July 27, 2023 in Consumer Banking Suite

How to deliver a human touch in a digital-first world

Empathy is the key to modern financial experiences with today’s distrustful consumers.

The failures of Silicon Valley Bank, First Republic Bank, Silvergate Bank, and Signature Bank have raised concerns over the industry’s short-term and long-term health as well as the impact this volatility may have on the economy. Banks are also concerned about how they are perceived by the public. U.S. Treasury Secretary Janet Yellen recently said that she would not be surprised to see more bank consolidation. There has certainly been reason for concern among board members and senior management in regard to the future direction of both the industry as a whole and likely their specific institution.

The action of the central bank will also be critical to build back some of the confidence that was lost during the last few months as we wrestle with economic uncertainty. Despite the well-publicized failures, poor management of interest rate risk and cryptocurrency bets paint the entire industry with the same brush. In a world where large and small banks can coexist, the first step is to improve the customer experience and enlisting the right tools to target a portion of the approximate 75% of domestic dollars that, according to the FDIC, remains within the largest 15 banks in the U.S. A slight shift in deposits away from the largest institutions can occur while barely making a dent in the strength of these banks while providing much needed fuel to grow regional and community banks and credit unions.

So, what does it take to thrive with these new expectations of an empathetic customer experience?

The good news: the majority of regional and community banks and credit unions will end up thriving, if they learn to adapt and focus on what they do well and recognize the key traits to success. The key is to recognize and value the need for partner solutions and the role of embedded finance and the impact they will have on their institution. For some institutions, the idea of embracing a complete, digital-first strategy is met with hesitation. However, the reality is that there are many options that a bank can choose to create a modern and empathetic financial experience while pursuing a digital-first approach.

Trust is low and empathy is rising

IDC recently conducted a consumer survey around the impact that environmental, social, and corporate governance (ESG) has on the U.S. and Canadian banking clients. One telling statistic was revealed when respondents were asked a question about bank profits versus the banks helping them achieve financial success.

Of surveyed consumers, 68.7% believe that their bank was more interested in profits than helping them during their financial journey.¹

This is where institutions must do better in providing financial education and improving the process of matching products with customers’ needs, and not necessarily to maximize bank profit. In the same survey,

One out of six customers use the bank’s reputation, philanthropy and support of important causes as a factor in choosing their institution.²

This sentiment is particularly important with small business owners, a growing and important segment for all retail banks, as it is for consumers choosing personal financial products as well.

Providing empathy has often been associated with just the human touch, and while that is a key measure, the human touch is difficult to provide in our digital-first world. Empathy has to be delivered at scale in order to truly provide a level of experience that a customer remembers – one that elicits a feeling that the customer is special and the institution cares about them. Providing this service will pay off in increased lifetime value and improved CSAT scores, yet more importantly, this kind of empathetic service will provide the necessary ingredients for financial institutions of all sizes to be competitive.

Delivering an empathetic financial experience

For institutions that choose to develop an empathetic approach internally, it could prove to be unsustainable long-term. Another option includes pursuing a strategy in which they become best-in-class providers in a specific aspect of banking, such as lending, risk management, compliance, or customer experience. To specialize in a best-of-class approach, the institution might want to partner with vendors who provide white-label offerings as a way to expand or refine new services while providing customers with a highly personalized and seamless experience. One such use case would be for a bank to partner with a brokerage service to offer self-managed investment options for customers who want to build their portfolios. In this scenario, individuals would become customers of the brokerage firm that in turn will handle all the compliance aspects while the customer can remain in the bank’s branded solutions set, creating a single point for engagement through the institution’s digital offerings. In another use case, some larger-sized institutions could provide their own operations and infrastructure as a service to help smaller-sized institutions expand without the need of investing in their infrastructure. And finally, institutions may choose to be an orchestrator in the industry ecosystem by providing advisory, compliance, and governance solutions. As one can see, there are options.

Integrating platform solutions and hybrid engagement

Those institutions that thrive are also going to fully embrace the value that a modern platform solution can provide. They will seek solutions that are cloud native and can leverage the ever growing shared and published APIs to legacy platforms that allow for integration without replacing core (for now) technologies. In our digital-first world, these modern platforms can handle the scale, speed, and complexity necessary to help banks compete. The cloud also serves as the foundation for generative AI and large language models, which inevitably will find their way into employee experiences first, but eventually into customer experiences as well. While we have some time to fully grasp the impact of generative AI, staying in front of vendor solutions and compliance mandates will level the playing field even further, allowing for institutions to provide the same solutions regardless of asset size.

Finally, having a digital-first approach is not just a preference among most institutions – it’s increasingly required as workloads continue to shift from manual to digital. This shift is necessary for institutions to create new ways to engage with customers that were not possible a few years ago. This does not mean that the branch is going away as retail and small business customers will continue to rely on it for the foreseeable future. Rather, further integration of digital technologies into the branch is going to be necessary to create the hyper-personalized experiences customers want. Smaller banks that invest in online and mobile solutions to better compete with the largest institutions will have an opportunity to regain market share.

Curious to see the kind of tech that helps deliver empathetic, hybrid engagement?

¹IDC Financial Insights North American Consumer Banking Channel Preference Survey, January 2023 n=2750

²IDC Financial Insights North American Consumer Banking Channel Preference Survey, January 2023 n=2750

Find out what we're up to!

Subscribe to get Blend news, customer stories, events, and industry insights.

How Lenders Can Reach More Bilingual Borrowers Without Adding Friction

Bilingual borrowers are a growing market. See how clarity, not just translation, builds confidence and keeps loans moving.

Read the article about How Lenders Can Reach More Bilingual Borrowers Without Adding Friction

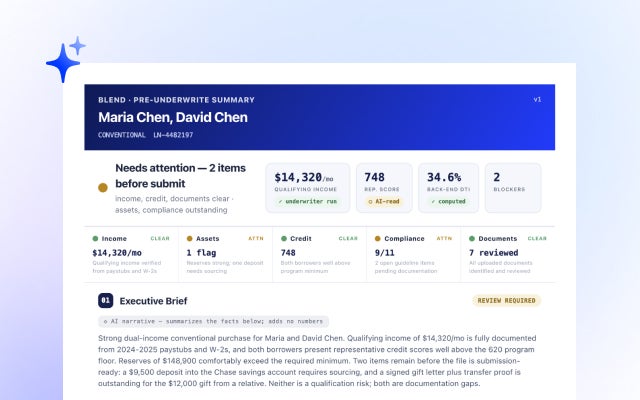

Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Every figure, every source. See how Autopilot's latest update makes pre-underwriting faster to act on.

Read the article about Autopilot Update: A Pre-Underwriting Summary That Shows Its Work, and Sharper Income and Asset Judgment

Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan

The mortgage market is projected to reach $2.2 trillion in 2026, but flat isn't the same as easy. With per-loan costs exceeding $12,500, discover why cost per loan is the…

Read the article about Competing in a Flat $2.2 Trillion Market by Fixing Cost per Loan