders are aligning verification timing with borrower intent and psychological inflection points. By viewing verification as both a cost control mechanism and a trust-building moment, they are maximizing conversion while protecting margin.

4. The channel you use matters

A consistent theme across institutions was the widening gap in engagement effectiveness between email and mobile channels. Participants reported that SMS delivers response rates up to 100% higher than email, and that AI-powered voice follow-up outperformed traditional call center outreach by a factor of 4–7x. One executive shared, “If we text a customer, we hear back. If we email them, we may never hear back.”

The lesson was clear: borrowers are more likely to respond when the channel mirrors how they already communicate in their daily lives. Mobile-first engagement is no longer a differentiator. It is becoming the baseline expectation.

Strategic shift: Leading lenders are rebalancing from email-dominant nurturing to channel strategies that emphasize immediacy and accessibility. This includes SMS-first engagement, AI voice follow-up on abandoned applications, and loan officer outreach that meets customers in the channel they started in.

5. Never force channel switching

A key source of funnel leakage is channel switching. Many institutions discovered that when a customer initiates engagement by phone, asking them to switch to a self-serve digital experience leads to immediate drop-off. As one participant noted, “The second you tell someone, ‘Go log in instead,’ you’ve lost them.”

Institutions that maintain the engagement channel from start to finish consistently reported higher conversion rates. For example, several lenders shared that when loan officers sent a Blend application invite during the live phone call and guided the borrower through the first steps using co-pilot functionality, adoption rates increased significantly.

Strategic shift: Rather than pushing borrowers into a single standardized path, leading lenders are matching the experience to the borrower’s entry point, whether phone, SMS, or digital, and using technology to augment, not redirect, human engagement.

6. Win the relationship game for purchase loans

Participants consistently reported that purchase loan funnels underperform refinances—not because of borrower intent, but because of ecosystem complexity. A key insight shared during the roundtable was that conversion in purchase transactions is heavily influenced by third-party engagement, especially realtors and builders. As one participant stated, “If the realtor isn’t participating in our process, the deal usually falls apart before the contract.”

Digital optimization alone cannot overcome these relational dependencies. Institutions that are outperforming in purchase lending are deliberately supporting loan officers with tools and programs that strengthen referral relationships, improve communication with transaction partners, and create shared visibility across parties.

Strategic shift: Leading lenders are investing in relationship enablement, integrating builders and realtors into the transaction journey, equipping loan officers with proactive engagement tools, and aligning incentives across all parties involved in the purchase funnel.

7. Capture intent data you’re currently throwing away

Roundtable participants acknowledged that valuable borrower signals are frequently captured during interactions but rarely stored or acted upon. Simple questions such as “Are you planning a move in the next year?” or “Is this refinance related to debt consolidation or cash flow?” can indicate future lending opportunities, yet these responses often remain disconnected from CRM systems.

Several lenders noted that up to 10% of future funded volume could be attributed to customer intent captured earlier in the journey, but only when that data was systematically collected and used for re-engagement.

As one participant said, “We already talk to these customers. We just don’t capture what they’re telling us.”

Strategic shift: Leading institutions are operationalizing intent capture by embedding lightweight data prompts into early borrower touchpoints and connecting them directly into marketing automation and retention workflows. Rather than treating conversations as one-time interactions, they are turning them into future triggers for high-quality engagement.

8. Test your way to higher conversion

Participants emphasized that conversion optimization is not achieved through one major redesign, it’s achieved through continuous iteration. Institutions conducting consistent A/B testing reported measurable improvements, with one lender citing a 5% lift in application completion from a single declaration field change.

Testing frequency has also become a differentiator. Some lenders are deploying updates multiple times per month, allowing them to respond quickly to borrower behavior and continuously refine performance.

As one participant shared, “We don’t wait for a quarterly review—if something is working, we scale it immediately.”

Strategic shift: Conversion excellence is no longer a static project, it’s an operational discipline. Leading institutions are making small, frequent adjustments to high-traffic areas of the funnel, recognizing that marginal gains compound into significant volume growth over time.

9. Make quality everyone’s problem

Operational leaders shared that incomplete or inaccurate applications create avoidable friction downstream, leading to processing delays, additional documentation requests, and borrower frustration. Yet quality control is often treated solely as a back-office function, disconnected from loan officer accountability.

Institutions that have made the most progress are those that have embedded quality expectations into the front of the process. One participant described tying a small compensation adjustment to submission quality, noting: “Once we aligned incentives, quality improved almost overnight.”

This is not about penalizing teams, it’s about ensuring that high standards are supported by clear expectations and aligned performance metrics.

Strategic shift: Leading lenders are elevating application quality from an operational issue to a front-line responsibility. By reinforcing quality at the point of origination, they reduce cycle time, improve customer satisfaction, and increase overall profitability.

The reality check

The lenders winning today aren’t chasing more leads. They’re converting more of what they already have through smarter data use, better channel management, and strategic technology deployment.

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

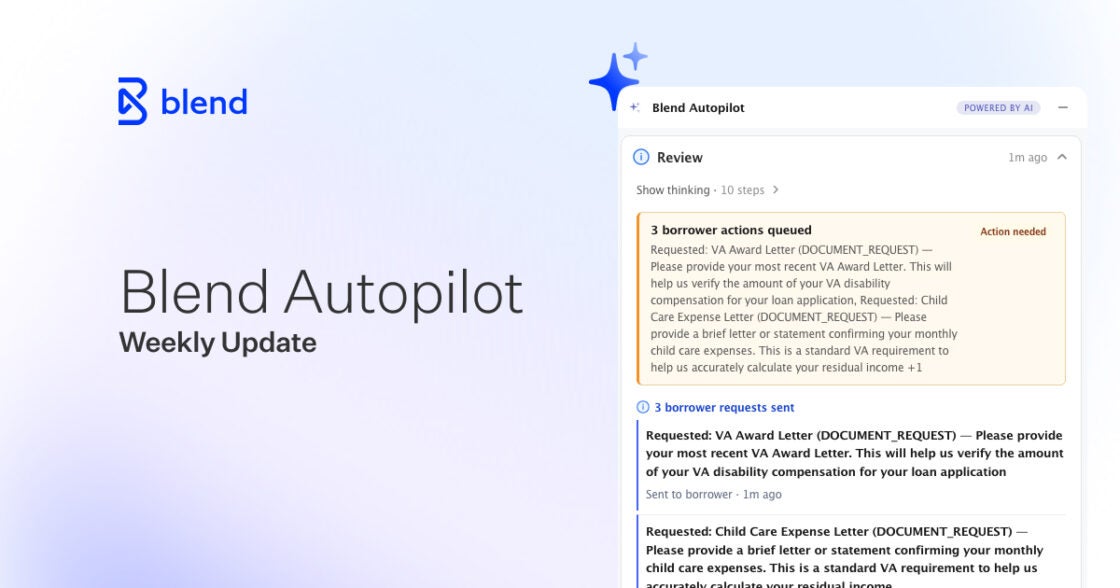

Blend Autopilot Week 11 Update: Rapid, VA, and FHA Continue to Harden, Ongoing Investment in Accuracy, and Verified Income Goes End to End

When upstream income is verified, Autopilot already knows. See what else shipped in week 11.

Read the article about Blend Autopilot Week 11 Update: Rapid, VA, and FHA Continue to Harden, Ongoing Investment in Accuracy, and Verified Income Goes End to End

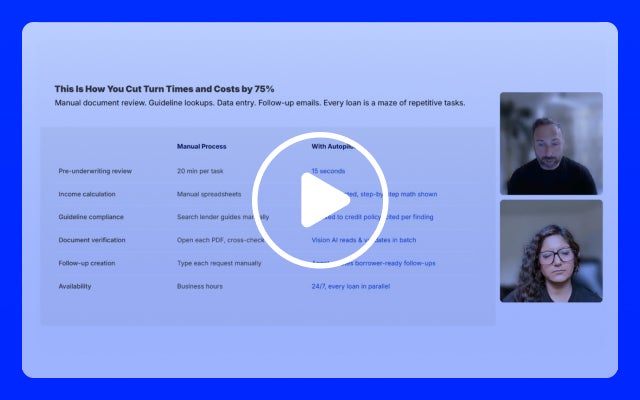

Home Equity Is the Proving Ground: How Digital-First Origination Will Define the Next Era of Lending

Speed is winning home equity. See how digital origination helps your institution compete.

Watch video about Home Equity Is the Proving Ground: How Digital-First Origination Will Define the Next Era of Lending

CrossCountry Mortgage

streamlined operations, eliminated errors, and empowered borrowers through Blend Close.

streamlined operations, eliminated errors, and empowered borrowers through Blend Close.

Read the full story about CrossCountry Mortgage